INseume that an investor has formed a portfolio of Awo nesets; aBset A and aset B,if he invested 30% of his weath in aSset A. Tf the return on asset A 1s 20% CInd the return on the gsset BB HDt, the weight of the weath invested in 13set B 1S. (a) 70% O we cannot find the weight d) 60% | Referring to question 1o above the portfolio's return 15 H0% () 30%

INseume that an investor has formed a portfolio of Awo nesets; aBset A and aset B,if he invested 30% of his weath in aSset A. Tf the return on asset A 1s 20% CInd the return on the gsset BB HDt, the weight of the weath invested in 13set B 1S. (a) 70% O we cannot find the weight d) 60% | Referring to question 1o above the portfolio's return 15 H0% () 30%

Chapter8: Risk And Rates Of Return

Section: Chapter Questions

Problem 7PROB

Related questions

Question

one question with two parts

Transcribed Image Text:0. Nssume that an investor ham formed a portfolio of

Hwo nesets; Bset A and aset B,if he invested

30% of his weath in asset A. Tf the return

Ion asset A s 20% Cind the return on the gsset

BB HDt, the weight of the wealth Invested in

13set B 1S.

70%

O we cannot find the weight

ld) 60%

(a)

3.

Referring to questLon 10 above,the porifolio's

return 15

(ay H0%

()34%

(0 30%

(d) 3T%

Expert Solution

Step 1

A mixture of different kinds of funds and securities for the investment is term as the portfolio.

Step 2

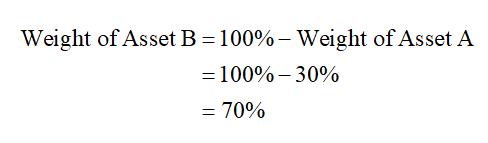

a.

Computation of the weight of Asset B:

Hence, option a is correct.

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you