B. Making the entries in the ledger.

Chapter4: The Adjustment Process

Section: Chapter Questions

Problem 15PA: Prepare an adjusted trial balance from the following account information, considering the adjustment...

Related questions

Question

B.)

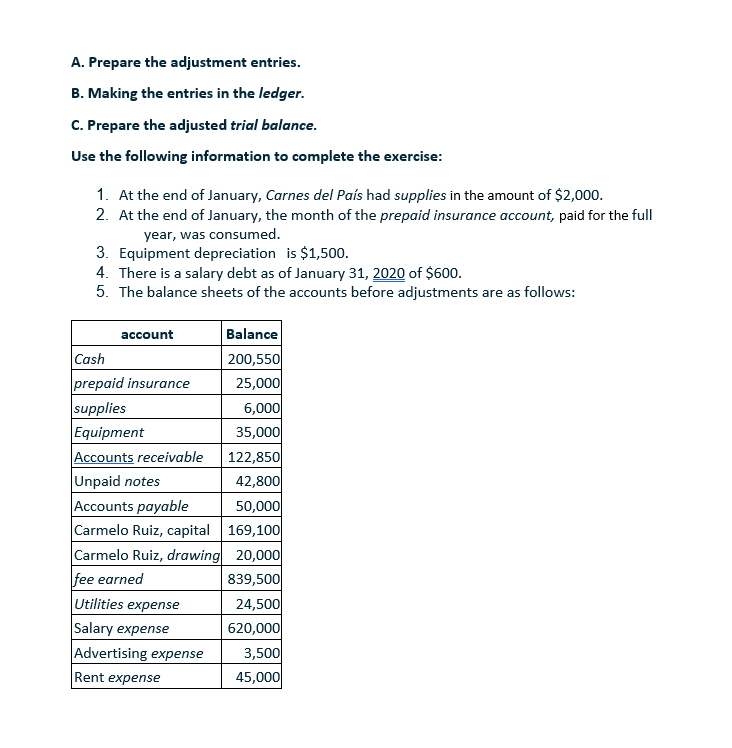

Transcribed Image Text:A. Prepare the adjustment entries.

B. Making the entries in the ledger.

C. Prepare the adjusted trial balance.

Use the following information to complete the exercise:

1. At the end of January, Carnes del País had supplies in the amount of $2,000.

2. At the end of January, the month of the prepaid insurance account, paid for the full

year, was consumed.

3. Equipment depreciation is $1,500.

4. There is a salary debt as of January 31, 2020 of $600.

5. The balance sheets of the accounts before adjustments are as follows:

account

Balance

Cash

200,550

25,000

prepaid insurance

supplies

Equipment

Accounts receivable

Unpaid notes

Accounts payable

Carmelo Ruiz, capital 169,100

Carmelo Ruiz, drawing 20,000

fee earned

Utilities expense

Salary expense

6,000

35,000

122,850

42,800

50,000

839,500

24,500

620,000

Advertising expense

Rent expense

3,500

45,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage