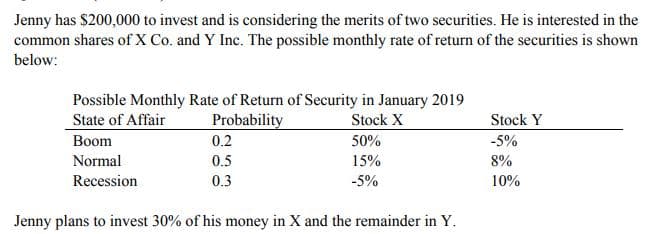

Jenny has $200,000 to invest and is considering the merits of two securities. He is interested in the common shares of X Co. and Y Inc. The possible monthly rate of return of the securities is shown below: Possible Monthly Rate of Return of Security in January 2019 State of Affair Stock X Stock Y Boom Normal Recession Probability 0.2 0.5 0.3 50% -5% 15% -5% 10% Jenny plans to invest 30% of his money in X and the remainder in Y.

(a) Calculate the expected rate of return, variance and standard deviation of Stock X & Stock Y.

(b) Assume that the covariance between Stock X and Stock Y is -0.005. Calculate the expected rate of return, variance and standard deviation of Jenny’s portfolio.

{Hint: you can express your answers for the variance and standard deviation in decimals or percentage form:

• For decimals, the covariance in your equation should be -0.005

• For percentage, the covariance in your equation should be -50%2

(= -50/10000)]

(c) Explain why, in general, the portfolio risk is lower than the weighted average of individual stocks’ risk.

(d) Suppose the risk-free rate is 4%, the market risk premium is 15% and the betas for stocks X and Y are 1.2 and 0.2 respectively. Using the

return

(e) Given the results above, are Stocks X and Y overpriced or underpriced? Explain.

Step by step

Solved in 5 steps with 8 images