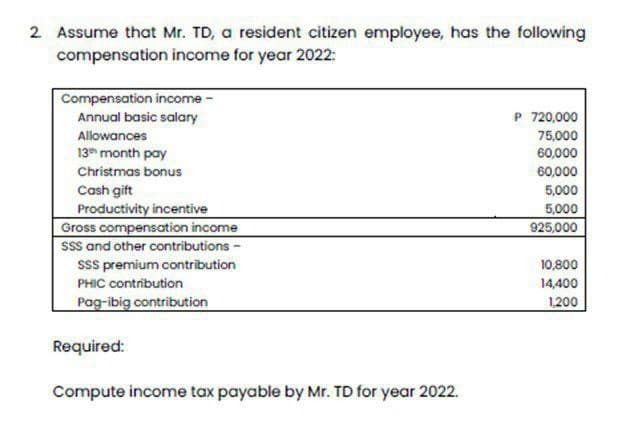

2. Assume that Mr. TD, a resident citizen employee, has the following compensation income for year 2022: Compensation income- Annual basic salary Allowances 13th month pay Christmas bonus Cash gift Productivity incentive Gross compensation income SSS and other contributions - SSS premium contribution PHIC contribution Pag-ibig contribution Required: Compute income tax payable by Mr. TD for year 2022. P 720,000 75,000 60,000 60,000 5,000 5,000 925,000 10,800 14,400 1,200

2. Assume that Mr. TD, a resident citizen employee, has the following compensation income for year 2022: Compensation income- Annual basic salary Allowances 13th month pay Christmas bonus Cash gift Productivity incentive Gross compensation income SSS and other contributions - SSS premium contribution PHIC contribution Pag-ibig contribution Required: Compute income tax payable by Mr. TD for year 2022. P 720,000 75,000 60,000 60,000 5,000 5,000 925,000 10,800 14,400 1,200

Chapter12: Alternative Minimum Tax

Section: Chapter Questions

Problem 24CE

Related questions

Question

Answer number 1 and 2.

Transcribed Image Text:2. Assume that Mr. TD, a resident citizen employee, has the following

compensation income for year 2022:

Compensation income -

Annual basic salary

Allowances

13th month pay

Christmas bonus

Cash gift

Productivity incentive

Gross compensation income

SSS and other contributions -

SSS premium contribution

PHIC contribution

Pag-ibig contribution

Required:

Compute income tax payable by Mr. TD for year 2022.

P 720,000

75,000

60,000

60,000

5,000

5,000

925,000

10,800

14,400

1,200

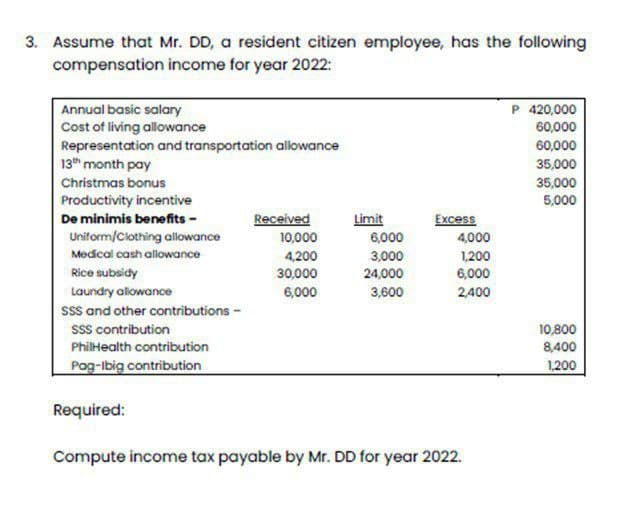

Transcribed Image Text:3. Assume that Mr. DD, a resident citizen employee, has the following

compensation income for year 2022:

Annual basic salary

Cost of living allowance

Representation and transportation allowance

13th month pay

Christmas bonus

Productivity incentive

De minimis benefits -

Uniform/Clothing allowance

Medical cash allowance

Rice subsidy

Laundry allowance

SSS and other contributions -

SSS contribution

PhilHealth contribution

Pag-Ibig contribution

Received

10,000

4,200

30,000

6,000

Limit

6,000

3,000

24,000

3,600

Excess

4,000

1,200

6,000

2,400

Required:

Compute income tax payable by Mr. DD for year 2022.

P 420,000

60,000

60,000

35,000

35,000

5,000

10,800

8,400

1,200

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College