Candlex Ltd Co is appraising an investment project which has an expected life of four years and which will not be repeated. The initial investment, payable at the start of the first year of operation, is K5 million. Scrap value of K500, 000 is expected to arise at the end of four years. There is some uncertainty about what price can be charged for the units produced by the investment project, as this is expected to depend on the future state of the economy. The following forecast of selling prices and their probabilities has been prepared: Future economic state Weak Medium Strong Probability of future economic state 35% 50% 15% Selling price in current price terms K25 per unit K30 per unit K35 per unit These selling prices are expected to be subject to annual inflation of 4% per year, regardless of which economic state prevails in the future. Forecast sales and production volumes, and total nominal variable costs, have already been forecast, as follows: Year 1 2 3 4 Sales and production (units) 150,000 250,000 400,000 300,000 Nominal variable cost (K000) 2,385 4,200 7,080 5,730 Incremental overheads of K400, 000 per year in current price terms will arise as a result of undertaking the investment project. A large proportion of these overheads relate to energy costs which are expected to increase sharply in the future because of energy supply shortages, so overhead inflation of 10% per year is expected. The initial investment will attract tax-allowable depreciation on a straight-line basis over the four-year project life. The rate of corporation tax is 30% and tax liabilities are paid in the year in which they arise. The company has traditionally used a nominal after-tax discount rate of 11% per year for investment appraisal. Required: Evaluate the use of the four investment appraisal methods in deciding which projects to undertake by government and private companies.

Candlex Ltd Co is appraising an investment project which has an expected life of four years and which will not be repeated. The initial investment, payable at the start of the first year of operation, is K5 million. Scrap value of K500, 000 is expected to arise at the end of four years. There is some uncertainty about what price can be charged for the units produced by the investment project, as this is expected to depend on the future state of the economy. The following forecast of selling prices and their probabilities has been prepared: Future economic state Weak Medium Strong Probability of future economic state 35% 50% 15% Selling price in current price terms K25 per unit K30 per unit K35 per unit These selling prices are expected to be subject to annual inflation of 4% per year, regardless of which economic state prevails in the future. Forecast sales and production volumes, and total nominal variable costs, have already been forecast, as follows: Year 1 2 3 4 Sales and production (units) 150,000 250,000 400,000 300,000 Nominal variable cost (K000) 2,385 4,200 7,080 5,730 Incremental overheads of K400, 000 per year in current price terms will arise as a result of undertaking the investment project. A large proportion of these overheads relate to energy costs which are expected to increase sharply in the future because of energy supply shortages, so overhead inflation of 10% per year is expected. The initial investment will attract tax-allowable depreciation on a straight-line basis over the four-year project life. The rate of corporation tax is 30% and tax liabilities are paid in the year in which they arise. The company has traditionally used a nominal after-tax discount rate of 11% per year for investment appraisal. Required: Evaluate the use of the four investment appraisal methods in deciding which projects to undertake by government and private companies.

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter19: Capital Investment

Section: Chapter Questions

Problem 2CE

Related questions

Question

Candlex Ltd Co is appraising an investment project which has an expected life of four years and which will not be repeated. The initial investment, payable at the start of the first year of operation, is K5 million. Scrap value of K500, 000 is expected to arise at the end of four years.

There is some uncertainty about what price can be charged for the units produced by the investment project, as this is expected to depend on the future state of the economy. The following forecast of selling prices and their probabilities has been prepared:

Future economic state Weak Medium Strong

Probability of future economic state 35% 50% 15%

Selling price in current price terms K25 per unit K30 per unit K35 per unit

These selling prices are expected to be subject to annual inflation of 4% per year, regardless of which economic state prevails in the future.

Forecast sales and production volumes, and total nominal variable costs, have already been forecast, as follows:

Year 1 2 3 4

Sales and production (units) 150,000 250,000 400,000 300,000

Nominal variable cost (K000) 2,385 4,200 7,080 5,730

Incremental overheads of K400, 000 per year in current price terms will arise as a result of undertaking the investment project. A large proportion of these overheads relate to energy costs which are expected to increase sharply in the future because of energy supply shortages, so overhead inflation of 10% per year is expected.

The initial investment will attract tax-allowable depreciation on a straight-line basis over the four-year project life. The rate of corporation tax is 30% and tax liabilities are paid in the year in which they arise. The company has traditionally used a nominal after-tax discount rate of 11% per year for investment appraisal.

Required:

Evaluate the use of the four investment appraisal methods in deciding which projects to undertake by government and private companies.

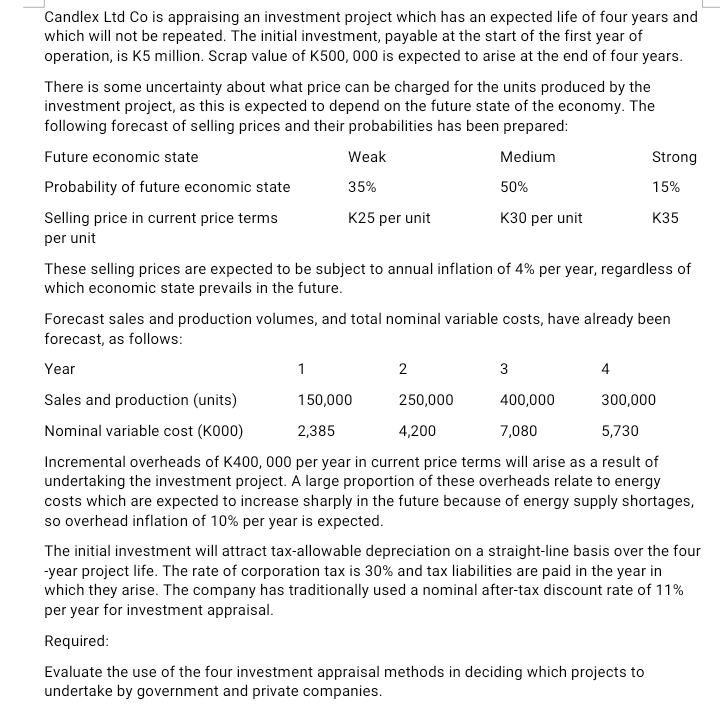

Transcribed Image Text:Candlex Ltd Co is appraising an investment project which has an expected life of four years and

which will not be repeated. The initial investment, payable at the start of the first year of

operation, is K5 million. Scrap value of K500, 000 is expected to arise at the end of four years.

There is some uncertainty about what price can be charged for the units produced by the

investment project, as this is expected to depend on the future state of the economy. The

following forecast of selling prices and their probabilities has been prepared:

Future economic state

Weak

Medium

Strong

Probability of future economic state

35%

50%

15%

K25 per unit

Selling price in current price terms

per unit

кзо реr unit

K35

These selling prices are expected to be subject to annual inflation of 4% per year, regardless of

which economic state prevails in the future.

Forecast sales and production volumes, and total nominal variable costs, have already been

forecast, as follows:

Year

1

3

4

Sales and production (units)

150,000

250,000

400,000

300,000

Nominal variable cost (K000)

2,385

4,200

7,080

5,730

Incremental overheads of K400, 000 per year in current price terms will arise as a result of

undertaking the investment project. A large proportion of these overheads relate to energy

costs which are expected to increase sharply in the future because of energy supply shortages,

so overhead inflation of 10% per year is expected.

The initial investment will attract tax-allowable depreciation on a straight-line basis over the four

-year project life. The rate of corporation tax is 30% and tax liabilities are paid in the year in

which they arise. The company has traditionally used a nominal after-tax discount rate of 11%

per year for investment appraisal.

Required:

Evaluate the use of the four investment appraisal methods in deciding which projects to

undertake by government and private companies.

Expert Solution

Step by step

Solved in 9 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning