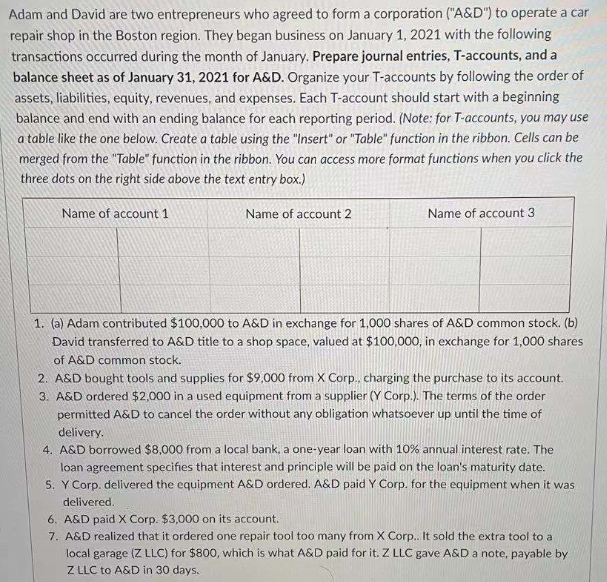

Adam and David are two entrepreneurs who agreed to form a corporation ("A&D") to operate a car repair shop in the Boston region. They began business on January 1, 2021 with the following transactions occurred during the month of January. Prepare journal entries, T-accounts, and a

Adam and David are two entrepreneurs who agreed to form a corporation ("A&D") to operate a car repair shop in the Boston region. They began business on January 1, 2021 with the following transactions occurred during the month of January. Prepare journal entries, T-accounts, and a

College Accounting (Book Only): A Career Approach

13th Edition

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:Scott, Cathy J.

Chapter3: The General Journal And The General Ledger

Section: Chapter Questions

Problem 5PA: Following is the chart of accounts of Sanchez Realty Company: Sanchez completed the following...

Related questions

Topic Video

Question

100%

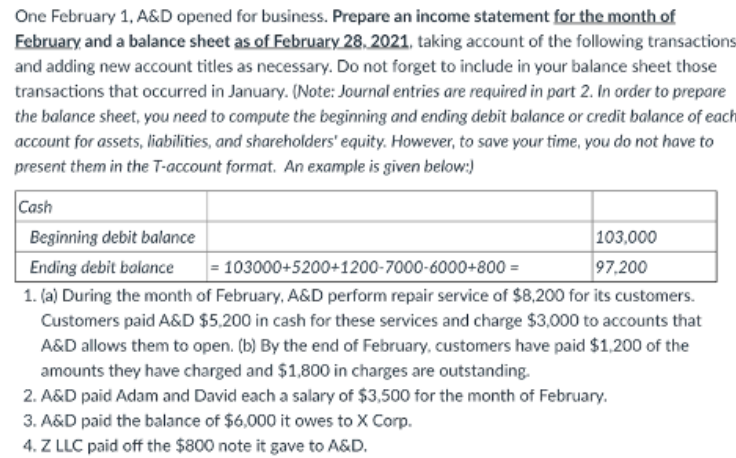

Transcribed Image Text:One February 1, A&D opened for business. Prepare an income statement for the month of

February and a balance sheet as of February 28, 2021, taking account of the following transactions

and adding new account titles as necessary. Do not forget to include in your balance sheet those

transactions that occurred in January. (Note: Journal entries are required in part 2. In order to prepare

the balance sheet, you need to compute the beginning and ending debit balance or credit balance of each

account for assets, liabilities, and shareholders' equity. However, to save your time, you do not have to

present them in the T-account format. An example is given below:)

Cash

103,000

97,200

Beginning debit balance

Ending debit balance

= 103000+5200+1200-7000-6000+800 =

1. (a) During the month of February, A&D perform repair service of $8,200 for its customers.

Customers paid A&D $5.200 in cash for these services and charge $3,000 to accounts that

A&D allows them to open. (b) By the end of February, customers have paid $1,200 of the

amounts they have charged and $1,800 in charges are outstanding.

2. A&D paid Adam and David each a salary of $3,500 for the month of February.

3. A&D paid the balance of $6,000 it owes to X Corp.

4. Z LLC paid off the $800 note it gave to A&D.

Transcribed Image Text:Adam and David are two entrepreneurs who agreed to form a corporation ("A&D") to operate a car

repair shop in the Boston region. They began business on January 1, 2021 with the following

transactions occurred during the month of January. Prepare journal entries, T-accounts, and a

balance sheet as of January 31, 2021 for A&D. Organize your T-accounts by following the order of

assets, liabilities, equity, revenues, and expenses. Each T-account should start with a beginning

balance and end with an ending balance for each reporting period. (Note: for T-accounts, you may use

a table like the one below. Create a table using the "Insert" or "Table" function in the ribbon. Cells can be

merged from the "Table" function in the ribbon. You can access more format functions when you click the

three dots on the right side above the text entry box.)

Name of account 1

Name of account 2

Name of account 3

1. (a) Adam contributed $100,000 to A&D in exchange for 1,000 shares of A&D common stock. (b)

David transferred to A&D title to a shop space, valued at $100,000, in exchange for 1,000 shares

of A&D common stock.

2. A&D bought tools and supplies for $9,000 from X Corp., charging the purchase to its account.

3. A&D ordered $2,000 in a used equipment from a supplier (Y Corp.). The terms of the order

permitted A&D to cancel the order without any obligation whatsoever up until the time of

delivery.

4. A&D borrowed $8,000 from a local bank, a one-year loan with 10% annual interest rate. The

loan agreement specifies that interest and principle will be paid on the loan's maturity date.

S. Y Corp. delivered the equipment A&D ordered. A&D paid Y Corp. for the equipment when it was

delivered.

6. A&D paid X Corp. $3,000 on its account.

7. A&D realized that it ordered one repair tool too many from X Corp.. It sold the extra tool to a

local garage (Z LLC) for $800, which is what A&D paid for it. Z LLC gave A&D a note, payable by

Z LLC to A&D in 30 days.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781305084087

Author:

Cathy J. Scott

Publisher:

Cengage Learning