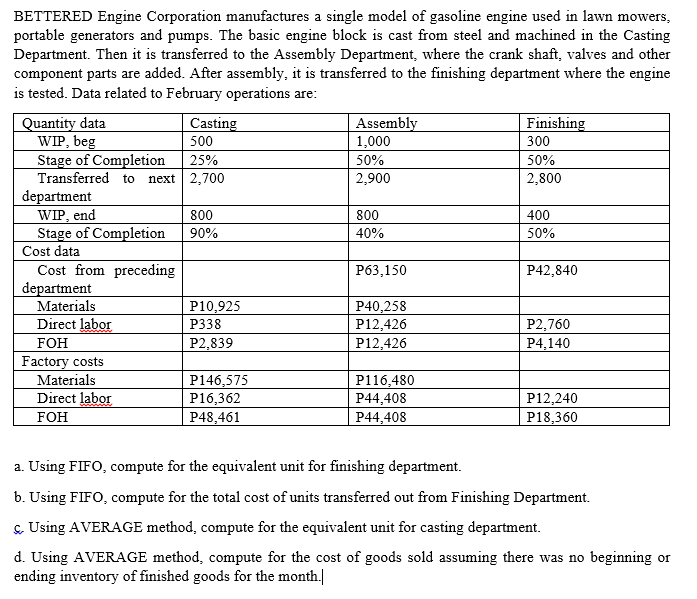

BETTERED Engine Corporation manufactures a single model of gasoline engine used in lawn mowers, portable generators and pumps. The basic engine block is cast from steel and machined in the Casting Department. Then it is transferred to the Assembly Department, where the crank shaft, valves and other component parts are added. After assembly, it is transferred to the finishing department where the engine is tested. Data related to February operations are: Quantity data WIP, beg Stage of Completion Transferred to next 2,700 Assembly 1,000 Casting 500 Finishing 300 25% 50% 50% 2,900 2,800

Q: The following information is available for Twinny Corporation for the month of Ma: Started in…

A: FIFO Inventory Valuation method:- In this method, valuation of inventory done on a FIFO basis( First…

Q: Lubricants, Inc., produces a special kind of grease that is widely used by race car drivers. The…

A: Part 1 Journal Entries - Lubricants Inc. Transaction No Particulars Debit ($) Credit ($) a…

Q: Frankle Manufacturing produces cylinders used in internal combustion engines. During June, Frankle’s…

A: Introduction: Production is the process of merging numerous material and immaterial inputs to create…

Q: XYZ Engine Corporation manufactures a single model of gasoline engine used in lawn mowers, portable…

A:

Q: Arona Corporation manufactures canoes in two departments, Fabrication and Waterproofing. In the…

A: An equivalent unit of production is an expression of the work done by a manufacturer on partially…

Q: BETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: Under the average method, the total cost incurred till date is divided by the total equivalent units…

Q: Balkan Bhd, manufatures a caulking compound that goes through three processing stage prior to…

A: The potential investor is the person who put the money into the investment. The person who invests…

Q: Work in Process—Refining Department March 1 balance 33,600 Completed and transferred to Blending ?…

A: Solution No General Journal Debit Credit A Work-in-Progress Inventory Refining 156600…

Q: ETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: Solution: Equivalent unit for Casting = Units Transferred to next Dept*100% + WIP end*90%

Q: Two-Stage ABC for Manufacturing Assume Sherwin-Williams Company, a large paint manufacturer, has…

A:

Q: Calculate the Packaging Department’s equivalent units for transferred-in, direct materials and…

A: Input details Units Output details Units Equivalent units Material Conversion cost % Units %…

Q: attached to a canoe- shaped aluminum frame. The canoes are then transferred to the Waterproofing…

A: Under cost accounting, the equivalent units are those units in the production that is multiplied…

Q: The Matis Manufacturing Company manufactures a single product in two producing departments. For the…

A:

Q: Lubricants, Inc., produces a special kind of grease that is widely used by race car drivers. The…

A: Cost accounting is the branch of accounting that inspects the cost structure of a business. This…

Q: The Matis Manufacturing Company manufactures a single product in two producing departments. For the…

A:

Q: Peter Company manufactures a product in three processes: Cutting, , and Packaging. In the Packaging…

A: Solution: Equivalent units for materials using FIFO method = Beginning units*100% + units started…

Q: Carson Paint Company, which manufactures quality paint to sell at premium prices, uses a single…

A: The total cost of producing a product, including raw materials and operating costs, is detailed in a…

Q: BETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: The question has multiple sub-parts, so first 3 sub-parts shall be answered. Under the average…

Q: Arona Corporation manufactures canoes in two departments, Fabrication and Waterproofing. In the…

A: When beginning and ending inventory of work in progress exist, units costs can not be determined by…

Q: Xavier Corporation manufactures a plastic toy product in a two-stage production process. Plastic…

A: Equivalent Units: An equivalent unit of production is an indication of the amount of work done by…

Q: Becton Labs, Inc., produces various chemical compounds for industrial use. One compound, called…

A: The variance is computed by comparing standard cost and actual cost. The standards are settled on…

Q: Waterway Processing Company uses a weighted-average process cost system and manufactures a single…

A:

Q: Becton Labs, Inc., produces various chemical compounds for industrial use. One compound, called…

A: Variance Analysis: Variance analysis is the study of variations between actual and projected or…

Q: Pant Risers manufactures bands for self-dressing assistive devices for mobility-impaired…

A: The question is based on the concept of Cost Accounting.

Q: Brite ideas Inc mass produces reading lamps. Materials used in constructing the body of the lamp are…

A: Compute the units started and completed in June.

Q: Peter Company manufactures a product in three processes: Cutting, Assembly, and Packaging. In the…

A: Answer is Option a) 10,250

Q: Jennie Electric manufactures several products, including an electric garage door opener called the…

A: The equivalent units are calculated on the basis of percentage of work completed during the period.…

Q: Ridgecrest Company manufactures plastic storage crates and has the following information available…

A: Formulas for the above table:

Q: Cullumber Company manufactures basketballs. The first step is the production of internal rubber…

A: Equivalent Units of Production: As defined by the International Accounting Standards (IAS), an…

Q: Honeybutter, Inc., manufactures a product that goes through two departments prior to comple-…

A:

Q: Venti Chemicals has a Mixing Department and a Refining Department. Its process-costing system in the…

A: Equivalent units of products concept came in to existence when some units are not fully completed at…

Q: Zeus Corporation produces cultured diamonds via a secretive process that grows the diamonds in a…

A: Cost allocation is the process of distributing costs to various cost drivers.

Q: Glencove Co. makes one model of radar gun used by law enforcement officers. All direct materials are…

A: Using the formulas given below we can determine the cost and inventory units:

Q: ETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: Solution: Units started and completed for finishing = total units transferred out - WIP beg units =…

Q: Schoen Corp. manufactures three types of electrical motors. Type A is sold upon completion of the…

A: In the above question, firstly we have to find total profit if product B are not sent for further…

Q: BETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: Calculation of equivalent units using average method for casting department

Q: Lubricants, Inc., produces a special kind of grease that is widely used by race car drivers. The…

A: 1. Prepare journal entries to record costs incurred in both refining department and blending…

Q: Woolens Corp. manufactures bolts of wool cloth. The wool cloth is cut and manufactured in the…

A: Step 1 Equivalent units of production are applied to the work-in-process inventory at the end of an…

Q: he Mountain Springs Water Company has two departments, Purifying and Bottling. The Bottling…

A: First in first out means that any stock which is purchased first are sold out first or in other…

Q: BETTERED Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: Although it has the multiple sub-parts, but the answer is specifically required for part b. The…

Q: Terry Linens Inc. manufactures bed and bath linens. The bath linens department sews terry cloth into…

A: Under weighted-average method, units completed and transferred out are 100% complete with respect to…

Q: Dover Chemical Company manufactures specialty chemicals by a series of three processes, all…

A: Cost Production Report is prepared to allocate the cost incurred during the period to beginning…

Q: i cannot figure out how to solve this problem

A: a. Reconciliation of the number of physical units worked on during the period:

Q: MediSecure, Inc., produces clear plastic containers for pharmacies in a process that starts in the…

A: First-in-First-Out (FIFO): In this method, items purchased initially are sold first. So, the value…

Q: Brightmore Corporation manufactures three styles of lighting fixtures using five sequential…

A: The problem contains two subparts. We have to calculate the total cost of work completed and the…

Q: Ridgecrest Company manufactures plastic storage crates and has the following information available…

A: Process costing is a method used to allocate and trace the direct costs and conversion costs to the…

Q: BETTERER Engine Corporation manufactures a single model of gasoline engine used in lawn mowers,…

A: The solution would involve the preparation of production costs reports for the Casting, Assembly,…

Q: Dover Chemical Company manufactures specialty chemicals by a series of three processes, all…

A: The equivalent units are calculated on the basis of percentage of the work completed during the…

Please show your computations through excel.

d. Using AVERAGE method, compute for the cost of goods sold assuming there was no beginning or ending inventory of finished goods for the month.

Step by step

Solved in 3 steps with 2 images

- Golding Manufacturing, a division of Farnsworth Sporting, Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handle. The limbs pass through four sequential processes before reaching final assembly: lay-up, molding, fabricating, and finishing. In the Lay-Up Department, limbs are created by laminating layers of wood. In Molding, the limbs are heat treated, under pressure, to form a strong resilient limb. In the Fabricating Department, any protruding glue or other processing residue is removed. Finally, in Finishing, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the Pattern Department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the Finishing Department where they are sprayed with the final finishes. In Final Assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80 percent of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: KAREN: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in direct material input. AARON: Your predecessor is responsible. He believed that tracking the difference in direct material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. KAREN: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the Pattern Department. The other departments fit what I view as a process-costing pattern. AARON: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the Pattern Department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no beginning work in process; however, there were 300 units in ending work in process: 200 Deluxe and 100 Econo models. Both models were 80 percent complete with respect to conversion costs and 100 percent complete with respect to direct materials. c. The Pattern Department experienced the following costs: d. On an experimental basis, the requisition forms for direct materials were modified to identify the dollar value of the direct materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the Pattern Department, assuming that process costing is totally appropriate. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price less manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?Golding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: Karen: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input. Aaron: Your predecessor is responsible. He believed that tracking the difference in material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. Karen: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern. Aaron: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials. c. The pattern department experienced the following costs: d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the pattern department, assuming that process costing is totally appropriate. Round unit cost to two decimal places. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. Round unit cost to two decimal places. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?Heap Company manufactures a product that passes through two processes: Fabrication and Assembly. The following information was obtained for the Fabrication Department for September: a. All materials are added at the beginning of the process. b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs. c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs. d. Started in process, 95,000 units. Required: 1. Prepare a physical flow schedule. 2. Compute equivalent units using the weighted average method. 3. Compute equivalent units using the FIFO method.

- Lacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Materials are added at the beginning of the process. Overhead is applied using the following drivers and activity rates: Other data for the Plate Cutting Department are as follows: Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production for: a. Direct materials b. Conversion costs 3. Calculate unit costs for: a. Direct materials b. Conversion costs c. Total manufacturing 4. Provide the following information: a. The total cost of units transferred out b. The journal entry for transferring costs from Plate Cutting to Welding c. The cost assigned to units in ending inventoryUsing the same data found in Exercise 6.22, assume the company uses the FIFO method. Required: Prepare a schedule of equivalent units, and compute the unit cost for the month of December. Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000.Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.

- Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use. Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength. In 20X1, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plantsone in Arizona and one in New Mexicoa suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant. The Arizona facilities had been in operation for more than a decade and were full of WIP. The New Mexico facility had been operational for only 2 years and had much smaller WIP inventories. The partner located in New Mexico argued that to disregard the unequal value of the WIP inventories would be grossly unfair. Unfortunately, during the entire business history of AKL Foundry, WIP inventories had never been assigned any value. In computing the cost of goods sold each year, the company had followed the policy of adding depreciation to the out-of-pocket costs of direct labor, direct materials, and overhead. Accruals for the company are nearly nonexistent, and there are hardly ever any ending inventories of materials. During 20X1, the Arizona plant had sales of 2,028,670. The cost of goods sold is itemized as follows: Upon request, the owners of AKL provided the following supplementary information (percentages are cumulative): Gating had 10,000 units in BWIP, 60% complete. Assume that all materials are added at the beginning of each process. During the year, 50,000 units were completed and transferred out. The ending inventory had 11,000 unfinished units, 60% complete. Required: 1. The partners of AKL want a reasonable estimate of the cost of WIP inventories. Using the gating departments inventory as an example, prepare an estimate of the cost of the EWIP. What assumptions did you make? Did you use the FIFO or weighted average method? Why? (Note: Round unit cost to two decimal places.) 2. Assume that the shell-creating process has 8,000 units in BWIP, 20% complete. During the year, 50,000 units were completed and transferred out. (Note: All 50,000 units were sold; no other units were sold.) The EWIP inventory had 8,000 units, 30% complete. Compute the value of the shell-creating departments EWIP. What additional assumptions had to be made?Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below. Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity. Other overhead activities, their costs, and drivers are listed below. Other production information concerning the two hydraulic cylinders is also provided: Required: 1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost. 2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate. 3. Calculate the global consumption ratios. 4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification. 5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.

- Novel Toys, Inc., manufactures plastic water guns. Each guns left and right frames are produced in the Molding Department. The left and right frames are then transferred to the Assembly Department where the trigger mechanism is inserted and the halves are glued together. (The left and right halves together define the unit of output for the Molding Department.) In June, the Molding Department reported the following data: a. In the Molding Department, all direct materials are added at the beginning of the process. b. Beginning work in process consisted of 3,000 units, 20 percent complete with respect to direct labor and overhead. Costs in beginning inventory included direct materials, 450; and conversion costs, 138. c. Costs added to production during the month were direct materials, 950; and conversion costs, 2,174.50. d. Inspection takes place at the end of the process. Malformed units are discarded. All spoilage is considered abnormal. e. During the month, 7,000 units were started, and 8,000 good units were transferred out to Finishing. All other units finished were malformed and discarded. There were 1,000 units that remained in ending work in process, 25 percent complete. Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production using the weighted average method. 3. Calculate the unit cost. 4. What is the cost of goods transferred out? Ending work in process? Loss due to spoilage? 5. Prepare the journal entry to remove spoilage from the Molding Department.K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.Handy Leather, Inc., produces three sizes of sports gloves: small, medium, and large. A glove pattern is first stencilled onto leather in the Pattern Department. The stenciled patterns are then sent to the Cut and Sew Department, where the glove is cut and sewed together. Handy Leather uses the multiple production department factory overhead rate method of allocating factory overhead costs. Its factory overhead costs were budgeted as follows: The direct labor estimated for each production department was as follows: Direct labor hours are used to allocate the production department overhead to the products. The direct labor hours per unit for each product for each production department were obtained from the engineering records as follows: a. Determine the two production department factory overhead rates. b. Use the two production department factory overhead rates to determine the factory overhead per unit for each product.