Q: Sketch a supply curve that represents the supply of salt in the short run. Explain your diagram? Add…

A: According to law of supply, the quantity supplied and the price is positively related keeping other…

Q: In the short-run, if the marginal cost of a firm in a competitive industry is upward sloping while…

A: The short-run is the time period where at least one variable is fixed and others are variable. In…

Q: Firms in a perfectly competitive market are said to be “price takers”—that is, once the market…

A: In perfect competition, there are a large number of buyers and sellers dealing with homogeneous…

Q: the new equilibrium point in the short run

A: AS curve shifts when the factors affecting aggregate supply changes. It will shift to right when the…

Q: If a retail clothing shop has to pay monthly rental of A$10,000 and has variable costs of A$20,000…

A: A firm faces different shut down constraint in different time periods such that in short-run or in…

Q: Factors that cause the short-run supply curve to change are factors that affect

A: In the short run supply can be able to change with limited resources.

Q: The long-run supply curve indifferent cost industries The following graph shows the market for milk.…

A: Answer -

Q: A firm's product sells for $4 per unit in a highly competitive market. The firm produces output…

A: The Marginal Product of Capital is the additional output when one more unit of capital is used in…

Q: Explain the concept of supply curve? Show the relationship between the Short run supply curve and…

A: The supply curve is a graph that shows the relationship between the cost of a commodity or service…

Q: Illustrate and explain how the short-run supply curve of a price-taking firm is determined.

A: In a price taking firm, the demand curve is a straight line parallel to x axis which is equal to…

Q: What is the equilibrium or profit-maximizing quantity of production for a perfectly competitive…

A: Prefect competitive market is:- 1) in perfect competitive market, there are many number of sellers…

Q: Why is it important for managers to understand the mechanics of supply and demand both in the short…

A: The terms "long run" and "short run" do not relate to a specific time period like three months or…

Q: In the short run, each firm experiences a loss of $

A: We know , Profit = TR - TC TR = Price * Quantity TR = 100 *50 TR = 5000 ATC = TCQ TC = ATC * Q TC…

Q: What determines the slope of the Market Supply Curve over the long run? Discuss some reasons why it…

A: The market supply bend/curve is an upward sloping bend portraying the positive connection between…

Q: Jackson Hardware, a firm in the perfectly competitive custom hardware industry, asks you for your…

A: A perfectly competitive firm is a price taker and can sell any quantity of the commodity at the…

Q: A firm in a perfectly competitive market uses only workers to produce output. The relationship…

A: Answer: Given, Wages (variable cost) = $100 per worker Fixed cost = $500 (a). The formula to be…

Q: (The Short-Run Firm Supply Curve) Use the following data to answer the questions below: Quantity…

A: (a) we can calculate marginal cost and average variable cost by using the following equations.…

Q: The following graph shows the market demand for wheat. 1. Use the orange points (square symbol) to…

A: In perfect competition, the short-run supply curve is the rising part of the MC curve above the…

Q: You are operating in a perfect market are you are price taker? Why?

A: The perfect competitive market is a type of market, which is characterized by a large number of…

Q: Family Mart like inner city grocery stores, sometimes exist even though they do not earn economic…

A: Hi Student, thanks for posting the question. As per the guideline we are providing answers for the…

Q: Explain why profit is greatest at this rate of output If fixed costs were $10 higher than those…

A: Producers objective is to maximize his or her profit . And The profit gets Maximized at the level of…

Q: What is the relationship between marginal cost and the short-run supply curve for the purely…

A: Supply curve is the graphical representation of direct relationship between price and quantity…

Q: Explain the following quotations; 1. " Greater production is not tantamount to greater profit" 2.…

A: In the field of economics, it is assumed that firms work towards maximizing profits. The profits of…

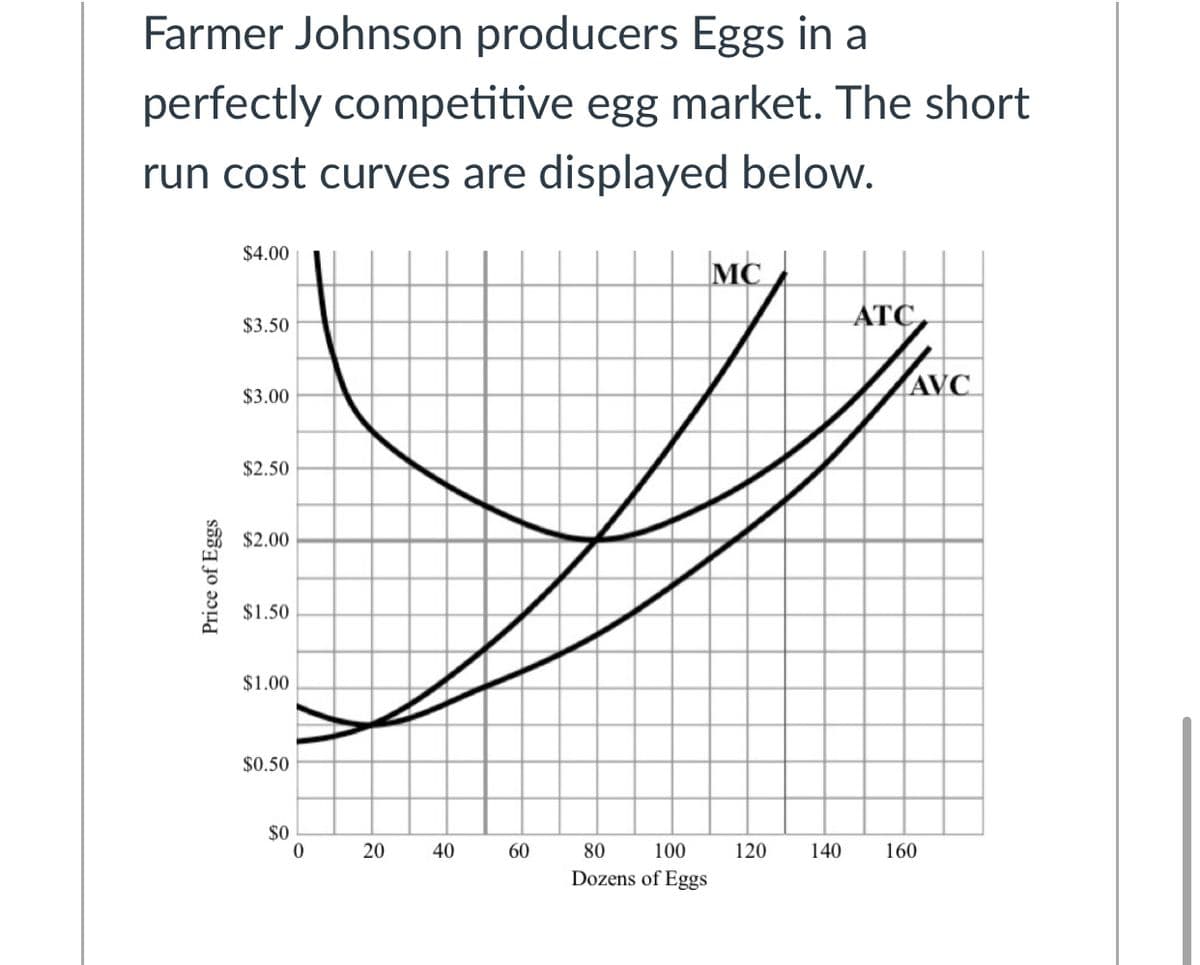

Q: The graph shows the cost curves for a perfectly competitive firm. If the market price of the product…

A: A perfectly competitive market is where there are large number of buyers and sellers. The price of…

Q: If the pandemic causes firms in a competitive industry to spend $100,000 per month on safety…

A: If the pandemic causes firms in a competitive industry to spend $100,000 per month on safety…

Q: Consider a firm that is currently producing a level of output that maximizes its profits. The firm…

A: Given: Revenue of the firm = $40 million per month. Worker Compensation = $30 million Renting of…

Q: For a perfectly competitive firm to operate and produce an output level in the short-run, the firm's…

A: A perfectly competitive market is a price taker as there are many firms in the market and no firm…

Q: A new korean restaurant opens in a city. People are initially cautious about eating new food items,…

A: Perfectly competitive market: - it is a market condition where there are many buyers and many…

Q: Fill in the blank: In the long run, maximizing profits is different from minimizing costs as the…

A: In a market, there are some differences in dealing the market condition in the short-run and in the…

Q: Which of the following is NOTa short run decision that a firm faces? (ר "If sales are not good,…

A: Answer to the question is as follows:

Q: In the short run, the firm should continue to produce if and only if a.Price exceeds average total…

A: Total fixed cost is independent of output produced whereas variable cost varies with the level of…

Q: Explain the profit and loss possibilities of a price taker firm and graphically draw the supply…

A: Long-run is the time period where all the factors of production become variable.

Q: Productive efficiency and allocative efficiency are two concepts achieved in the long run in a…

A: Perfect competition is a competition where the firms in the market are price takers and have no…

Q: What is most likely to increase the total output of a firm in the short run? A a rise in the length…

A: Hi! Thank you for the question. As per the honor code, We’ll answer the first question since the…

Q: Consider the perfectly competitive market for steel, which is in long-run equilibrium. Now the…

A: Perfectly competitive market- It is a market where there are large numbers of buyers and sellers and…

Q: Briefly define the short run and long run supply curve?

A: The supply curve is a graphical representation that describes the relationship between the price and…

Q: Which of the following is not a characteristic of a perfectly competitive market? a. There is a…

A: Perfectly Competitive Market: In terms of economics, Perfect competition is a form of market…

Q: All the supply of peppermint oil is produced from mint plants grown in one county by several…

A: In a market, supply of output depends upon various factors such as price, availability of resources,…

Q: Distinguish between short-run and long-run supply curves.

A: Short run refers to a period of time during which some manufacturing elements are constant while…

Q: “That segment of a competitive firm’s marginal-cost curve that lies above its average-variable-cost…

A:

Q: Consider the perfectly competitive market for tofu. Tofu production requires special inspections…

A: Introduction: Pure or perfect competition is a theoretical market structure in which the following…

Q: The following graph shows the long-run supply curve for persimmons. Place the orange line (square…

A: "Supply curve for a product depicts a positive relationship between the price of the product and…

Q: What is the short run Supply Curve for a competitive firm?

A: In perfect competition, the short-run supply curve is the marginal cost curve (MC) at and below the…

Q: Utilize the graph above, which illustrates average fixed costs, average variable costs, average…

A: The given graph below highlights the perfectly competitive market Therefore I represents Average…

Q: Use the graphs below to answer the following questions. $1b $/gal S1 25E 25E MC S2 ATC 20 20 15 15…

A:

Q: Choose the statement that is true. Fixed costs in the long run can become variable in the short run.…

A: Out of the given statements, only the fourth statement is true. The reason for this is explained…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

- Why will losses for firms in a perfectly competitive industry tend to vanish in the long run?What two rules does a perfectly competitive firm apply to determine its profit-maximizing quantity of output?Fabulous Farms operates in a perfectly competitive market. Which of the following is required for Fabulous Farms to both maximize profits and achieve allocative efficiency? A P = MC B P > MC C P < MC D P = MC – MR

- he following problem traces the relationship between firm decisions, market supply, and market equilibrium in a perfectly competitive market. Complete the cost table below. (Round your responses to two decimal places.) q TFC TVC TC AVC ATC MC 0 $4040 $0 $4040 long dash— long dash— long dash— 1 4040 125125 165165 125125 165165 125125 2 4040 167167 207207 83.583.5 103.5103.5 4242 3 4040 195195 235235 6565 78.3378.33 2828 4 4040 209209 249249 52.2552.25 62.2562.25 1414 5 4040 237237 277277 47.447.4 55.455.4 2828 6 4040 279279 319319 46.546.5 53.1753.17 4242 7 4040 335335 375375 47.8647.86 53.5753.57 5656 8 4040 405405 445445 50.6350.63 55.6355.63 7070 9 4040 489489 529529 54.3354.33 58.7858.78 8484 10 4040 587587 627627 58.758.7 62.762.7 9898 Using the…Cost figures for a hypothetical firm are given in the following table. Use them for the exercises below. The firm is selling in a perfectly competitive market. Output Fixed AFC Variable AVC Total ATC MC Cost Cost cost 1 $50 50/1=50 $30 30/1=30 30+50=80 80/1=80 NA 2 $50 50/2=25 $50 50/2=25 50+50=100 100/2=50 (100-80)/(2-1)=20 3 $50 50/3=16.67 $80 80/3=26.67 50+80=130 130/3=43.33 (130-100)/(3-2)=30 4 $50 50/4=12.50 $120 120/4=30 50+120=170 170/4=42.50 (170-130)/(4-3)=40 5 $50 50/5=10 $170 170/5=34 50+170=220 220/5=44 (220-170)/(5-4) =50 What can you expect from an industry in perfect competition in the long run? That is, what will the price be? What quantity will be produced? What will be the relation between marginal cost, average cost, and price?The market for fertilizer is perfectly competitive.Firms in the market are producing output but arecurrently incurring economic losses.a. How does the price of fertilizer compare to theaverage total cost, the average variable cost, andthe marginal cost of producing fertilizer?b. Draw two graphs, side by side, illustrating thepresent situation for the typical firm and for themarket.c. Assuming there is no change in either demand orthe firms’ cost curves, explain what will happenin the long run to the price of fertilizer, marginalcost, average total cost, the quantity supplied byeach firm, and the total quantity supplied to themarket.

- Suppose that the market for chicken momos is perfectly competitive with ten firms producing momos. Tasty treat is one of the ten price-takers in the market for momos. The accompanying tables show the demand schedule for momos in Dhaka and cost schedule for "Tasty Treat". DEMAND SCHEDULE Price (BDT per plate) Quantity demanded (plate per hour) 10 900 25 675 30 600 40 450 50 300 70 0 COST SCHEDULE OF TASTY TREAT Output (plate per hour) Marginal Cost (BDT per extra plate) Average Variable Cost (BDT per plate) Average total cost (BDT per plate) 40 20 25 90 50 10 10 75 60 30 20 55 70 50 23 50 80 70 35 60 90 85 50 77 a) What is the value of the shut-down price and break-even price for Tasty Treat?How did you figure that out?b) Write down the individual supply schedule of chicken momos for Tasty Treat and the industry supply schedule for chicken momos.c) Plot the market demand and supply curves for chicken momos and find the equilibrium price and…Assume that Harry Ellis produces table lamps in the perfectly competitive table lamp market. OUTPUT PER WEEK TOTAL COSTS AFC AVC ATC MC 0 $100 1 150 2 175 3 190 4 210 5 240 6 280 7 330 8 390 9 460 10 540 Fill in the missing values in the table. Suppose the equilibrium price in the table lamp market is $50. How many table lamps should Harry produce, and how much profit will he make? If next week the equilibrium price of table lamps drops to $30, should Harry shut down?Will a perfectly competitive market display allocative efficiency? Why or why not?

- How a firm respond to economy profits and economy losses in perfectly competitive market?Assume that the cost data in the following table are for a purely competitive producer: TotalProduct AverageFixed Cost AverageVariable Cost AverageTotal Cost Marginal Cost 0 1 $60.00 $45.00 $105.00 $45.00 2 30.00 42.50 72.50 40.00 3 20.00 40.00 60.00 35.00 4 15.00 37.50 52.50 30.00 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 7 8.57 38.57 47.14 45.00 8 7.50 40.63 48.13 55.00 9 6.67 43.33 50.00 65.00 10 6.00 46.50 52.50 75.00 Instructions: If you are entering any negative numbers be sure to include a negative sign (−) in front of those numbers. Select "Not applicable" and enter a value of "0" for output if the firm does not produce. a. At a product price of $56.00 (i) Will this firm produce in the short run? (Click to select) No Yes (ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output? (Click to select) Not applicable Loss-minimizing…Assume that the cost data in the following table are for a purely competitive producer: TotalProduct AverageFixed Cost AverageVariable Cost AverageTotal Cost Marginal Cost 0 1 $ 60.00 $ 45.00 $ 105.00 $ 45.00 2 30.00 42.50 72.50 40.00 3 20.00 40.00 60.00 35.00 4 15.00 37.50 52.50 30.00 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 7 8.57 38.57 47.14 45.00 8 7.50 40.63 48.13 55.00 9 6.67 43.33 50.00 65.00 10 6.00 46.50 52.50 75.00 a. At a product price of $56.00 (i) Will this firm produce in the short run? yes (ii) If it is preferable to produce, what will be the profit-maximizing or loss-minimizing output? profit- maximizing output = 9 units per firm (iii) What economic profit or loss will the firm realize per unit of output? Profit per unit = $ 16 b. At a product price of $41.00 (i) Will this firm produce in the short run? Yes (ii) If it is preferable to produce, what will be the…