Assume that a firm in a perfectly competitive market is making a loss in the short run. In the long run, firms will [Select ] , the market [ Select ] will [ Select ] v and losses [Select ] increasing decreasing will decrease because price

Assume that a firm in a perfectly competitive market is making a loss in the short run. In the long run, firms will [Select ] , the market [ Select ] will [ Select ] v and losses [Select ] increasing decreasing will decrease because price

Chapter11: The Firm: Production And Costs

Section: Chapter Questions

Problem 21P

Related questions

Question

![Assume that a firm in a perfectly competitive market is making a loss in the

short run. In the long run, firms will [Select ]

, the market

[ Select ]

v will [Select ]

v and losses

will decrease because price iv[Select ]

increasing

decreasing](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2Fd19fb2b3-85a3-489b-9688-26d1151d3b8b%2F1446d171-86d6-481b-8cb3-6df45a6938d6%2Fqnnfsv_processed.jpeg&w=3840&q=75)

Transcribed Image Text:Assume that a firm in a perfectly competitive market is making a loss in the

short run. In the long run, firms will [Select ]

, the market

[ Select ]

v will [Select ]

v and losses

will decrease because price iv[Select ]

increasing

decreasing

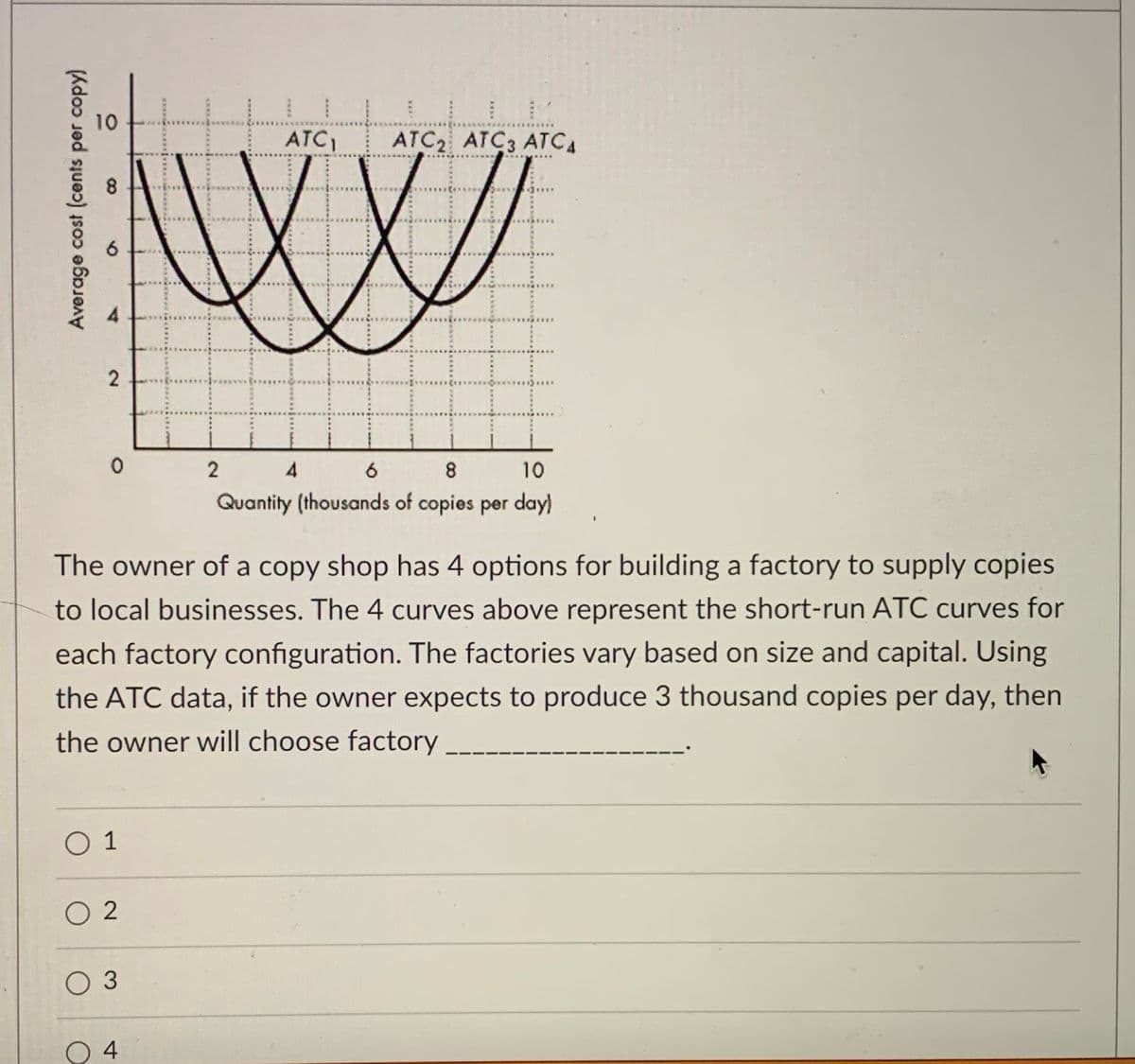

Transcribed Image Text:10

ATC

ATC2 ATC3 ATCA

6.

4

8

10

Quantity (thousands of copies per day)

The owner of a copy shop has 4 options for building a factory to supply copies

to local businesses. The 4 curves above represent the short-run ATC curves for

each factory configuration. The factories vary based on size and capital. Using

the ATC data, if the owner expects to produce 3 thousand copies per day, then

the owner will choose factory

O 1

O 2

O 3

O 4

****** *

マ

Average cost (cents per copy)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax