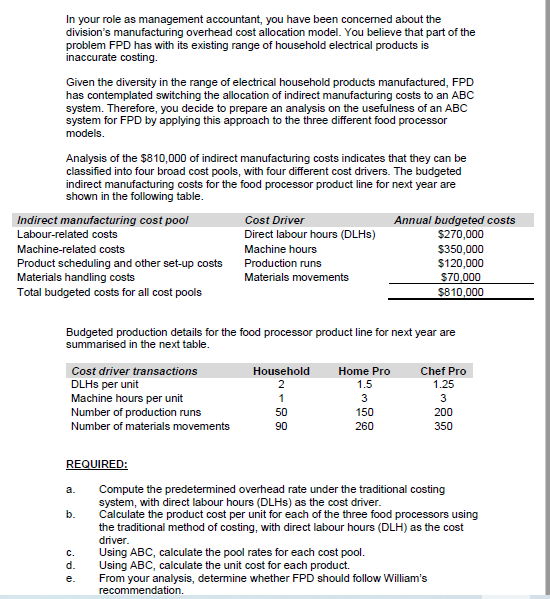

In your role as management accountant, you have been concerned about the division's manufacturing overhead cost allocation model. You believe that part of the problem FPD has with its existing range of household electrical products is inaccurate costing. Given the diversity in the range of electrical household products manufactured, FPD has contemplated switching the allocation of indirect manufacturing costs to an ABC system. Therefore, you decide to prepare an analysis on the usefulness of an ABC system for FPD by applying this approach to the three different food processor models. Analysis of the $810,000 of indirect manufacturing costs indicates that they can be classified into four broad cost pools, with four different cost drivers. The budgeted indirect manufacturing costs for the food processor product line for next year are shown in the following table. Indirect manufacturing cost pool Cost Driver Annual budgeted costs $270,000 Labour-related costs Direct labour hours (DLHS) Machine-related costs Machine hours $350,000 $120,000 $70,000 $810,000 Product scheduling and other set-up costs Materials handling costs Production runs Materials movements Total budgeted costs for all cost pools Budgeted production details for the food processor product line for next year are summarised in the next table. Cost driver transactions Household Home Pro Chef Pro DLHS per unit Machine hours per unit Number of production runs 2 1.5 1.25 1 3 3 50 150 200 Number of materials movements 90 260 350 REQUIRED: Compute the predetermined overhead rate under the traditional costing system, with direct labour hours (DLHS) as the cost driver. Calculate the product cost per unit for each of the three food processors using the traditional method of costing, with direct labour hours (DLH) as the cost driver. a. b. C. Using ABC, calculate the pool rates for each cost pool.

In your role as management accountant, you have been concerned about the division's manufacturing overhead cost allocation model. You believe that part of the problem FPD has with its existing range of household electrical products is inaccurate costing. Given the diversity in the range of electrical household products manufactured, FPD has contemplated switching the allocation of indirect manufacturing costs to an ABC system. Therefore, you decide to prepare an analysis on the usefulness of an ABC system for FPD by applying this approach to the three different food processor models. Analysis of the $810,000 of indirect manufacturing costs indicates that they can be classified into four broad cost pools, with four different cost drivers. The budgeted indirect manufacturing costs for the food processor product line for next year are shown in the following table. Indirect manufacturing cost pool Cost Driver Annual budgeted costs $270,000 Labour-related costs Direct labour hours (DLHS) Machine-related costs Machine hours $350,000 $120,000 $70,000 $810,000 Product scheduling and other set-up costs Materials handling costs Production runs Materials movements Total budgeted costs for all cost pools Budgeted production details for the food processor product line for next year are summarised in the next table. Cost driver transactions Household Home Pro Chef Pro DLHS per unit Machine hours per unit Number of production runs 2 1.5 1.25 1 3 3 50 150 200 Number of materials movements 90 260 350 REQUIRED: Compute the predetermined overhead rate under the traditional costing system, with direct labour hours (DLHS) as the cost driver. Calculate the product cost per unit for each of the three food processors using the traditional method of costing, with direct labour hours (DLH) as the cost driver. a. b. C. Using ABC, calculate the pool rates for each cost pool.

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter11: Differential Analysis And Product Pricing

Section: Chapter Questions

Problem 21E

Related questions

Question

Transcribed Image Text:In your role as management accountant, you have been concerned about the

division's manufacturing overhead cost allocation model. You believe that part of the

problem FPD has with its existing range of household electrical products is

inaccurate costing.

Given the diversity in the range of electrical household products manufactured, FPD

has contemplated switching the allocation of indirect manufacturing costs to an ABC

system. Therefore, you decide to prepare an analysis on the usefulness of an ABC

system for FPD by applying this approach to the three different food processor

models.

Analysis of the $810,000 of indirect manufacturing costs indicates that they can be

classified into four broad cost pools, with four different cost drivers. The budgeted

indirect manufacturing costs for the food processor product line for next year are

shown in the following table.

Indirect manufacturing cost pool

Cost Driver

Annual budgeted costs

$270,000

$350,000

$120,000

S70,000

$810,000

Labour-related costs

Direct labour hours (DLHS)

Machine-related costs

Machine hours

Product scheduling and other set-up costs

Materials handling costs

Production runs

Materials movements

Total budgeted costs for all cost pools

Budgeted production details for the food processor product line for next year are

summarised in the next table.

Chef Pro

1.25

Cost driver transactions

Household

Home Pro

DLHS per unit

Machine hours per unit

Number of production runs

2

1.5

1

3

50

150

200

Number of materials movements

90

260

350

REQUIRED:

Compute the predetermined overhead rate under the traditional costing

system, with direct labour hours (DLHS) as the cost driver.

Calculate the product cost per unit for each of the three food processors using

the traditional method of costing, with direct labour hours (DLH) as the cost

driver.

a.

b.

Using ABC, calculate the pool rates for each cost pool.

Using ABC, calculate the unit cost for each product.

From your analysis, determine whether FPD should follow William's

C.

d.

e.

recommendation.

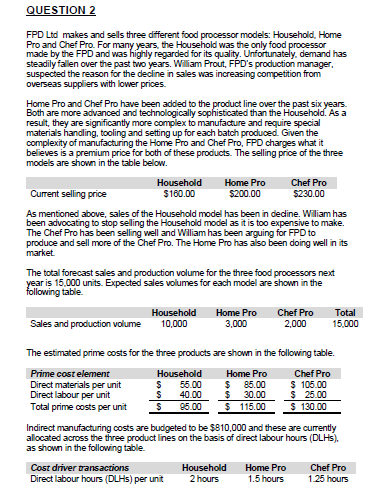

Transcribed Image Text:QUESTION 2

FPD Ltd makes and sells three different food processor models: Household, Home

Pro and Chef Pro. For many years, the Household was the only food processor

made by the FPD and was highly regarded for its quality. Unfortunately, demand has

steadily fallen over the past two years. William Prout, FPD's production manager,

suspected the reason for the decline in sales was increasing competition from

overseas suppliers with lower prices.

Home Pro and Chef Pro have been added to the product line over the past six years.

Both are more advanced and technologically sophisticated than the Household. As a

result, they are significantly more complex to manufacture and require special

materials handling, tooling and setting up for each batch produced. Given the

complexity of manufacturing the Home Pro and Chef Pro, FPD charges what it

believes is a premium price for both of these products. The selling price of the three

models are shown in the table below.

Home Pro

$200.00

Household

Chef Pro

Current selling price

$160.00

$230.00

As mentioned above, sales of the Household model has been in dedine. Wiliam has

been advocating to stop selling the Household model as it is too expensive to make.

The Chef Pro has been selling well and William has been arguing for FPD to

produce and sell more of the Chef Pro. The Home Pro has also been doing well in its

market.

The total forecast sales and production volume for the three food processors next

year is 15,000 units. Expected sales volumes for each model are shown in the

following table.

Household

10,000

Home Pro

3,000

Chef Pro

Total

Sales and production volume

2,000

15,000

The estimated prime costs for the three products are shown in the following table.

Prime cost element

Direct materials per unit

Direct labour per unit

Total prime costs per unit

Household

Home Pro

Chef Pro

55.00

$ 40.00

$ 85.00

$ 30.00

$ 115.00

$ 105.00

$ 25.00

$ 130.00

95.00

Indirect manufacturing costs are budgeted to be $810,000 and these are currently

allocated across the three product lines on the basis of direct labour hours (DLHS).

as shown in the following table.

Cost driver transactions

Household

Home Pro

Chef Pro

Direct labour hours (DLHS) per unit

2 hours

1.5 hours

1.25 hours

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 6 images

Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Accounting Information Systems

Accounting

ISBN:

9781337619202

Author:

Hall, James A.

Publisher:

Cengage Learning,