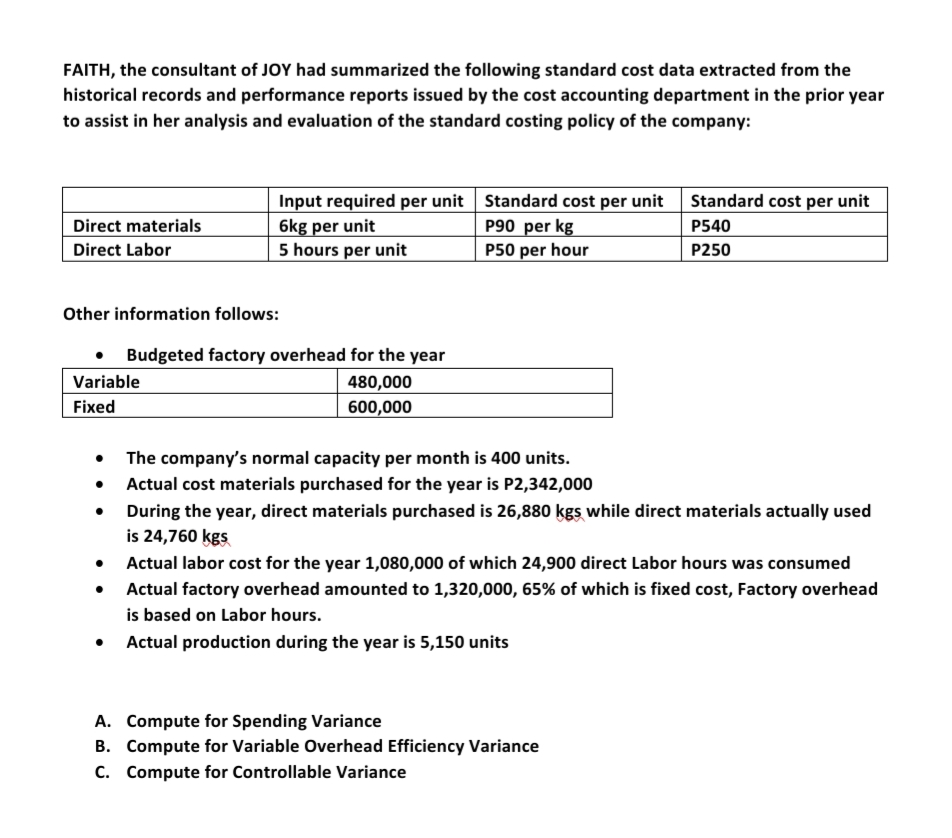

FAITH, the consultant of JOY had summarized the following standard cost data extracted from the historical records and performance reports issued by the cost accounting department in the prior year to assist in her analysis and evaluation of the standard costing policy of the company: Input required per unit Standard cost per unit Standard cost per unit 6kg per unit 5 hours per unit Direct materials P90 per kg P540 Direct Labor P50 per hour P250 Other information follows: Budgeted factory overhead for the year Variable 480,000 600,000 Fixed The company's normal capacity per month is 400 units. • Actual cost materials purchased for the year is P2,342,000 • During the year, direct materials purchased is 26,880 kgs while direct materials actually used is 24,760 kgs • Actual labor cost for the year 1,080,000 of which 24,900 direct Labor hours was consumed Actual factory overhead amounted to 1,320,000, 65% of which is fixed cost, Factory overhead is based on Labor hours. Actual production during the year is 5,150 units A. Compute for Spending Variance B. Compute for Variable Overhead Efficiency Variance C. Compute for Controllable Variance

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

Trending now

This is a popular solution!

Step by step

Solved in 3 steps