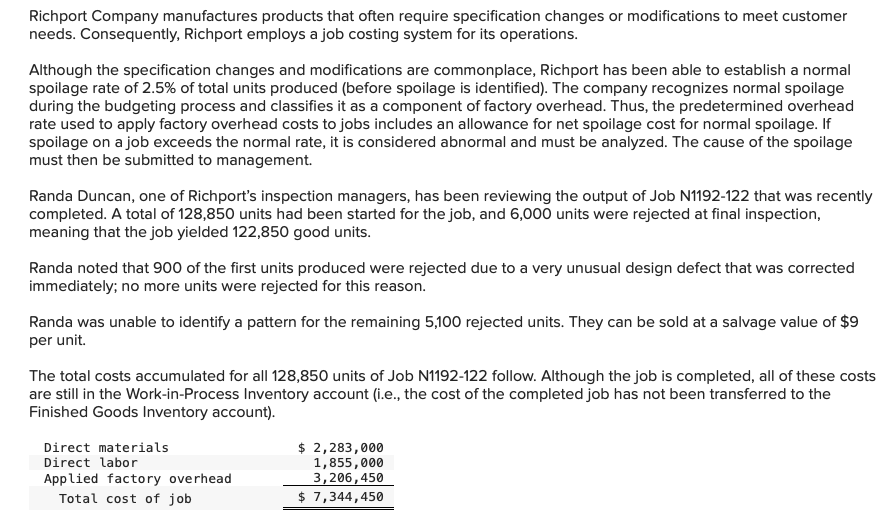

Richport Company manufactures products that often require specification changes or modifications to meet customer needs. Consequently, Richport employs a job costing system for its operations. Although the specification changes and modifications are commonplace, Richport has been able to establish a normal spoilage rate of 2.5% of total units produced (before spoilage is identified). The company recognizes normal spoilage during the budgeting process and classifies it as a component of factory overhead. Thus, the predetermined overhead rate used to apply factory overhead costs to jobs includes an allowance for net spoilage cost for normal spoilage. If spoilage on a job exceeds the normal rate, it is considered abnormal and must be analyzed. The cause of the spoilage must then be submitted to management. Randa Duncan, one of Richport's inspection managers, has been reviewing the output of Job N1192-122 that was recently completed. A total of 128,850 units had been started for the job, and 6,000 units were rejected at final inspection, meaning that the job yielded 122,850 good units. Randa noted that 900 of the first units produced were rejected due to a very unusual design defect that was corrected immediately; no more units were rejected for this reason. Randa was unable to identify a pattern for the remaining 5,100 rejected units. They can be sold at a salvage value of $9 per unit. The total costs accumulated for all 128,850 units of Job N1192-122 follow. Although the job is completed, all of these costs are still in the Work-in-Process Inventory account (i.e., the cost of the completed job has not been transferred to the Finished Goods Inventory account). $ 2,283,000 1,855,000 3,206,450 $ 7,344,450 Direct materials Direct labor Applied factory overhead Total cost of job

Richport Company manufactures products that often require specification changes or modifications to meet customer needs. Consequently, Richport employs a job costing system for its operations. Although the specification changes and modifications are commonplace, Richport has been able to establish a normal spoilage rate of 2.5% of total units produced (before spoilage is identified). The company recognizes normal spoilage during the budgeting process and classifies it as a component of factory overhead. Thus, the predetermined overhead rate used to apply factory overhead costs to jobs includes an allowance for net spoilage cost for normal spoilage. If spoilage on a job exceeds the normal rate, it is considered abnormal and must be analyzed. The cause of the spoilage must then be submitted to management. Randa Duncan, one of Richport's inspection managers, has been reviewing the output of Job N1192-122 that was recently completed. A total of 128,850 units had been started for the job, and 6,000 units were rejected at final inspection, meaning that the job yielded 122,850 good units. Randa noted that 900 of the first units produced were rejected due to a very unusual design defect that was corrected immediately; no more units were rejected for this reason. Randa was unable to identify a pattern for the remaining 5,100 rejected units. They can be sold at a salvage value of $9 per unit. The total costs accumulated for all 128,850 units of Job N1192-122 follow. Although the job is completed, all of these costs are still in the Work-in-Process Inventory account (i.e., the cost of the completed job has not been transferred to the Finished Goods Inventory account). $ 2,283,000 1,855,000 3,206,450 $ 7,344,450 Direct materials Direct labor Applied factory overhead Total cost of job

Principles of Cost Accounting

17th Edition

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Edward J. Vanderbeck, Maria R. Mitchell

Chapter4: Accounting For Factory Overhead

Section: Chapter Questions

Problem 2P: Miller Minerals Co. manufactures a product that requires the use of a considerable amount of natural...

Related questions

Concept explainers

Variance Analysis

In layman's terms, variance analysis is an analysis of a difference between planned and actual behavior. Variance analysis is mainly used by the companies to maintain a control over a business. After analyzing differences, companies find the reasons for the variance so that the necessary steps should be taken to correct that variance.

Standard Costing

The standard cost system is the expected cost per unit product manufactured and it helps in estimating the deviations and controlling them as well as fixing the selling price of the product. For example, it helps to plan the cost for the coming year on the various expenses.

Topic Video

Question

Transcribed Image Text:Richport Company manufactures products that often require specification changes or modifications to meet customer

needs. Consequently, Richport employs a job costing system for its operations.

Although the specification changes and modifications are commonplace, Richport has been able to establish a normal

spoilage rate of 2.5% of total units produced (before spoilage is identified). The company recognizes normal spoilage

during the budgeting process and classifies it as a component of factory overhead. Thus, the predetermined overhead

rate used to apply factory overhead costs to jobs includes an allowance for net spoilage cost for normal spoilage. If

spoilage on a job exceeds the normal rate, it is considered abnormal and must be analyzed. The cause of the spoilage

must then be submitted to management.

Randa Duncan, one of Richport's inspection managers, has been reviewing the output of Job N1192-122 that was recently

completed. A total of 128,850 units had been started for the job, and 6,000 units were rejected at final inspection,

meaning that the job yielded 122,850 good units.

Randa noted that 900 of the first units produced were rejected due to a very unusual design defect that was corrected

immediately; no more units were rejected for this reason.

Randa was unable to identify a pattern for the remaining 5,100 rejected units. They can be sold at a salvage value of $9

per unit.

The total costs accumulated for all 128,850 units of Job N1192-122 follow. Although the job is completed, all of these costs

are still in the Work-in-Process Inventory account (i.e., the cost of the completed job has not been transferred to the

Finished Goods Inventory account).

$ 2,283,000

1,855,000

3,206,450

$ 7,344,450

Direct materials

Direct labor

Applied factory overhead

Total cost of job

Transcribed Image Text:a. Determine the normal input required to yield 122,850 good units.

b. Prepare an analysis separating the spoiled units into normal and abnormal spoilage.

c. Prepare the appropriate journal entries to account for Job N1192-122.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,