a) What are x and y? b) What are the cumulative repricing gaps for 1 month (CGAP1-month), 3 months (CGAP3-month), 1-year (CGAP1-year), and 2 years (CGAP2year)? c) What is the impact over the next three months on the net interest income if interest rate on RSAS and RSLS both increase by 40 basis points (i.e. +0.4%)?

a) What are x and y? b) What are the cumulative repricing gaps for 1 month (CGAP1-month), 3 months (CGAP3-month), 1-year (CGAP1-year), and 2 years (CGAP2year)? c) What is the impact over the next three months on the net interest income if interest rate on RSAS and RSLS both increase by 40 basis points (i.e. +0.4%)?

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter4: The Balance Sheet And The Statement Of Shareholders' Equity

Section: Chapter Questions

Problem 16P: Ratios Analyses: McCormick Refer to the information for McCormick above. Additional information for...

Related questions

Question

Please provide steps.

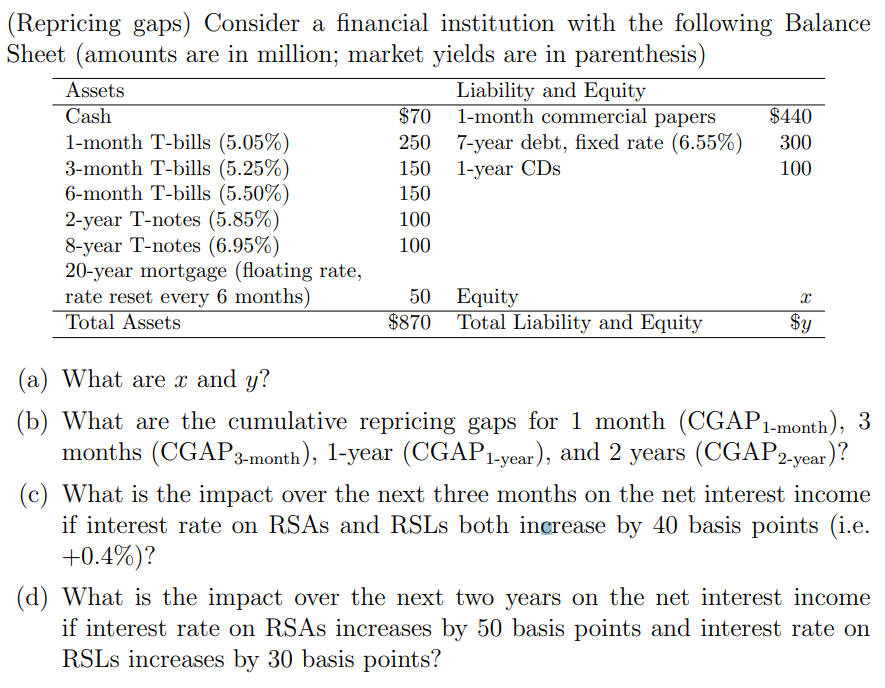

Transcribed Image Text:(Repricing gaps) Consider a financial institution with the following Balance

Sheet (amounts are in million; market yields are in parenthesis)

Assets

Liability and Equity

1-month commercial papers

Cash

1-month T-bills (5.05%)

3-month T-bills (5.25%)

6-month T-bills (5.50%)

2-year T-notes (5.85%)

8-year T-notes (6.95%)

20-year mortgage (floating rate,

rate reset every 6 months)

Total Assets

$70

$440

250 7-year debt, fixed rate (6.55%)

150 1-year CDs

300

100

150

100

100

50 Equity

$870 Total Liability and Equity

$y

(a) What are x and y?

(b) What are the cumulative repricing gaps for 1 month (CGAP1-month), 3

months (CGAP3-month), 1-year (CGAP1-year), and 2 years (CGAP2-year)?

(c) What is the impact over the next three months on the net interest income

if interest rate on RSAS and RSLS both increase by 40 basis points (i.e.

+0.4%)?

(d) What is the impact over the next two years on the net interest income

if interest rate on RSAS increases by 50 basis points and interest rate on

RSLS increases by 30 basis points?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning