A firm's costs are represented in the table below. Assume the firm is only able produce at the quantities listed in the table. Quantity TVC ($) MC ($) AVC ($) TC ($) ATC ($) - 1,000 10 500 50 50 1,500 150 20 900 40 45 1,900 95 30 1,700 80 57 2,700 90 40 4,400 270 110 5,400 135 50 8,000 360 160 9,000 180 60 14,000 600 233 15,000 250 a. If the market price of this good is $110, what is the firm's profit-maximizing quantity? 30 units. b. If the firm produces its profit-maximizing quantity, what is it's total revenue? $ c. What is the total amount of profit or loss? Include a negatve sign if the firm makes a loss. $ d. Suppose the price in the market remains $110, and all firms in the market have identical cost structures. What happens to the number of firms in the long-run equilibrium? decreases.

A firm's costs are represented in the table below. Assume the firm is only able produce at the quantities listed in the table. Quantity TVC ($) MC ($) AVC ($) TC ($) ATC ($) - 1,000 10 500 50 50 1,500 150 20 900 40 45 1,900 95 30 1,700 80 57 2,700 90 40 4,400 270 110 5,400 135 50 8,000 360 160 9,000 180 60 14,000 600 233 15,000 250 a. If the market price of this good is $110, what is the firm's profit-maximizing quantity? 30 units. b. If the firm produces its profit-maximizing quantity, what is it's total revenue? $ c. What is the total amount of profit or loss? Include a negatve sign if the firm makes a loss. $ d. Suppose the price in the market remains $110, and all firms in the market have identical cost structures. What happens to the number of firms in the long-run equilibrium? decreases.

Managerial Economics: A Problem Solving Approach

5th Edition

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Chapter7: Economies Of Scale And Scope

Section: Chapter Questions

Problem 5MC

Related questions

Question

Please answer all parts and show your work!

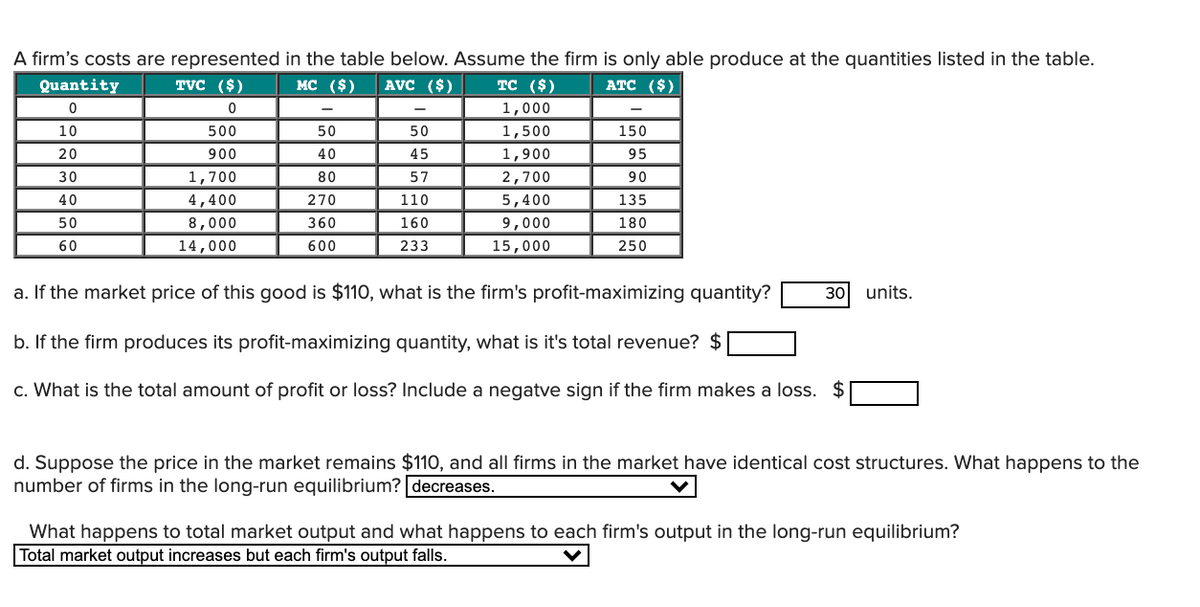

Transcribed Image Text:A firm's costs are represented in the table below. Assume the firm is only able produce at the quantities listed in the table.

тC ($)

Quantity

TVC ($)

MC ($)

AVC ($)

АTC ($)

1,000

10

500

50

50

1,500

150

20

900

40

45

1,900

95

30

1,700

80

57

2,700

90

40

4,400

270

110

5,400

135

8,000

14,000

50

360

160

9,000

180

60

600

233

15,000

250

a. If the market price of this good is $110, what is the firm's profit-maximizing quantity?

30

units.

b. If the firm produces its profit-maximizing quantity, what is it's total revenue? $

c. What is the total amount of profit or loss? Include a negatve sign if the firm makes a loss. $

d. Suppose the price in the market remains $110, and all firms in the market have identical cost structures. What happens to the

number of firms in the long-run equilibrium? decreases.

What happens to total market output and what happens to each firm's output in the long-run equilibrium?

Total market output increases but each firm's output falls.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 6 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou…

Economics

ISBN:

9781285165875

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning