2. Consider an expected utility maximizing risk-averse individual with the utility-of- wealth function u(w) and initial wealth wo. There is a lottery that pays G with probability p and B with probability 1 -P, with G> B. (a) Suppose the individual already owns the ticket to this lottery, in addition to her initial wealth. Find an equation that implicitly defines the smallest price P, such that she would be willing to sell the ticket for this price. (b) Now suppose she does not initially own the ticket, and has to consider whether to buy one. Find an equation that implicitly defines the highest price P, that she would be willing to pay to buy the ticket. (c) Calculate P, and P, if the individual's utility function of his final wealth w is u(w) = √w, and G = 10, B = 0, wo = 10, and p = 0.5.

2. Consider an expected utility maximizing risk-averse individual with the utility-of- wealth function u(w) and initial wealth wo. There is a lottery that pays G with probability p and B with probability 1 -P, with G> B. (a) Suppose the individual already owns the ticket to this lottery, in addition to her initial wealth. Find an equation that implicitly defines the smallest price P, such that she would be willing to sell the ticket for this price. (b) Now suppose she does not initially own the ticket, and has to consider whether to buy one. Find an equation that implicitly defines the highest price P, that she would be willing to pay to buy the ticket. (c) Calculate P, and P, if the individual's utility function of his final wealth w is u(w) = √w, and G = 10, B = 0, wo = 10, and p = 0.5.

Chapter7: Uncertainty

Section: Chapter Questions

Problem 7.5P

Related questions

Question

Explanation with answers plz

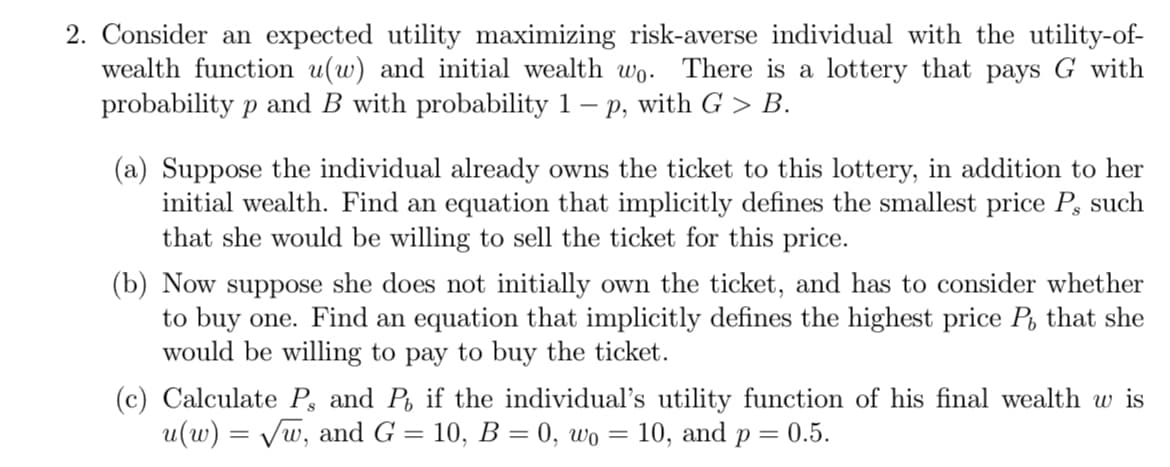

Transcribed Image Text:2. Consider an expected utility maximizing risk-averse individual with the utility-of-

wealth function u(w) and initial wealth wo. There is a lottery that pays G with

probability p and B with probability 1 – p, with G > B.

-

(a) Suppose the individual already owns the ticket to this lottery, in addition to her

initial wealth. Find an equation that implicitly defines the smallest price P, such

that she would be willing to sell the ticket for this price.

(b) Now suppose she does not initially own the ticket, and has to consider whether

to buy one. Find an equation that implicitly defines the highest price P, that she

would be willing to pay to buy the ticket.

(c) Calculate P, and P, if the individual's utility function of his final wealth w is

u(w) = √w, and G = 10, B = 0, wo = 10, and p = 0.5.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 7 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning