ANSWER IN PYTHON. THIS IS A CODING PROBLEM.

Operations Research : Applications and Algorithms

4th Edition

ISBN:9780534380588

Author:Wayne L. Winston

Publisher:Wayne L. Winston

Chapter19: Probabilistic Dynamic Programming

Section19.4: Further Examples Of Probabilistic Dynamic Programming Formulations

Problem 7P

Related questions

Question

ANSWER IN PYTHON. THIS IS A CODING PROBLEM.

![Note: The incoming trades from CBOE do not have a side field, instead the quantity

represents the side. A positive qty represents a buy and negative represents a sell.

Example:

Trade1: (date= '2022-03-15', time-9:01:00, type=Broker, qty=-500, strike-1500, expiry=¹2022-

04-28', kind=P, exchange-CBOE, trade-id=737acm, product-ABC)

Trade2: (date='2022-03-15', time-9:00:24, type=Electronic, qty=-200, strike-1500,

expiry='2022-04-28', kind-P, exchange=CBOE, trade-id=w6c229, product=ABC)

Trade3: (date = '2022-03-15', time-9:03:45, type=Electronic, qty=-100, strike-1500,

expiry='2022-04-28', kind-P, exchange=CBOE, trade-id=tssrin, product-ABC) [Fails condition

(b)]

Trade4: (date='2022-03-15', time-9:00:53, type=Electronic, qty=-500, strike-1500,

expiry='2022-04-28', Kind-P, exchange-CBOE, trade-id = Ik451a, product=XYZ) [Fails

condition (c)]

Trade5: (date='2022-03-15', time-9:00:05, type=Electronic, qty=-350, strike-1500,

expiry='2022-04-28', Kind=C, exchange-CBOE, trade-id=9numpr, product-ABC) [Fails

condition (d)]

Trade6: (date = '2022-03-15', time-9:00:35, type=Electronic, qty=200, strike-1500,

expiry='2022-04-28', Kind-P, exchange=CBOE, trade-id=922v3g, product-ABC) [Fails

condition (e)]

Trade7: (date = '2022-03-15', time-9:00:47, type=Electronic, qty=-150, strike-1500,

expiry=¹2022-04-21', Kind-P, exchange=CBOE, trade-id=bg54nm, product=ABC) [Fails

condition (f)]

Trade8: (date = '2022-03-15', time-9:02:23, type=Electronic, qty=-200, strike-1550,

expiry='2022-04-28', Kind-P, exchange=CBOE, trade-id=6y7fhm, product-ABC) [Fails

condition (g)]

Output:

[('737acm', 'w6c229')]

6 days ago](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F6d1ae07f-bdb5-47a8-9afa-ea5a04bdf9c8%2F43c92de0-327a-42e0-8540-f548acfbfad2%2F0opd3e9_processed.jpeg&w=3840&q=75)

Transcribed Image Text:Note: The incoming trades from CBOE do not have a side field, instead the quantity

represents the side. A positive qty represents a buy and negative represents a sell.

Example:

Trade1: (date= '2022-03-15', time-9:01:00, type=Broker, qty=-500, strike-1500, expiry=¹2022-

04-28', kind=P, exchange-CBOE, trade-id=737acm, product-ABC)

Trade2: (date='2022-03-15', time-9:00:24, type=Electronic, qty=-200, strike-1500,

expiry='2022-04-28', kind-P, exchange=CBOE, trade-id=w6c229, product=ABC)

Trade3: (date = '2022-03-15', time-9:03:45, type=Electronic, qty=-100, strike-1500,

expiry='2022-04-28', kind-P, exchange=CBOE, trade-id=tssrin, product-ABC) [Fails condition

(b)]

Trade4: (date='2022-03-15', time-9:00:53, type=Electronic, qty=-500, strike-1500,

expiry='2022-04-28', Kind-P, exchange-CBOE, trade-id = Ik451a, product=XYZ) [Fails

condition (c)]

Trade5: (date='2022-03-15', time-9:00:05, type=Electronic, qty=-350, strike-1500,

expiry='2022-04-28', Kind=C, exchange-CBOE, trade-id=9numpr, product-ABC) [Fails

condition (d)]

Trade6: (date = '2022-03-15', time-9:00:35, type=Electronic, qty=200, strike-1500,

expiry='2022-04-28', Kind-P, exchange=CBOE, trade-id=922v3g, product-ABC) [Fails

condition (e)]

Trade7: (date = '2022-03-15', time-9:00:47, type=Electronic, qty=-150, strike-1500,

expiry=¹2022-04-21', Kind-P, exchange=CBOE, trade-id=bg54nm, product=ABC) [Fails

condition (f)]

Trade8: (date = '2022-03-15', time-9:02:23, type=Electronic, qty=-200, strike-1550,

expiry='2022-04-28', Kind-P, exchange=CBOE, trade-id=6y7fhm, product-ABC) [Fails

condition (g)]

Output:

[('737acm', 'w6c229')]

6 days ago

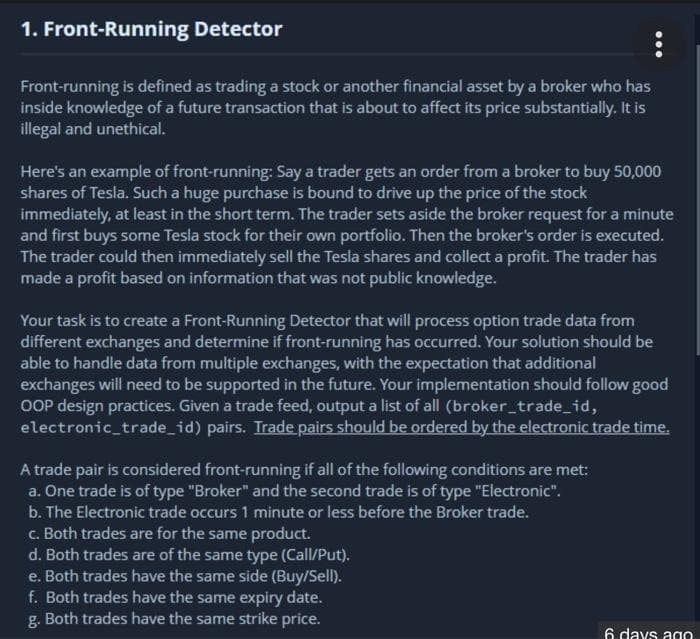

Transcribed Image Text:1. Front-Running Detector

Front-running is defined as trading a stock or another financial asset by a broker who has

inside knowledge of a future transaction that is about to affect its price substantially. It is

illegal and unethical.

Here's an example of front-running: Say a trader gets an order from a broker to buy 50,000

shares of Tesla. Such a huge purchase is bound to drive up the price of the stock

immediately, at least in the short term. The trader sets aside the broker request for a minute

and first buys some Tesla stock for their own portfolio. Then the broker's order is executed.

The trader could then immediately sell the Tesla shares and collect a profit. The trader has

made a profit based on information that was not public knowledge.

Your task is to create a Front-Running Detector that will process option trade data from

different exchanges and determine if front-running has occurred. Your solution should be

able to handle data from multiple exchanges, with the expectation that additional

exchanges will need to be supported in the future. Your implementation should follow good

OOP design practices. Given a trade feed, output a list of all (broker_trade_id,

electronic_trade_id) pairs. Trade pairs should be ordered by the electronic trade time.

A trade pair is considered front-running if all of the following conditions are met:

a. One trade is of type "Broker" and the second trade is of type "Electronic".

b. The Electronic trade occurs 1 minute or less before the Broker trade.

c. Both trades are for the same product.

d. Both trades are of the same type (Call/Put).

e. Both trades have the same side (Buy/Sell).

f. Both trades have the same expiry date.

g. Both trades have the same strike price.

6 days ago

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, computer-science and related others by exploring similar questions and additional content below.Recommended textbooks for you

Operations Research : Applications and Algorithms

Computer Science

ISBN:

9780534380588

Author:

Wayne L. Winston

Publisher:

Brooks Cole

C++ Programming: From Problem Analysis to Program…

Computer Science

ISBN:

9781337102087

Author:

D. S. Malik

Publisher:

Cengage Learning

Programming Logic & Design Comprehensive

Computer Science

ISBN:

9781337669405

Author:

FARRELL

Publisher:

Cengage

Operations Research : Applications and Algorithms

Computer Science

ISBN:

9780534380588

Author:

Wayne L. Winston

Publisher:

Brooks Cole

C++ Programming: From Problem Analysis to Program…

Computer Science

ISBN:

9781337102087

Author:

D. S. Malik

Publisher:

Cengage Learning

Programming Logic & Design Comprehensive

Computer Science

ISBN:

9781337669405

Author:

FARRELL

Publisher:

Cengage