Q: Identify the cash flow series associated with production or service over thelife of the asset?

A: Definition: Cash inflows: The amount of cash received by a company from the operating, investing,…

Q: Which capital investment methods require the use of a present value table?

A: Net Present Value: It is a measure of profitability for a project used primarily in capital…

Q: Explain how the cost of capital serves as a screening tool when using (a) the net present value…

A: Cost of capital: Cost of capital is the required return necessary to make a capital budgeting…

Q: Define risk-adjusted cost of capital (r)

A: Risk adjusted cost of capital is the measure of returns of a project relative to the risks of a…

Q: Explain what net operating working capital is, and explain how changes in that quantity can affect…

A: Net operating working capital is defined as excess of current operating assets over current…

Q: Why is it important to match your funding with economic life of corresponding asset?

A: The use of assets economic life matching with funding can be an integral tool for financial…

Q: What distinguishes a capital investment from other investments?

A: Investments: It is the method by which an investor increases his value over some time for future…

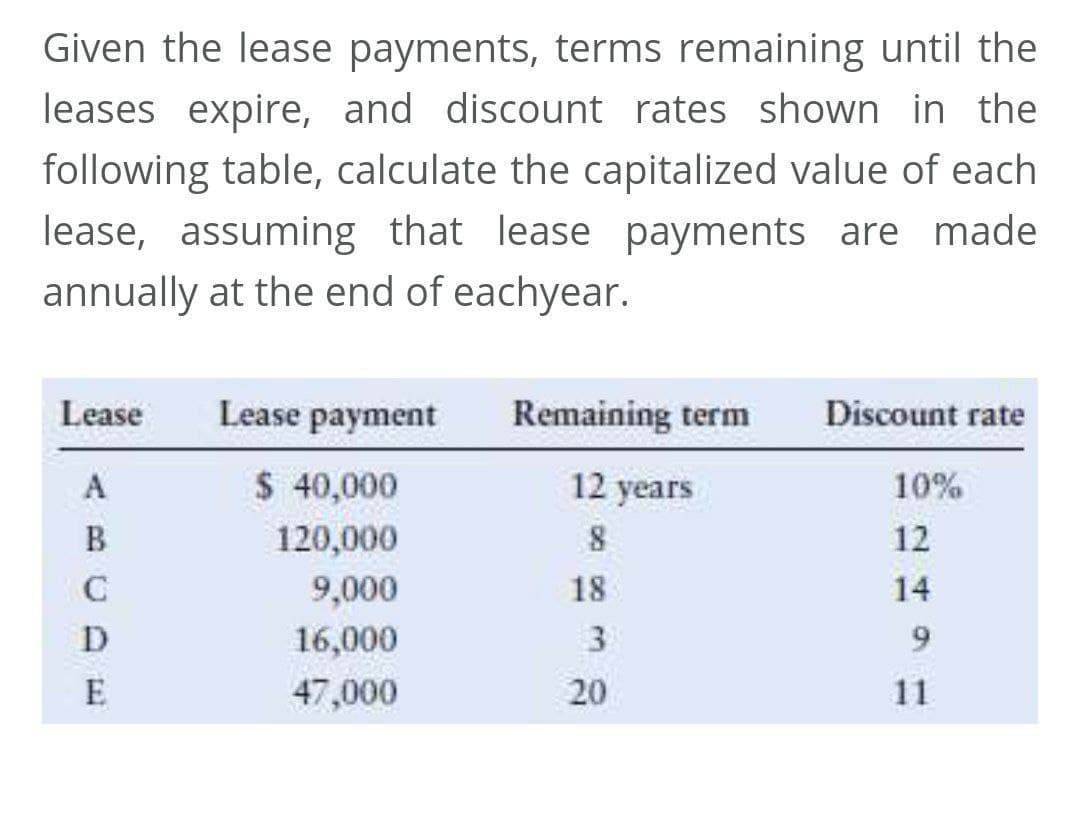

Q: Define the term capitalized cost?

A: A Capitalized Cost is the cost incurred in the purchase and financing of fixed assets. It includes…

Q: Write the capitalized-cost equation?

A: Answer: Capitalized cost is well-defined as the present value of an annual cost constant over an…

Q: Find 'return on invested capital'.

A: Ratio analysis is a method of analyzing a company's liquidity, profitability, and operational…

Q: Explain how the cost of capital serves as a screening tool when using the net present value method.

A: Definition: Net present value method: The net present value method is the method that is used to…

Q: . How are the component costs combined to forma weighted average cost of capital (WACC),and why is…

A: It is the discounted rate that has been calculated by the company on the basis of which present…

Q: Discuss the advantages and disadvantages of using (a) payback, (b) net present value and (c )…

A: Payback Period: It refers to the period in which the project's or investment's initial cost is…

Q: Explain what is capital or capital financing? Examples

A: capital financing is the form of business finance that is raised through equity funds and lenders…

Q: What is a capitalization rate? What are the different ways of arriving at this rate for an…

A: Capitalization rate: Capitalization rate is the projected rate of return percentage that a property…

Q: The net present value of an investment represents the difference between the:

A: The Answer :

Q: Explain the process of Return on Invested Capital?

A: It represents the amount of return earned by all the investors. It can be calculated by dividing…

Q: Define capital intensity ratio

A: Formula to compute capital intensity ratio:

Q: Define the term Paid-in capital?

A: Stockholders’ equity: Stockholders’ equity is referred to as the claims of the stockholders on the…

Q: Derivation of capital asset pricing model

A: The Capital Asset Pricing Model (CAPM) relates the returns on individual assets or entire portfolios…

Q: Capital Asset Pricing Model

A: The Capital Asset Pricing Model Is also known as CAPM. CAPM shows the relationship between…

Q: Relate the idea of cost of capital to the opportunity cost concept. Is the cost of capital the…

A: The total cost of financing current projects (or projects under consideration) will be the financial…

Q: Explain Initial Capital Contributions with example?

A: Initial contributions are generally made by members to take part in the company's interests. Many…

Q: What is the return on invested capital (RIC)?

A: Return on investment (ROI): This financial ratio evaluates how efficiently the assets are used in…

Q: Explain the blended capitalization rate and where it can be applied?

A: The rate which is a combination of the previous rate and the new rate charged on a loan is called a…

Q: How to make capital investment choices based on the internal rate of return (IRR)

A: Capital investment choices based on the internal rate of return (IRR) will be explained:

Q: asset

A: The term CAPM or capitam asset pricing model is a model which shows the relationship between risk…

Q: The estimated capitalized cost is $

A: A stream of equal cash flows paid or received periodically is termed as annuity. Annuity is either…

Q: What is an example or scenarios of Capital Allocation Line (CAL)?

A:

Q: Define paid-in capital

A: Definition: Stockholders’ equity: Stockholders’ equity is referred to as the claims of the…

Q: how was capital asset pricing model (CAPM) created? GIVE reference

A: Meaning CAPM Capital asset pricing model, It is created to explain the investor that he/she will get…

Q: Explain the concept of capital budgeting

A: Capital budgeting is additionally called investment appraisal utilized in evaluating major…

Q: Capital; capital structure; optimal capital structure

A: Capital: Ownership of assets of financial nature is termed as capital. Capital can be used for…

Q: What is the Return on Invested Capital?

A: Return on invested capital is calculated or determined to know the efficiency of the company on…

Q: purpose for capital analysis

A: Capital analysis is the study of capital structure of a business entity.

Q: How capital expenditure(investment) analysis helps in evaluating the inflows and outflows of cash?

A: Capital expenditure is a sort of investment in the business either by making a new product line or…

Q: How is the CAPM (Capital Asset Pricing Model) related to valuation?

A: The relationship between systematic risk and expected return on assets, particularly equities, is…

Q: What is a target capital structure?

A: Capital structure is the combination of debt and equity used by the company to finance its business.

Q: Define the term, the return on invested capital (RIC)?

A: All investments are made keeping focus on the expected returns that can be generated from it. The…

Q: Explain the term Return on Invested Capital?

A: The formula used to compute return on invested capital:

Q: Describe the concept of rate of return based on the return on invested capital in terms of a…

A: The term ROIC is used to calculate the profitability or return on invested capital that a business…

Q: Briefly discuss capital asset price model from the standpoint of investors and managers.

A: CAPM from standpoint of managers : Capital asset pricing model is of high value for financial…

Q: Which of the following is a present value method of analyzing capital investment proposals? Uaverage…

A: Cost Accounting: It is the process of collecting, recording, analyzing the cost, summarizing cost,…

Step by step

Solved in 3 steps with 2 images

- Use the information in RE20-3. Prepare the journal entries that Richie Company (the lessor) would make in the first year of the lease assuming the lease is classified as a sales-type lease. Assume that the lessee is required to make payments on December 31 each year. Also assume that Richie had purchased the equipment at a cost of 200,000.Lessee Accounting Issues Timmer Company signs a lease agreement dated January 1, 2019, that provides for it to lease equipment from Landau Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: The lease is noncancelable and has a term of 5 years. The annual rentals are 83,222.92, payable at the end of each year, and provide Landau with a 12% annual rate of return on its net investment. Timmer agrees to pay all executory costs directly to a third party on December 1 of each year. In 2019, these were insurance, 3,760; property taxes, 5,440. In 2020: insurance, 3,100; property taxes, 5,330. There is no renewal or bargain purchase option. Timmer estimates that the equipment has a fair value of 300,000, an economic life of 5 years, and a zero residual value. Timmers incremental borrowing rate is 16%, it knows the rate implicit in the lease, and it uses the straightline method to record depreciation on similar equipment. Required: 1. Calculate the amount of the asset and liability of Timmer at the inception of the lease. (Round to the nearest dollar.) 2. Prepare a table summarizing the lease payments and interest expense. 3. Prepare journal entries on the books of Timmer for 2019 and 2020. 4. Next Level Prepare a partial balance sheet in regard to the lease for Timmer for December 31, 2019. Use the present value of next years payment approach to classify the finance lease obligation between current and noncurrent. 5. Next Level Prepare a partial balance sheet in regard to the lease for Timmer for December 31, 2019. Use the change in present value approach to classify the finance lease obligation between current and noncurrent.Lessor Accounting with Guaranteed Residual Value Use the information for Edom Company in E20-8, except that the residual value was guaranteed by Davis Company (the lessee). Required: 1. Assuming that the lease is a sales-type lease, calculate the selling price. 2. Prepare a table summarizing the lease receipts and interest income earned by Edom. 3. Prepare journal entries for Edom tor the years 2019 and 2020.

- Use the information in RE20-3. Prepare the journal entries that Garvey Company would make in the first year of the lease assuming the lease is classified as a finance lease. Assume that Garvey is required to make payments on December 31 each year.Determining Type of Lease and Subsequent Accounting On January 1, 2019, Ballieu Company leases specialty equipment with an economic life of 8 years to Anderson Company. The lease contains the following terms and provisions: The lease is noncancelable and has a term of 8 years. The annual rentals arc 35,000, payable at the beginning of each year. The interest rate implicit in the lease is 14%. Anderson agrees to pay all executory costs directly to a third party and is given an option to buy the equipment for 1 at the end of the lease term, December 31, 2026. The cost of the equipment to the lessee is 150,000, and the fair value is approximately 185,100. Ballieu incurs no material initial direct costs. It is probable that Ballieu will collect the lease payments. Ballieu estimates that the fair value is expected to be significantly greater than 1 at the end of the lease term. Ballieu calculates that the present value on January 1, 2019, of 8 annual payments in advance of 35,000 discounted at 14% is 185,090.68 (the 1 purchase option is ignored as immaterial). Required: 1. Next Level Identify the classification of the lease transaction from Ballices point of view. Give the reasons for your classification. 2. Prepare all the journal entries tor Ballieu for the years 2019 and 2020. 3. Discuss the disclosure requirements for the lease transaction in Ballices notes to the financial statements.Lessor Accounting Issues Ramsey Company leases heavy equipment to Terrell Inc. on March 1, 2019, on the following terms: 1. Twenty-four lease rentals of 2,950 at the beginning of each month are to be paid by Terrell, and the lease is noncancelable. 2. The cost of the heavy equipment to Ramsey was 55,000. 3. Ramsey uses an implicit interest rate of 18% per year and will account for this lease as a sales-type lease. Required: Prepare journal entries for Ramsey (the lessor) to record the lease contract on March 1, 2019, the receipt of the first two lease rentals, and any interest income for March and April 2019. (Round your answers to the nearest dollar.)

- Sales-Type Lease with Unguaranteed Residual Value Lessor Company and Lessee Company enter into a 5-year, noncancelable, sales-type lease on January 1, 2019, for equipment that cost Lessor 375,000 (useful life is 5 years). The fair value of the equipment is 400,000. Lessor expects a 12% return on the cost of the asset over the 5-year period of the lease. The equipment will have an estimated unguaranteed residual value of 20,000 at the end of the fifth year of the lease. The lease provisions require 5 equal annual amounts, payable each January 1, beginning with January 1, 2019. Lessee pays all executory costs directly to a third party. The equipment reverts to the lessor at the termination of the lease. Assume there are no initial direct costs, and the lessor expects to be able to collect all lease payments. Required: 1. Show how Lessor should compute the annual rental amounts. 2. Prepare a table summarizing the lease and interest receipts that would be suitable for Lessor. 3. Prepare a table showing the accretion of the unguaranteed residual asset. 4. Prepare the journal entries for Lessor for the years 2019, 2020, and 2021.Sales-Type Lease with Guaranteed Residual Value Calder Company, the lessor, enters into a lease with Darwin Company, the lessee, to provide heavy equipment beginning January 1, 2017. The lease is appropriately classified as a sales-type lease. The lease terms, provisions, and related events are as follows: The lease is noncancelable, has a term of 8 years, and has no renewal or bargain purchase option. The annual rentals are 65,000, payable at the end of each year. The interest rate implicit in the lease is 15%. Darwin agrees to pay all executory costs directly to a third party. The cost of the equipment is 280,000. The fair value of the equipment to Calder is 308,021.03. Calder incurs no material initial direct costs. Calder expects that it will be able to collect all lease payments. Calder estimates that the fair value at the end of the lease term will be 50,000 and that the economic life the equipment is 9 years. This residual value is guaranteed by Darwin. The following present value factors are relevant: PV of an ordinary annuity n = 8, i = 15% = 4.487322 PV n = 8, i = 15% = 0.326902 PV n = 1, i = 15% = 0.869565 Required: 1. Determine the proper classification of the lease. 2. Prepare a table summarizing the lease receipts and interest income earned by Calder for this lease. 3. Prepare journal entries for Calder for the years 2019, 2020, and 2021. 4. Next Level Prepare partial balance sheets for December 31, 2019, and December 31, 2020, showing how the accounts should be reported. Use the present value of next years payment approach to classify the lease receivable as current and noncurrent. 5. Next Level Prepare partial balance sheets for December 31, 2019, and December 31, 2020, showing how the accounts should be reported. Use the change in present value approach to classify the lease receivable as current and noncurrent.Owens Company leased equipment for 4 years at 50,000 a year with an option to renew the lease for 6 years at 2,000 per month or to purchase the equipment for 25,000 (a price considerably less than the expected fair value) after the initial lease term of 4 years. Why would this lease qualify as a finance lease?

- Lessee Accounting Issues Sax Company signs a lease agreement dated January 1, 2019, that provides for it to lease computers from Appleton Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 5 years. The lease is noncancelable and requires equal rental payments to be made at the end of each year. The computers are not specialized for Sax. 2. The computers have an estimated life of 5 years, a fair value of 300,000, and a zero estimated residual value. 3. Sax agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. The annual payment is set by Appleton at 83,222.92 to earn a rate of return of 12% on its net investment. Sax is aware of this rate. Saxs incremental borrowing rate is 10%. 6. Sax uses the straight-line method to record depreciation on similar equipment. Required: 1. Next Level Examine and evaluate each capitalization criteria and determine what type of lease this is for Sax. 2. Calculate the amount of the asset and liability of Sax at the inception of the lease (round to the nearest dollar). 3. Prepare a table summarizing the lease payments and interest expense. 4. Prepare journal entries for Sax for the years 2019 and 2020.Lessee Accounting with Payments Made at Beginning of Year Adden Company signs a lease agreement dated January 1, 2019, that provides for it to lease non-specialized heavy equipment from Scott Rental Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 4 years. The lease is noncancelable and requires annual rental payments of 20,000 to be paid in advance at the beginning of each year. 2. The cost, and also fair value, of the heavy equipment to Scott at the inception of the lease is 68,036.62. The equipment has an estimated life of 4 years and has a zero estimated residual value at the end of this time. 3. Adden agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. Scotts interest rate implicit in the lease is 12%. Adden is aware of this rate, which is equal to its borrowing rate. 6. Adden uses the straight-line method to record depreciation on similar equipment. 7. Executory costs paid at the end of the year by Adden are: Required: 1. Next Level Determine what type of lease this is for Adden. 2. Prepare a table summarizing the lease payments and interest expense for Adden. 3. Prepare journal entries for Adden for the years 2019 and 2020.Lessee and Lessor Accounting Issues The following information is available for a noncancelable lease of equipment entered into on March 1, 2019. The lease is classified as a sales-type lease by the lessor (Anson Company) and as a finance lease by the lessee (Bullard Company). Assume that the lease payments are nude at the beginning of each month, interest and straight-line depreciation are recognized at the end of each month, and the residual value of the leased asset is zero at the end of a 3-year life. Required: 1. Record the lease (including the initial receipt of 2,000) and the receipt of the second and third installments of 2,000 in Ansons accounts. Carry computations to the nearest dollar. 2. Record the lease (including the initial payment of 2,000), the payment of the second and third installments of 2,000, and monthly depreciation in Bullards accounts. The lessee records the lease obligation at net present value. Carry computations to the nearest dollar.