Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

14th Edition

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Chapter11: Price And Output Determination: Monopoly And Dominant Firms

Section: Chapter Questions

Problem 3E

Related questions

Question

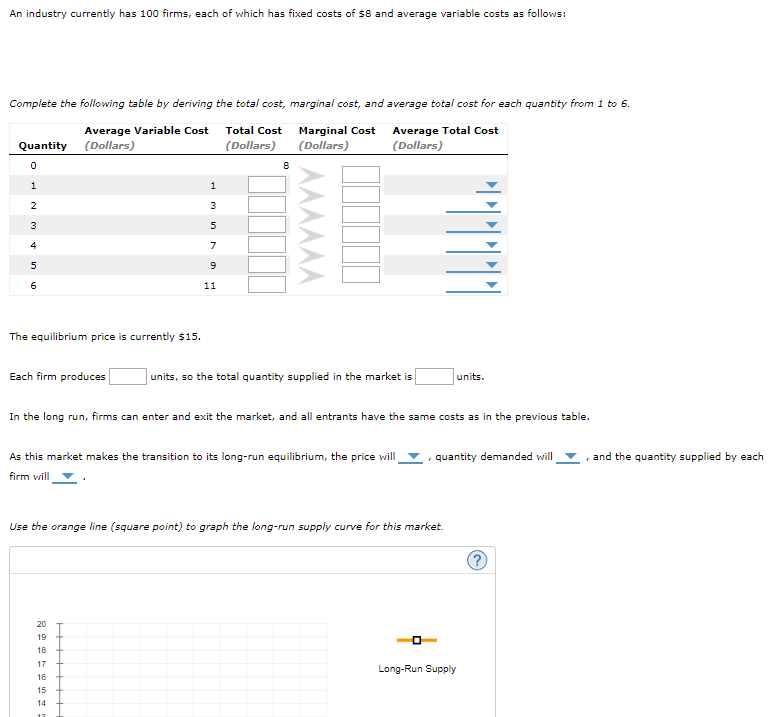

Transcribed Image Text:An industry currently has 100 firms, each of which has fixed costs of $8 and average variable costs as follows:

Complete the following table by deriving the total cost, marginal cost, and average total cost for each quantity from 1 to 6.

Average Variable Cost

(Dollars)

Total Cost

Marginal Cost

(Dollars)

Average Total Cost

(Dollars)

Quantity

(Dollars)

11

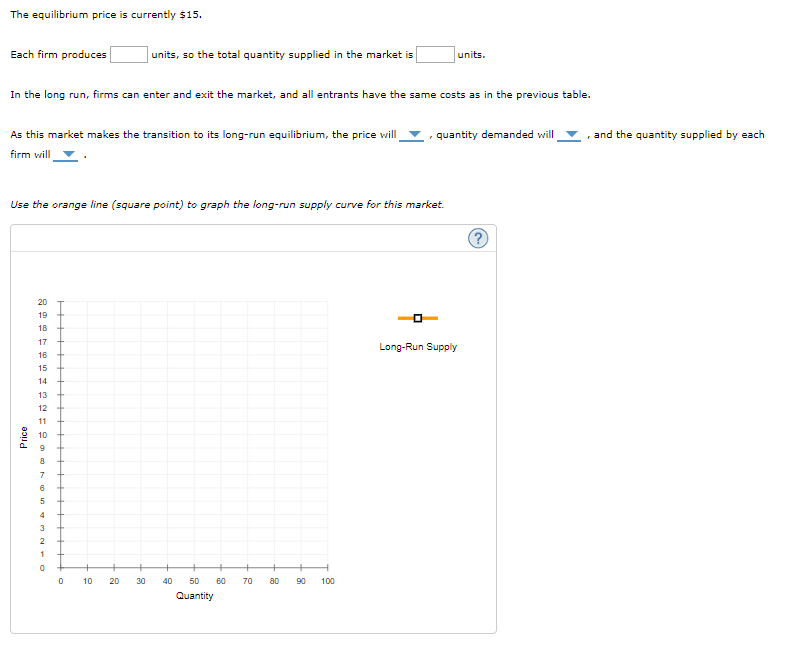

The equilibrium price is currently $15.

Each firm produces

units, so the total quantity supplied in the market is

units.

In the long run, firms can enter and exit the market, and all entrants have the same costs as in the previous table.

As this market makes the transition to its long-run equilibrium, the price will

quantity demanded will

and the quantity supplied by each

firm will

Use the orange line (square point) to graph the long-run supply curve for this market.

20

19

18

17

Long-Run Supply

16

15

14

Transcribed Image Text:The equilibrium price is currently $15.

Each firm produces

units, so the total quantity supplied in the market is

units.

In the long run, firms can enter and exit the market, and all entrants have the same costs as in the previous table.

As this market makes the transition to its long-run equilibrium, the price will

- quantity demanded will

and the quantity supplied by each

firm will

Use the orange line (square point) to graph the long-run supply curve for this market.

20

19

18

17

Long-Run Supply

16

15

14

13

12

11

10

10

20

30

40

50

60

70

80

90

100

Quantity

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 2 images

Recommended textbooks for you

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning