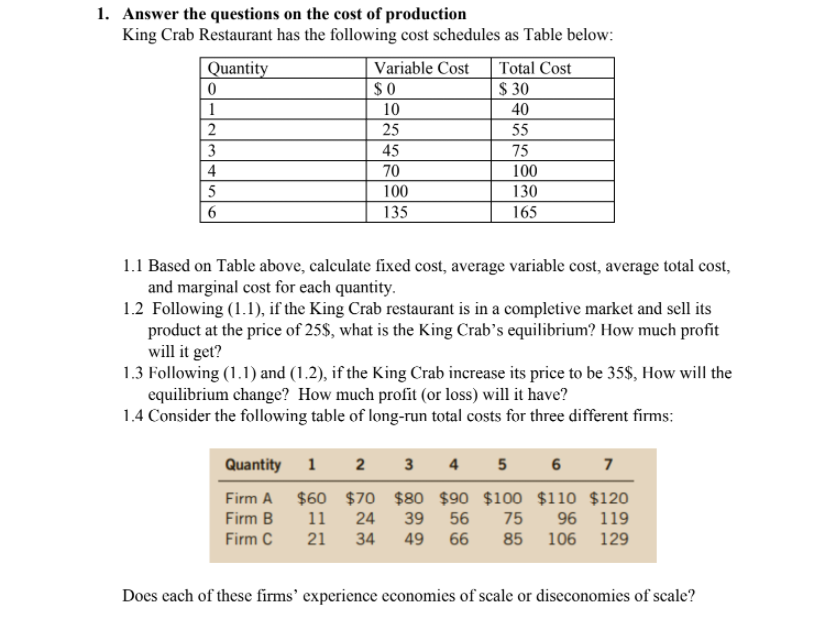

Answer the questions on the cost of production King Crab Restaurant has the following cost schedules as Table below: Quantity Variable Cost Total Cost 0 $ 0 $ 30 1 10 40 2 25 55 3 45 75 4 70 100 5 100 130 6 135 165 1.1 Based on Table above, calculate fixed cost, average variable cost, average total cost, and marginal cost for each quantity. 1.2 Following (1.1), if the King Crab restaurant is in a completive market and sells its product at the price of 25$, what is the King Crab’s equilibrium? How much profit will it get? 1.3 Following (1.1) and (1.2), if the King Crab increases its price to be 35$, How will the equilibrium change? How much profit (or loss) will it have?

Answer the questions on the cost of production

King Crab Restaurant has the following cost schedules as Table below:

Quantity Variable Cost Total Cost

0 $ 0 $ 30

1 10 40

2 25 55

3 45 75

4 70 100

5 100 130

6 135 165

1.1 Based on Table above, calculate fixed cost, average variable cost,

and marginal cost for each quantity.

1.2 Following (1.1), if the King Crab restaurant is in a completive market and sells its

product at the price of 25$, what is the King Crab’s equilibrium? How much profit

will it get?

1.3 Following (1.1) and (1.2), if the King Crab increases its price to be 35$, How will the

equilibrium change? How much profit (or loss) will it have?

1.4 Consider the following table of long-run total costs for three different firms:

Trending now

This is a popular solution!

Step by step

Solved in 2 steps