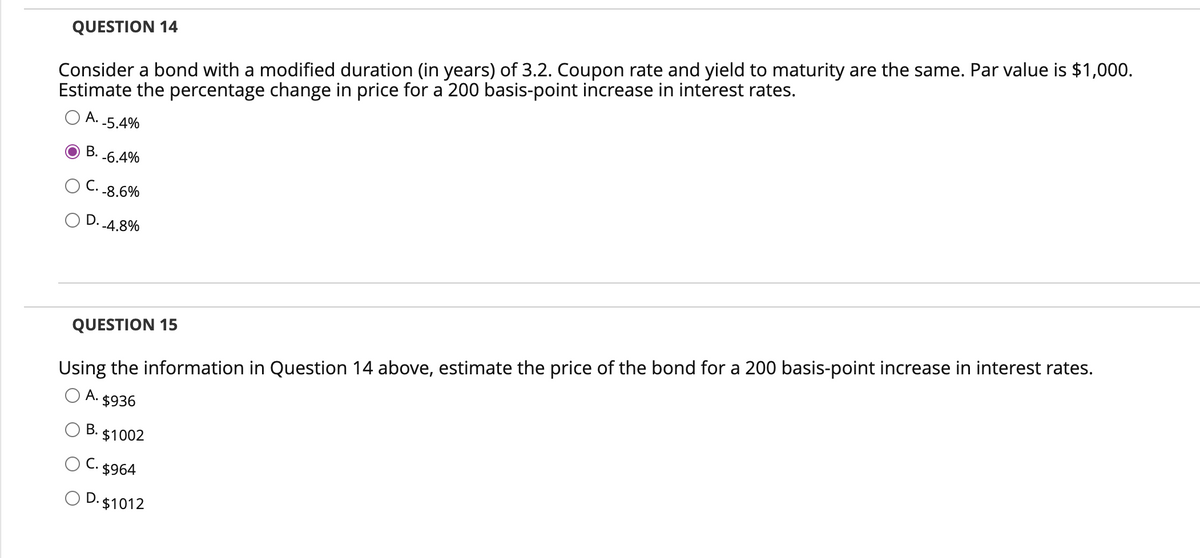

Consider a bond with a modified duration (in years) of 3.2. Coupon rate and yield to maturity are the same. Par value is $1,000. Estimate the percentage change in price for a 200 basis-point increase in interest rates.

Consider a bond with a modified duration (in years) of 3.2. Coupon rate and yield to maturity are the same. Par value is $1,000. Estimate the percentage change in price for a 200 basis-point increase in interest rates.

Chapter14: Investing In Stocks And Bonds

Section: Chapter Questions

Problem 6DTM

Related questions

Question

The second question. Thank you.

Transcribed Image Text:Consider a bond with a modified duration (in years) of 3.2. Coupon rate and yield to maturity are the same. Par value is $1,000.

Estimate the percentage change in price for a 200 basis-point increase in interest rates.

A. -5.4%

B. -6.4%

C.

QUESTION 14

-8.6%

OD. -4.8%

QUESTION 15

Using the information in Question 14 above, estimate the price of the bond for a 200 basis-point increase in interest rates.

O A. $936

B.

³. $1002

C. $964

O D. $1012

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781337395250

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning