Determine the following as a result of your audit: 16. How much is the cost of Land disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 17. How much is the cost of Land Improvements disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 18. How much is the cost of Building disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 19. How much is the cost of Machineries disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 20. How much is the amount of Depreciation expense reported by Fix You Company in its statement of comprehensive income for the period ending December 31, 2022?

Determine the following as a result of your audit: 16. How much is the cost of Land disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 17. How much is the cost of Land Improvements disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 18. How much is the cost of Building disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 19. How much is the cost of Machineries disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 20. How much is the amount of Depreciation expense reported by Fix You Company in its statement of comprehensive income for the period ending December 31, 2022?

Determine the following as a result of your audit: 16. How much is the cost of Land disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 17. How much is the cost of Land Improvements disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 18. How much is the cost of Building disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 19. How much is the cost of Machineries disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 20. How much is the amount of Depreciation expense reported by Fix You Company in its statement of comprehensive income for the period ending December 31, 2022?

Determine the following as a result of your audit: 16. How much is the cost of Land disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 17. How much is the cost of Land Improvements disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 18. How much is the cost of Building disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 19. How much is the cost of Machineries disclosed in its notes to financial statement as component of property, plant and equipment – net as of December 31, 2022? 20. How much is the amount of Depreciation expense reported by Fix You Company in its statement of comprehensive income for the period ending December 31, 2022?

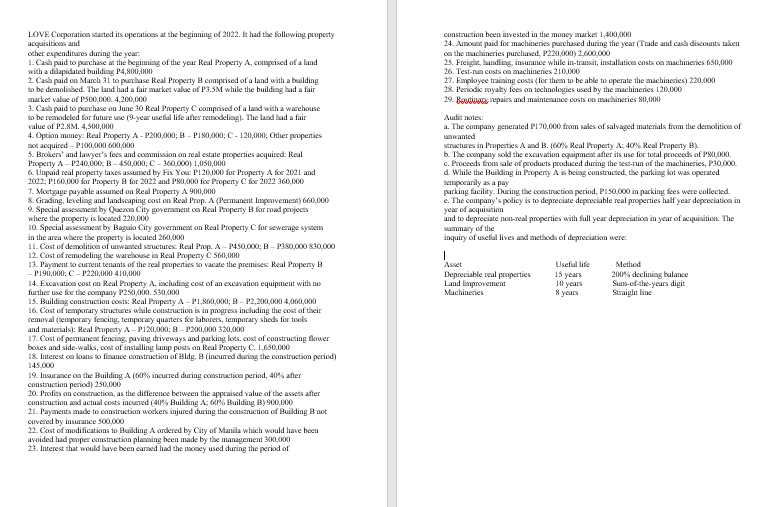

Transcribed Image Text:LOVE Corporation started its operations at the beginning of 2022. It had the following property

acquisitions and

other expenditures during the year:

1. Cash paid to purchase at the beginning of the year Real Property A, comprised of a land

with a dilapidated building P4,800,000

2. Cash paid on March 31 to purchase Real Property B comprised of a land with a building

to be demolished. The land had a fair market value of P3.5M while the building had a fair

market value of P500,000. 4,200,000

3. Cash paid to purchase on June 30 Real Property C comprised of a land with a warehouse

to be remodeled for future use (9-year useful life after remodeling). The land had a fair

value of P2.8M. 4,500,000

4. Option money: Real Property A-P200,000; B - P180,000; C-120,000; Other properties

not acquired-P100,000 600,000

5. Brokers and lawyer's fees and commission on real estate properties acquired: Real

Property A-P240,000; B-450,000; C-360,000) 1,050,000

6. Unpaid real property taxes assumed by Fix You: P120,000 for Property A for 2021 and

2022; P160,000 for Property B for 2022 and P80,000 for Property C for 2022 360,000

7. Mortgage payable assumed on Real Property A 900,000

& Grading, leveling and landscaping cost on Real Prop. A (Permanent Improvement) 660,000

9. Special assessment by Quezon City government on Real Property B for road projects

where the property is located 220,000

10. Special assessment by Baguio City government on Real Property C for sewerage system

in the area where the property is located 260,000

11. Cast of demolition of unwanted structures: Real Prop. A-P450,000; B-P380,000 830,000

12. Cost of remodeling the warehouse in Real Property C 560,000

13. Payment to current tenants of the real properties to vacate the premises: Real Property B

- P190,000; C-P220,000 410,000

14. Excavation cost on Real Property A, including cost of an excavation equipment with no

further use for the company P250,000. 530,000

15. Building construction costs: Real Property A-P1,860,000; B-P2,200,000 4,060,000

16. Cost of temporary structures while construction is in progress including the cost of their

removal (temporary fencing, temporary quarters for laborers, temporary sheds for tools

and materials): Real Property A-P120,000; B-P200,000 320,000

17. Cost of permanent fencing, paving driveways and parking lots, cost of constructing flower

boxes and side-walks, cost of installing lamp posts on Real Property C. 1,650,000

18. Interest on loans to finance construction of Bldg. B (incurred during the construction period)

145,000

19. Insurance on the Building A (60% incurred during construction period, 40% after

construction period) 250,000

20. Profits on construction, as the difference between the appraised value of the assets after

construction and actual costs incurred (40% Building A; 60% Building B) 900,000

21. Payments made to construction workers injured during the construction of Building B not

covered by insurance 500,000

22. Cost of modifications to Building A ordered by City of Manila which would have been

avoided had proper construction planning been made by the management 300,000

23. Interest that would have been earned had the money used during the period of

construction been invested in the money market 1,400,000

24. Amount paid for machineries purchased during the year (Trade and cash discounts taken

on the machineries purchased, P220,000) 2,600,000

25. Freight, handling, insurance while in-transit, installation costs on machineries 650,000

26. Test-run costs on machineries 210,000

27. Employee training costs (for them to be able to operate the machineries) 220,000

28. Periodic royalty fees on technologies used by the machineries 120,000

29. Bouti, repairs and maintenance costs on machineries 80,000

Audit notes:

a. The company generated P170,000 from sales of salvaged materials from the demolition of

unwanted

structures in Properties A and B. (60% Real Property A: 40% Real Property B).

b. The company sold the excavation equipment after its use for total proceeds of P80,000.

c. Proceeds from sale of products produced during the test-run of the machineries, P30,000.

d. While the Building in Property A is being constructed, the parking lot was operated

temporarily as a pay

parking facility. During the construction period, P150,000 in parking fees were collected.

e. The company's policy is to depreciate depreciable real properties half year depreciation in

year of acquisition

and to depreciate non-real properties with full year depreciation in year of acquisition. The

summary of the

inquiry of useful lives and methods of depreciation were:

|

Asset

Depreciable real properties

Land Improvement

Machineries

Useful life

15 years

10 years

8 years

Method

200% declining balance

Sum-of-the-years digit

Straight line

Definition Video Definition Accounting method wherein the cost of a tangible asset is spread over the asset's useful life. Depreciation usually denotes how much of the asset's value has been used up and is usually considered an operating expense. Depreciation occurs through normal wear and tear, obsolescence, accidents, etc. Video

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.