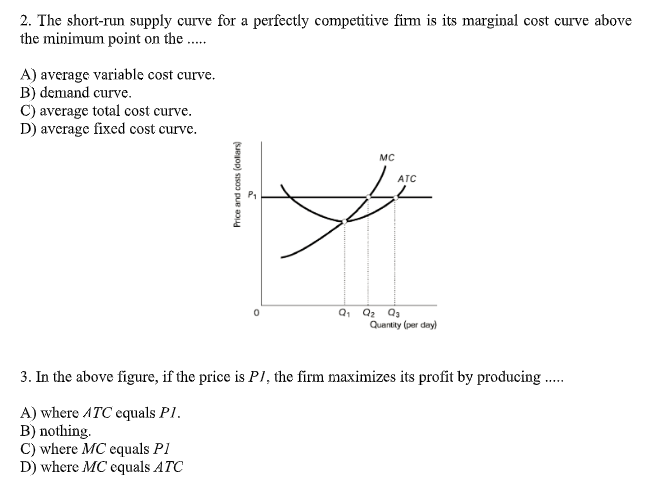

2. The short-run supply curve for a perfectly competitive firm is its marginal cost curve above the minimum point on the . A) average variable cost curve. B) demand curve. C) average total cost curve. D) average fixed cost curve.

Q: 1. Consider a typical perfectly competitive firm with an increasing MC curve. At the current…

A: Q1 A firm in the perfectly competitive market produces at MC=P, In the given problem MC<P, in…

Q: 1. A perfectly competitive firm realizes a total revenue of $2500 and a profit of $500. The firm…

A: Total revenue = Price * quantity 2500 = 12 * qty Qty = 208

Q: rm

A: The short run supply curve In a perfectly competitive market is the curve of marginal cost being at…

Q: QUESTION 7 • Explain the ettect of an increase in demand in a perfectly competitive market in the…

A: The perfectly competitive market is the market structure where a large number of firms compete in…

Q: 3. Suppose you start a business of manufacturing computer software. company is a perfectly…

A: Given: The fixed cost = Tk. 60000 Total cost = Tk. 140000

Q: 5. The short-run cost function of a competitive firm is c(Q) = 0.1Q3 – 2Q2 + 15Q + 10, when the…

A: In perfectly competitive market, price is constant so it is equal to marginal revenue. At profit…

Q: 1) Referring to Figure, at price $80, what is the profit-maximizing output in the short run? 2)…

A: This is a case of a perfect competition market. Here, in the short run Price= AR= MR = $80. The…

Q: shows the short-run cost curves of a toy producer. There are 1,000 identical toy producers. Price…

A: In a perfectly competitive market structure there exists a large number of producers and consumers…

Q: 5. Figure: A Perfectly Competitive Firm in the Short Run Price MC ATC G -MR AVC E N P W B D Quantity…

A: In perfectly competitive market, firms are price takers. Firms do not have any control over the…

Q: a. Is the firm making an economic profit or loss? b. Will firms enter or exit this market? c. Sketch…

A: Firms in a perfectly competitive market face a perfectly elastic individual demand curve as they…

Q: 1. Consider market adjustment from the short-run to the long-run under a perfectly competitive…

A: Since you posted multiple questions, we will provide you the answer of first question. If you want…

Q: 4. Cherry Market The short run equilibrium market price in the perfectly competitive cherry market…

A: Given Short-run cost function: SRTC=Q2+3Q+3 .... (1) Market price p*=9

Q: 4. The number of firms that can survive in a very competitive industry in the long run depends on a.…

A: Economics is a branch of social science that describes and analyzes the behaviors and decisions…

Q: Question 3: Cost Table Question Complete the following short-run cost table for a perfectly…

A: Since we only answer up to 3 sub-parts, we’ll answer the first 3. Please resubmit the question and…

Q: 1.(a) Explain with the help of a graph how a perfectly competitive firm determines its profit-…

A: The perfectly competitive market would result in large number of buyers and sellers in the market.…

Q: 2. A price taker in a perfectly competitive industry is currently selling 6000 units per month at…

A: Total cost = TFC + TVC = $20,000 + $50,000 = $70,000

Q: 1. A firm operating in a perfectly competitive environment faces the following costs and revenues:…

A: The characteristics of perfectly competitive market structure are as follows: (i) There are large…

Q: 8. Consider the following demand schedule. Does it apply to a perfectly competitive firm? Compute…

A: A perfectly competitive firm will always sell their goods and services at a fixed price decided by…

Q: A firm operating in a perfectly competitive market cannot increase its profit. Which of the…

A: Since you have asked multiple question, we will solve the first question for you. If you want any…

Q: 26 - What is the maximum profit condition in a perfectly competitive market? a) TC<MR B)…

A: A perfectly competitive market is the one in which there are numerous sellers and buyers and no…

Q: here a) price is higher than marginal revenue

A: The long-run is defined as the period of time where there exist no fixed variables of production.

Q: 2. Show and explain the equilibrium in the short run for a perfectly competitive firm. Why…

A: Under perfect competition, there are a large number of firms who sell identical products. The…

Q: Exhibit: Perfectly Competitive Firm Price per unit MC ATC $3.00 P. 2.00 1.90 1.00 100 250 300 400…

A: A perfectly competitive firm maximizes profit by producing at d=MC. It accepts the market price as…

Q: onsider the following cost information for a firm that operates in a perfectly competitive market.…

A: In perfectly competitive market, firms earn economic profits in the short run. With free entry and…

Q: 1. Using the characteristics of perfect competition, explain why are garlic producers price-takers.…

A: Firms are said to be in perfect competition when the subsequent conditions occur: (1) many firms…

Q: Refer to Figure #1. The short-run supply curve for a firm in a perfectly competitive market is O the…

A: The short run supply curve of a perfectly competitive firm is the firm's marginal cost on all points…

Q: A perfectly competitive firm faces the short-run cost schedule shown in Table Assume market…

A: The total production process of a firm is an amalgamation of various costs, the optimum quantity…

Q: (1) Consider the following cost schedule for a firm. Quantity Marginal Cost Average Total Cost…

A: The additional cost incurred by a producer when he/she increases the total output by one unit is…

Q: 31. In short-run equilibrium for a competitive firm economic profits: Will be positive. b., Will be…

A: A competitive firm is a price taker in the market. All the buyers and sellers have perfect…

Q: 6. For a perfectly competitive firm, which of the following statement is wrong? A. It enjoys 0…

A: Characteristics of a perfectly competitive market are- 1. Large Number of buyers and sellers -…

Q: 8. (The Short-Run Firm Supply Curve) Each of the following situations could exist for a perfectly…

A: A firm in a perfectly competitive market is one of the many small firms producing and supplying…

Q: 7 What is the total variable cost? 8 Identify the firm's short-run supply curve. 9 Is the industry…

A: In the perfectly competitive market structure, there exists a large number of buyers and sellers of…

Q: (Short-Run Loss) Suppose a firm decides to shut down in the short run. What is the resulting loss?

A: When the price level is charged below the average variable cost, the firm forced to shut down. At…

Q: Short Questions: 1. What are the three conditions for long-run equilibrium for a firm in perfectly…

A: "Since you have asked multiple questions, we will solve the first question for you. If you want any…

Q: 10. In perfect competitive market, there is a firm with a U-shape marginal cost curve. The supply…

A: The supply curve for perfectly competitive firm starts with minimum point of Average variable…

Q: What is the meaning of ‘acceptable loss’ for a perfectly competitive firm ? Draw a graph and…

A: Since you posted multiple questions, we will provide you the answer of first question. If you want…

Q: 12. An industry currently has 100 firms, all of which have fixed costs of $16 and average variable…

A: Hi, thank you for the question. As per our Honor code, we are allowed to attempt only the first…

Q: 2. Since a firm in a perfectly competitive market is a price taker, the demand for this firm's…

A: In the perfect competition, there is a large number of sellers present in the market, and each firm…

Q: QUESTION 7 (10 points): • Explain the effect of an increase in demand in a perfectly competitive…

A: Short Run - Increase in Demand When market demand increases, the market price of the good rises, and…

Q: Explain the three possible profit maximizing positions of perfectly competitive firms in the…

A: Profit maximization is that the method by that a corporation determines the evaluation, input, and…

Q: 3. Illustrate short run supply curve for a perfectly competitive firm and derive market supply…

A: In economics, the short run refers to the time horizon in which some inputs are variable while the…

Q: 20) What will a firm in a perfectly competitive industry do in the short-run if the price of its…

A: Short-run: - it is a short time period in which some factors of production are variable and some are…

Q: the firm under Perfect Competition continues production in the short run even if the firm incurs…

A: Under the perfect competition, firms are price takers. The price of goods and services determined by…

Q: 1. Draw the cost curves for a typical firm. Explain how a competitive firm chooses the level of…

A: The typical cost functions are given in the next step.

Q: 33) At the profit-maximizing level of output for a perfectly competitive firm A) price equals…

A: Economics is a branch of social science that describes and analyzes the behaviors and decisions…

Q: 1. The profit maximizing output for this firm is . 2. In the short-run, this firm will earn $…

A: The monopoly is a market structure which has a single seller and many buyers in the market. The…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

- A perfectly competitive firm faces the short-run cost schedule shown in Table (a)Calculate average total cost (ATC=TC/Q), marginal cost (MC=ATC/AQ) and marginal revenue (MR-ATR/AQ) for each level of output. The price per unit of output is £16 b) Plot ATC, MC and MR on a graph and mark the profit-maximising output. At what output is profit maximised? c) How much profit/loss is made at the optimum level of output? Assume market price declines to £9 per unit. If the firm's average variable cost is £9.5, should the firm shut down in the short run? In the long run? Explain. If the firm is typical of other firms, what price will it charge in the long run? Explain.A perfectly competitive firm faces the short-run cost schedule shown in Table 1. A) Calculate average total cost (ATC=TC/Q), marginal cost (MC=∆TC/∆Q) and marginal revenue (MR=∆TR/∆Q) for each level of output. The price per unit of output is £16. B) Plot ATC, MC and MR on a graph and mark the profit-maximising output. At what output is profit maximised? C) How much profit/loss is made at the optimum level of output?(a) A competitive firm’s short-run supply curve depends on two curves. Which two exact curves are we talking about? (b) Clearly explain which portion/part of these curves provide us with the short-run supply curve of such a firm and which part is excluded from being considered a part of such a supply curve? (c) In this context, explain the economic reason why the short run supply curve of a competitive firm slopes upwards.

- A perfectly competitive firm faces the short-run cost schedule shown in Table 1. A) Assume market price declines to £9 per unit. If the firm’s average variable cost is £9.5, should the firm shut down in the short run? In the long run? Explain. B) If the firm is typical of other firms, what price will it charge in the long run? Explain.How does an increase in market demand for a product in a perfectly competitive market affectthe short-run and long-run equilibrium? Show on a diagram and discuss the adjustments firms make in terms of price and quantity to reach the new equilibrium. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.1)Which kind of industry would have a downward-sloping long-run supply curve? Select one: a. no industry b. a decreasing cost industry c. a constant cost industry d. an increasing cost industry 2)The market for designer jeans is a good example of a perfectly competitive market. Select one: True False 6)The long run is the period after all exit and entry has occurred. Select one: True False

- A perfectly competitive firm faces the short-run cost schedule shown in Table Assume market price declines to £9 per unit. If the firm's average variable cost is £9.5, should the firm shut down in the short run? In the long run? Explain. If the firm is typical of other firms, what price will it charge in the long run? Explain.Course: Microeconomics A given firm, which is part of a perfectly competitive market, would have following cost function: TCLR = 2X3 - 20X2 + 200XWhat will be its level of output (X) and long-run equilibrium price (P)? NOTE: TCLR is long run total cost functionQuestion 8 Art’s Garage operates in a perfectly competitive market. At the point where marginal cost equals marginal revenue, ATC=$20, AVC=$18, and price per unit is $10. Given this situation, in the short run, Art will shut down immediately. Art will shut down, but only after the lease on the garage expires. Art will sustain losses in the short run but will continue to operate. Art will break even.

- a. Draw the marginal cost and average total cost curves for a typical firm. Explain why the curves have the shapes that they do and why they cross where they do. b. Does a competitive firm’s price equal its marginal cost in the short run, in the long run, or both? Explain.A competitive firm’s short-run supply curve is its_________ cost curve above its _________ costcurve.a. average-total-; marginalb. average-variable-; marginalc. marginal-; average-totald. marginal-; average-variableQuestion: In a perfectly competitive market, what is true about the long - run equilibrium? Options: A) Firms earn economic profits in the long run B) Price equals marginal cost for all firms C) There are significant barriers to entry for new firms D) Firms produce at the point where marginal revenue equals marginal cost Note:- Please avoid using ChatGPT and refrain from providing handwritten solutions; otherwise, I will definitely give a downvote. Also, be mindful of plagiarism. Answer completely and accurate answer. Rest assured, you will receive an upvote if the answer is accurate.