Assuming that joint product costs are allocated using

Principles of Cost Accounting

17th Edition

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Edward J. Vanderbeck, Maria R. Mitchell

Chapter6: Process Cost Accounting—additional Procedures; Accounting For Joint Products And By-products

Section: Chapter Questions

Problem 14E: LeMoyne Manufacturing Inc.’s joint cost of producing 2,000 units of Product X, 1,000 units of...

Related questions

Question

Subject: Cost Accounting

#16

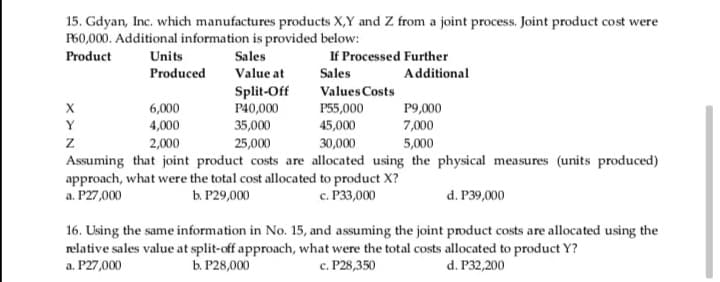

Transcribed Image Text:15. Gdyan, Inc. which manufactures products X,Y and Z from a joint process. Joint product cost were

P60,000. Additional information is provided below:

If Processed Further

Additional

Product

Units

Sales

Produced

Value at

Sales

Split-Off

P40,000

35,000

Values Costs

P55,000

45,000

30,000

Assuming that joint product costs are allocated using the physical measures (units produced)

6,000

4,000

2,000

P9,000

7,000

5,000

Y

z

25,000

approach, what were the total cost allocated to product X?

a. P27,000

b. Р29,000

с. Р3З,000

d. P39,000

16. Using the same information in No. 15, and assuming the joint product costs are allocated using the

relative sales value at split-off approach, what were the total costs allocated to product Y?

а. Р27,000

Ь Р28,000

с. Р28,350

d. Р32,200

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning