How much is the Non-controlling interest on January 1, 2x19?

Q: Based on the preceding information, what is the amount of comprehensive attributable to the…

A: Controlling interest represents the ownership stake in an organization obtains by investing in…

Q: Company A acquired a 70% holding in Company B on 1 January 20X4 for $600,000. At that date the fair…

A: We have the following information: Company A acquired a 70% holding in Company B on 1 January 20X4…

Q: Company P purchases a 100%o interest in Company S for $800,000. If Company

A: APIC is Additional Paid In Capital is the amount paid by the…

Q: a) Determine Mr Penny's stocks owned for purposes of the Internal Revenue Code Section 302(b)(2))…

A: Redemption: Redemption can be defined as the repayment made in respect of any money market security…

Q: Assume that the cost of acquisition includes a control premium of P30,000, the non-controlling…

A: Retained earnings refer to the earnings earned by the parent company and the part of the earnings of…

Q: dentify w

A: Shareholders also invest money in the company and in return they become the owners in proportion to…

Q: How come that it became P27,000? Isn't that is the non-controlling interest in net assets (90,000 x…

A: Non Controlling Interest Calculation of non controlling interest is important in part in the workout…

Q: Illustration 2. Non-Controlling Interest On January 1, 2021, Inahan Co. acquired 75% of the voting…

A: 1. Previously held equity untereat in the aquiree is a 0.00 since Inhaan Co. acquired 75% share on…

Q: You are required to prepare the consolidated statement of financial position as at 31 December x7.…

A: Generally the value of the selling company shall be calculated in different methods like Net asset…

Q: 1. How much will be the Non-controlling interest net income for 2020? 2. How much will be the…

A: Consolidated Statement: It is statement which present all income, expenses, assets and liability of…

Q: share dividend on its share capital

A: Upon issue of share dividend, retained earnings is debited with issue price, common stock is…

Q: An entity acquired a 30% interest in another entity in Year I. In Year 2, it acquired another 50%…

A: Business Combination: In a business combination, the acquirer gets ownership of another company via…

Q: In elemination entries, in the credit investment in subsidiaries and non-controlling interest were…

A: Total credit entry = Investment in subsidiaries + Non-controlling interest

Q: Apple Corporation issued its 3,000 ordinary share in exchange for land which has a fair market value…

A: Share premium = Fair market value of Land - Par value of ordinary share where, Par value of ordinary…

Q: 18. An entity, with an investment in debt securities carried as FVOCI, deemed its original business…

A: If the entity business model changed then the entity needs to reclassify its financial instrument. A…

Q: Solely Stock. S transferred appreciated property to a newly created corporation for 60% of its stock…

A: When the capital asset is sold above than its carrying value, the gain incurred on such transaction…

Q: 7. What amount of non-controlling interest is to be presented in the consolidated statement of…

A: Retained Earnings:- Retained earnings are considered as the part of profit, that is not distributed…

Q: If the purchase price is 500000 OMR under IFRS, the market value of the net assets is 450000 OMR and…

A: NCI is the residual interest in the subsidiary entity other than the parent interest. NCI at…

Q: An entity acquired a 30% interest in another entity in Year I. In Year 2, it acquired another 50%…

A: As per IFRS 3 Business combination, If after acquisition of a portion of stake without obtaining…

Q: What is the total non-controlling interest in net income of subsidiary (NCINI5) on Dec 31, 20x5?

A: As per our protocol, we provide the solution to the one question only but as you have asked two…

Q: The Non-controlling interest in Net Income for 20x1:

A: Solution: Non-controlling Interest-: A Non-controlling Interest, which is also understood as a…

Q: The par value of a share capital is * O The legal nominal value assigned to the share O The amount…

A: Share means a ita an financial instrument that a Company used for their Fund arrangements from the…

Q: How much is the shareholder's equity at 12/31/2019?

A: Shareholders Equity The preparation of shareholders equity which know the details of total equity…

Q: What amount should be recognized as gain on reversal of share appreciation rights in 2021? *see…

A: Compensation Expense- Compensation Expense means all expenses and costs related with compensation…

Q: When does a dividend become a liability

A: Dividend: dividend is the portions of profit given to the shareholders by the company Major days in…

Q: n from the separ ome of P Compa as follows: ial position acco ..... ...

A: Given The percent of non-controlling interest ownership in S Company as of December 31, 2019.

Q: Question: What is the implied goodwill on January 1, 2020? On January 1, 2019, an entity purchased…

A: Implies goodwill is kind of deemed goodwill which is included in the cost of investment made by the…

Q: The fair value of Winds' assets is P50,000 more than the aggregate carrying amounts. Non-controlling…

A: Consolidated Total Equity is the value of Equity of the company after consolidation of Two or more…

Q: Determine if this shall result in recognition of liabilities 8.Declaration of property dividends on…

A: The dividend is declared to the shareholders from the retained earnings of the business.

Q: What is the adjusted amount of shareholders’ equity that should be reported by REBOND in its…

A: The question is related Shareholder's equity as on December 31st, 2021. Inventory will be Valued at…

Q: how much is the non-controlling interest on december 31, 20x2 if entity A acquired 90% interest in…

A: Acquired 90% interest in entity B on Jan 1.

Q: Does X, Inc control Z, Inc as a result of this agreement?

A: Introduction: Business combination: Business combination can be defined as transaction through…

Q: Which of the following nominal rates does not apply to a C corporation? a. 10% b. 15% c. 25% d. 35%

A: C Corporation: C Corporation refers to the legal structure where the owners or the shareholders are…

Q: .How much is the transaction costs incurred during the business combination?

A: The answers for the multiple choice questions and relevant working are presented hereunder :…

Q: Statement of Financial Position as on 31st Dec 2019 Super Star LLC LLC Assets Non-Current Assets…

A: A consolidated balance sheet is a key financial statement in the case of group companies. The…

Q: Which of the following circumstance lead to delisting of a company from the M 1. Liquidation of the…

A: Delisting is defined as removal of the listed security from the stock exchange and it could be done…

Q: Smart owns 80% of Simple. Where is the 20% noncontrolling interest in Simple reported on the balance…

A: Introduction: Balance sheet: All Assets and liabilities are shown in Balance sheet. It tells the net…

Q: An entity acquired a 30% interest in another entity in Year I. In Year 2, it acquired another 50%…

A: As per IFRS/PFRS 3 Business combination, and IFRS 10 Consolidation After acquiring controlling…

Q: b) Demonstrate that in principle the shareholders will be equally well off by subscribing to the…

A: The answer is stated below:

Q: - 9, 2022, PC Inc. rec $0.30 per share on i in A&A Company. 5, 2022, PC Inc. sold

A:

Q: An entity acquired a 30% interest in another entity in Year I. In Year 2, it acquired another 50%…

A: As per IFRS/PFRS3 Business combination, An entity after acquiring controlling stake, it's…

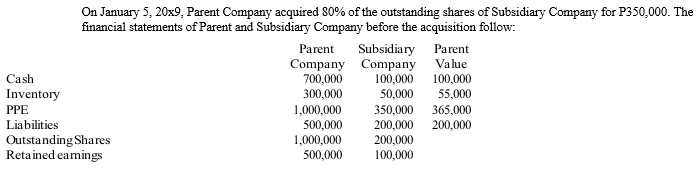

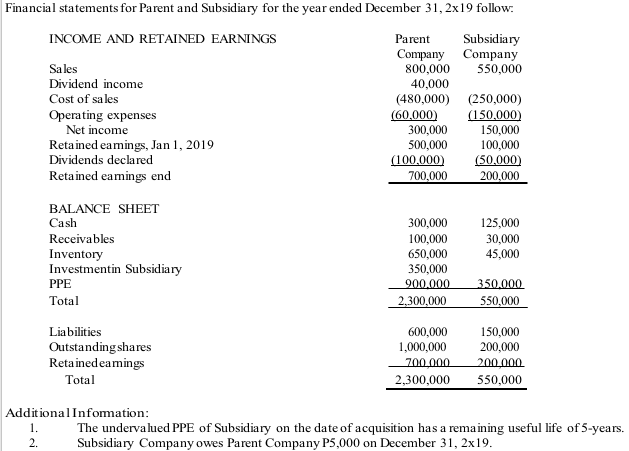

Q: How much is the non-controlling interest in profit of Subsidiary Company on December 31, 2x19?

A: Consolidated money statements area unit money statements of Associate in Nursing entity with…

Q: Accenture purchases 55% of the voting common stock of JBL. After the purchase, Accenture has a…

A: Share of purchase = 55%

Q: Equity securities acquired by a corporation which are accounted for by recognizing unrealized…

A: When some investments are made in some other company or corporation, then it depends on the quantum…

Q: The portion of proceeds from the sale of bonds with detachable stock warrants attributable to the…

A: Option (A) additional paid-in capital account is the correct answer.

How much is the Non-controlling interest on January 1, 2x19?

Step by step

Solved in 2 steps

- On January 1, 20x8, Parent Company purchased 80% of the outstanding shares of Subsidiary Company for P800,000. On the date of acquisition, Subsidiary Company reported Ordinary Shares of P800,000 and Retained Earnings of P200,000. Subsidiary’s Inventory was understated by P20,000; Equipment with a 5-year life was understated by P20,000, Building with an 8-year life was understated by P80,000 and land was understated by P40,000. The non-controlling interest is to be stated at fair value and the fair value of the non-controlling interest on January 1, 20x8 is P210,000. During the year, Parent sold goods to Subsidiary for P150,000 at a 25% mark-up and in turn purchased P200,000 of Subsidiary’s goods which Subsidiary sold at a 20% mark-up. From the goods purchased, P50,000 remain in Parent’s books at the end of the year, while P20,000 remain in Subsidiary’s books at the end of the year. 30% of the undervalued inventory of Subsidiary still remain unsold by the end of 20x8. The following are…On January 1, 20x8,Parent Company purchased 80% of the outstanding shares of Subsidiary Company for P800,000. On the date of acquisition, Subsidiary Company reported Ordinary Shares of P800,000 and Retained Earnings of P200,000. Subsidiary’s Inventory was understated by P20,000; Equipment with a 5-year life was understated by P20,000, Building with an 8-year life was understated by P80,000 and land was understated by P40,000. The non-controlling interest is to be stated at fair value and the fair value of the non-controlling interest on January 1, 20x8 is P210,000. The following are taken from the books of Parent and Subsidiary for 20x8: Determine the Non-Controlling Interest as of December 31, 20x8. Your answerOn January 1, 20x8,Parent Company purchased 80% of the outstanding shares of Subsidiary Company for P800,000. On the date of acquisition, Subsidiary Company reported Ordinary Shares of P800,000 and Retained Earnings of P200,000. Subsidiary’s Inventory was understated by P20,000; Equipment with a 5-year life was understated by P20,000, Building with an 8-year life was understated by P80,000 and land was understated by P40,000. The non-controlling interest is to be stated at fair value and the fair value of the non-controlling interest on January 1, 20x8 is P210,000. The following are taken from the books of Parent and Subsidiary for 20x8. 1. Determine the Non-Controlling Interest as of December 31, 20x8. 2.

- On January 1, 20x8,Parent Company purchased 80% of the outstanding shares of Subsidiary Company for P800,000. On the date of acquisition, Subsidiary Company reported Ordinary Shares of P800,000 and Retained Earnings of P200,000. Subsidiary’s Inventory was understated by P20,000; Equipment with a 5-year life was understated by P20,000, Building with an 8-year life was understated by P80,000 and land was understated by P40,000. The non-controlling interest is to be stated at fair value and the fair value of the non-controlling interest on January 1, 20x8 is P210,000. The following are taken from the books of Parent and Subsidiary for 20x8. 1) From the given data, determine the total assets as of December 31, 20x1. 2) From the given data, assuming the retained earning of Subsidiary on December 31, 20x11 is P350,000, determine the non-controlling interest to be reported in the consolidated financial statements on December 31, 20x11 assuming no changes to Subsidiary company’s ordinary…From the given data, determine the NON-CONTROLLING INTEREST on December 31, 20x8. On January 1, 20x8,Parent Company purchased 80% of the outstanding shares of Subsidiary Company for P800,000. On the date of acquisition, Subsidiary Company reported Ordinary Shares of P800,000 and Retained Earnings of P200,000. Subsidiary’s Inventory was understated by P20,000; Equipment with a 5-year life was understated by P20,000, Building with an 8-year life was understated by P80,000 and land was understated by P40,000. The non-controlling interest is to be stated at fair value and the fair value of the non-controlling interest on January 1, 20x8 is P210,000. During the year, Parent sold goods to Subsidiary for P150,000 at a 25% mark-up and in turn purchased P200,000 of Subsidiary’s goods which Subsidiary sold at a 20% mark-up. From the goods purchased, P50,000 remain in Parent’s books at the end of the year, while P20,000 remain in Subsidiary’s books at the end of the year. 30% of the undervalued…PARENT Corporation acquired 80% of the outstanding shares of SUBSIDIARY Company on June 1, 2022 for P3,517,500. SUBSIDIARY Company’s stockholder’s equity components at the end of this year are as follows; Ordinary shares, P100 par, P1,500,000. Share premium P675,000 and Retained Earnings P1,335,000. Non-controlling interest is measured at fair value and the fair value is P705,000. The assets of SUBSIDIARY were fairly valued, except for inventories, which are overstated by P66,000 and equipment, which was understated by P90,000. Remaining useful life of equipment is 4 years. Stockholder’s equity of PARENT on January 1, 2022 is composed of Ordinary shares P4,500,000, Share premium P1,050,000, Retained Earnings P3,150,000. Goodwill, if any, should be written down by P85,350 at year-end. Net Income for the first year of parent is P450,000 and the net income of subsidiary from the date of acquisition is P255,000. Dividends declared at the end of the year amounted to P120,000 and P90,000 for…

- On 1 January 20X9, JB Enterprises acquired 70 per cent of the shares of Good Company. The separate condensed statements of financial position of JB Enterprises and of Good Company immediately after the acquisition appeared as shown below: (all amounts in €) JB Good Company Assets Property, plant and equipment (net) 18.750.000 2.600.000 Investment in Good Company 3.600.000 - Inventories 1.000.000 740.000 Cash 13.550.000 560.000 Trade and other receivables 4.400.000 660.000 41.300.000 4.560.000 Equity and Liabilities Share capital 10.000.000 2.000.000 Reserves 16.200.000 1.600.000 Profit for the year 20X4 1.600.000 240.000 Provisions 100.000 250.000 Current liabilities 13.400.000 470.000 41.300.000 4.560.000 Additional information (at acquisition…On January 1, 2022, Pet Company purchased 80% of the shares of Sam Company for P1,000,000. The shareholders' equity of Sam Company on that date showed: Ordinary Shares - P570,000 and Retained Earnings - P490,000. Non-controlling interest is initially measured at proportionate share of subsidiary's net assets.On April 30, 2022, Pet acquired used machinery for P84,000 from Sam that was being carried in the latter's books at P105,000. The asset still has a remaining useful life of 5 years. On the other hand, on August 31, 2022, Sam purchased an equipment that was already 20% depreciated from Pet for P345,000. The original cost of this equipment was P375,000 and had a remaining life of 8 years.Net income of Pet Company and Sam Company for 2022 amounted to P360,000 and P155,000. Dividends paid totaled to P115,000 and P52,500 for Pet and Sam, respectively.Required:On the consolidated financial statements in 2022, how much would be the Net income attributable to parents' shareholders'…On January 1, 2022, Pet Company purchased 80% of the shares of Sam Company for P1,000,000. The shareholders' equity of Sam Company on that date showed: Ordinary Shares - P570,000 and Retained Earnings - P490,000. Non-controlling interest is initially measured at proportionate share of subsidiary's net assets.On April 30, 2022, Pet acquired used machinery for P84,000 from Sam that was being carried in the latter's books at P105,000. The asset still has a remaining useful life of 5 years. On the other hand, on August 31, 2022, Sam purchased an equipment that was already 20% depreciated from Pet for P345,000. The original cost of this equipment was P375,000 and had aremaining life of 8 years.Net income of Pet Company and Sam Company for 2022 amounted to P360,000 and P155,000. Dividends paid totaled to P115,000 and P52,500 for Pet and Sam, respectively.Required:On the consolidated financial statements in 2022, how much would be the carrying value of Property and Equipment?

- On January 1, 2022, Pet Company purchased 80% of the shares of Sam Company for P1,000,000. The shareholders' equity of Sam Company on that date showed: Ordinary Shares - P570,000 and Retained Earnings - P490,000. Non-controlling interest is initially measured at proportionate share of subsidiary's net assets.On April 30, 2022, Pet acquired used machinery for P84,000 from Sam that was being carried in the latter's books at P105,000. The asset still has a remaining useful life of 5 years. On the other hand, on August 31, 2022, Sam purchased an equipment that was already 20% depreciated from Pet for P345,000. The original cost of this equipment was P375,000 and had a remaining life of 8 years.Net income of Pet Company and Sam Company for 2022 amounted to P360,000 and P155,000. Dividends paid totaled to P115,000 and P52,500 for Pet and Sam, respectively.Required:On the consolidated financial statements in 2022, how much would be the Non-controlling interest in the net income of…Parent Company acquired 80% of the outstanding shares of Subsidiary Company for 4,500,000 on January 2, 2020 and paid P50,000 for direct acquisition related costs. On this date, Subsidiary Company’s stockholders’ equity was composed of: Share Capital – P2,000,000; Share Premium – P1,200,000 and Retained Earnings – P1,600,000. The excess of cost over book value was allocated as follows: 10% to undervalued inventory, 40% to over depreciated fixed assets which has a remaining life of 5 years and the remainder to goodwill. Subsidiary reported net income of P200,000 and paid dividends of P150,000 in 2020. The impairment on goodwill for 2020 was reported to be P5,000. The NCI in the consolidated balance sheet on December 31, 2020 is?Parent Corporation acquired 80% of the outstanding shares of Subsidiary Company on June 1, 2021 for P3,517,500. Subsidiary Company’s stockholder’s equity components at the end of this year are as follows: Ordinary shares, P100 par, P1,500,000, Share premium P675,000 and Retained Earnings P1,335,000. Non-controlling interest is measured at fair value and the fair value is P705,000. The assets of Subsidiary Company were fairly valued, except for inventories, which are overstated by P66,000, and equipment, which was understated by P90,000. Remaining useful life of equipment is 4 years. Stockholder’s equity of Parent Corporation on January 1, 2021 is composed of Ordinary shares P4,500,000, Share premium P1,050,000, Retained Earnings P3,150,000. Goodwill, if any, should be written down by P85,350 at year end. Net Income for the first year of parent is P450,000 and the net income of Subsidiary Company from the date of acquisition is P255,000. Dividends declared at the end of the year…