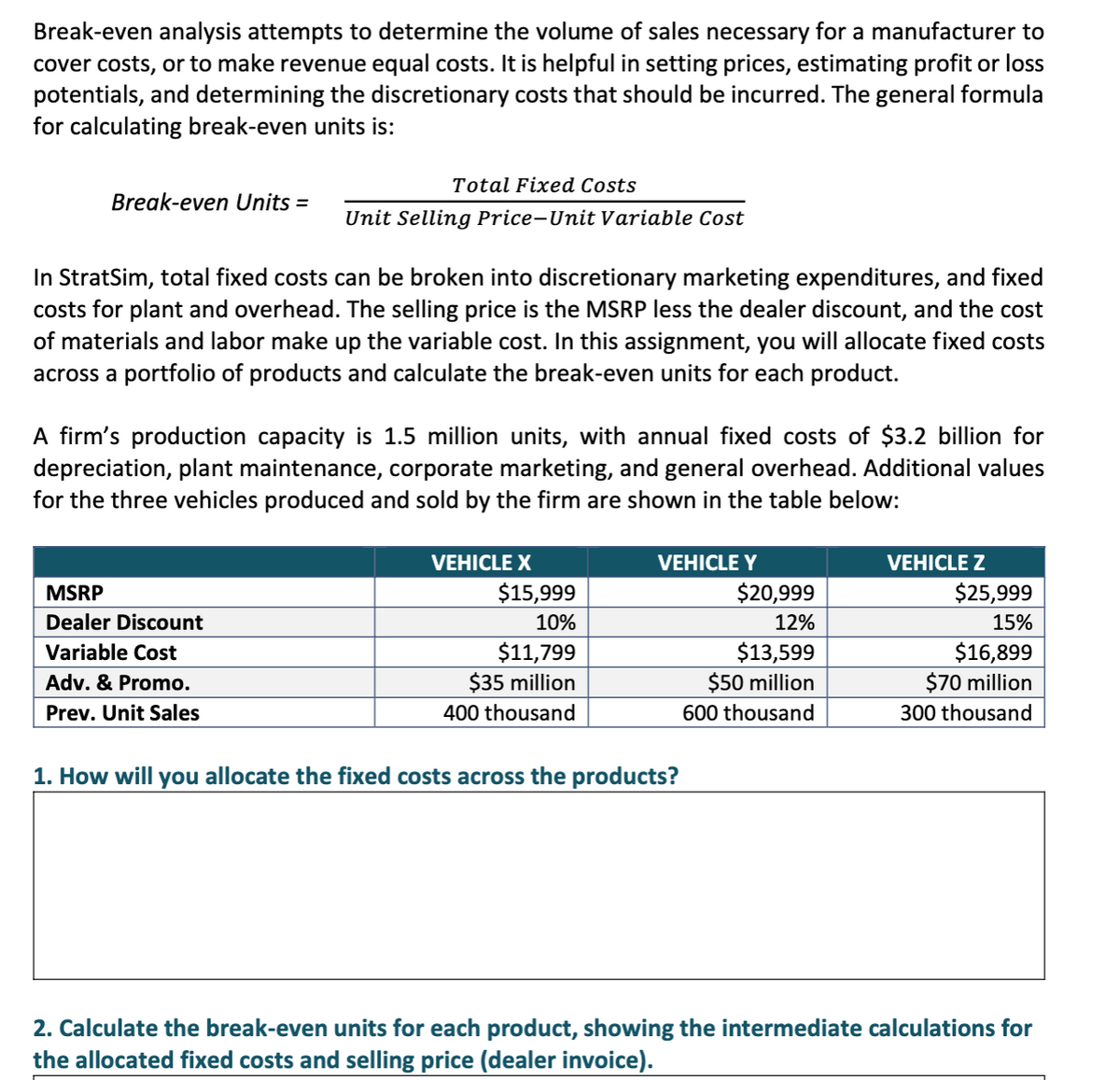

Break-even analysis attempts to determine the volume of sales necessary for a manufacturer to cover costs, or to make revenue equal costs. It is helpful in setting prices, estimating profit or loss potentials, and determining the discretionary costs that should be incurred. The general formula for calculating break-even units is: Total Fixed Costs Break-even Units = Unit Selling Price-Unit Variable Cost In StratSim, total fixed costs can be broken into discretionary marketing expenditures, and fixed costs for plant and overhead. The selling price is the MSRP less the dealer discount, and the cost of materials and labor make up the variable cost. In this assignment, you will allocate fixed costs across a portfolio of products and calculate the break-even units for each product. A firm's production capacity is 1.5 million units, with annual fixed costs of $3.2 billion for depreciation, plant maintenance, corporate marketing, and general overhead. Additional values for the three vehicles produced and sold by the firm are shown in the table below: VEHICLE X VEHICLE Y VEHICLE Z MSRP $15,999 $20,999 $25,999 Dealer Discount 10% 12% 15% $11,799 $35 million $13,599 $50 million $16,899 $70 million Variable Cost Adv. & Promo. Prev. Unit Sales 400 thousand 600 thousand 300 thousand 1. How will you allocate the fixed costs across the products? 2. Calculate the break-even units for each product, showing the intermediate calculations for the allocated fixed costs and selling price (dealer invoice).

Process Costing

Process costing is a sort of operation costing which is employed to determine the value of a product at each process or stage of producing process, applicable where goods produced from a series of continuous operations or procedure.

Job Costing

Job costing is adhesive costs of each and every job involved in the production processes. It is an accounting measure. It is a method which determines the cost of specific jobs, which are performed according to the consumer’s specifications. Job costing is possible only in businesses where the production is done as per the customer’s requirement. For example, some customers order to manufacture furniture as per their needs.

ABC Costing

Cost Accounting is a form of managerial accounting that helps the company in assessing the total variable cost so as to compute the cost of production. Cost accounting is generally used by the management so as to ensure better decision-making. In comparison to financial accounting, cost accounting has to follow a set standard ad can be used flexibly by the management as per their needs. The types of Cost Accounting include – Lean Accounting, Standard Costing, Marginal Costing and Activity Based Costing.

Trending now

This is a popular solution!

Step by step

Solved in 5 steps