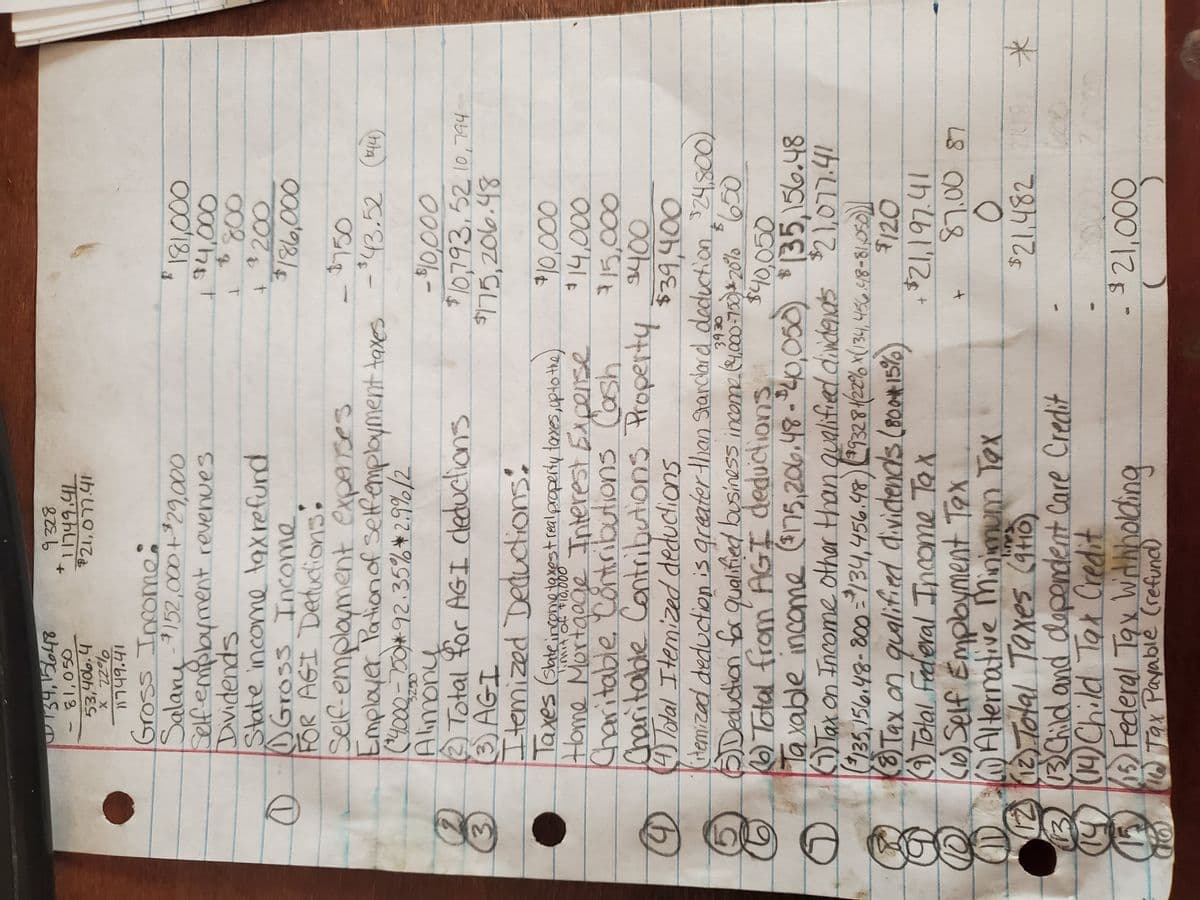

JUNII and Sahdy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: • State income taxes of $4,400. Federal tax withholding of $21,000. Alimony pay.nents to John's former wife of $10,000 (divorced 12/31/2014). • Child support payments for John's child with his former wife of $4.100. $12,200 of real property taxes. Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. •$3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. • $14,000 interest on their home mortgage ($400,000 acquisition debt). • $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. • $15,000 cash charitable contributions to qualified charities. Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost

JUNII and Sahdy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: • State income taxes of $4,400. Federal tax withholding of $21,000. Alimony pay.nents to John's former wife of $10,000 (divorced 12/31/2014). • Child support payments for John's child with his former wife of $4.100. $12,200 of real property taxes. Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. •$3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. • $14,000 interest on their home mortgage ($400,000 acquisition debt). • $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. • $15,000 cash charitable contributions to qualified charities. Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost

Chapter1: Financial Statements And Business Decisions

Section: Chapter Questions

Problem 1Q

Related questions

Question

What is the Fergusons' 2021 federal income taxes payable or refund, including any self-employment tax and AMT, if applicable?

Transcribed Image Text:1749.41

81,050

53,406.4

X 22%

749.41

to

7aו' Lh ULO

Gross Incomes

Salany-3152,000 +*29,000

Selfempbyment revenues

Dividends

State income taxrefund

D O Gross Income

FOR AGI Detuctions.

Self-emplayment experses

Employer, Pationof selfemployment taxes

(4000-00*92.35% *2.9%/2

1000

800

-43.52 (t14)

-$43.52

00000

*10,793,5210, 794

Total for AGI dleduclions

3.

3 AGI

Itemized Deductions:

Taxes (sateincenve texest realproperty taxes,uptothe)

$75,206.48

Charitable Contributions Cash

Charitable Contributions Property 400

D4otal Itemized deductionns

stemizad deduction is greater than Stanclard deduction 24.800)

पगंजकणा UMC+

1400

Total from AGI deductions

Ta xable income $75,206.48-40,050)

Tax on Income other Hhan qualified diidenats $21,077.41

135,156.48-800=/34,456.48)9328422% x(134, 486.418-81,I5)|

Tax an qualified divictends (80015%

$40,050

*(35,156.48

$120

(10)Self Empoyment Tex

122 Tolal Taxes (Gro)

3R Child and dapendent Care Credit

O 1)Child Tar Credit

) Federal Tax Withholhing

ng

Tax Payablé (refund)

$21.482 2418

00000

Transcribed Image Text:John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha.

In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and

Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does

some Web design work on the side and reported revenues of $4,000 and associated expenses of $750.

The Fergusons received $800 in qualified dividends and a $20O refund of their state income taxes. The

Fergusons always itemize their deductions, and their itemized deductions were well over the standard

deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021

individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate

Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference.

The Fergusons reported making the following payments during the year:

State income taxes of $4,400. Federal tax withholding of $21,000.

Alimony pay.ments to John's former wife of $10,000 (divorced 12/31/2014).

• Child support payments for John's child with his former wife of $4,100.

•$12,200 of real property taxes.

Sandy was reimbursed $600 for employee business expenses she incurred. She was required to

provide documentation for her expenses to her employer.

$3,600 to Kid Care day care center for Samantha's care while John and Sandy worked.

$14,000 interest on their home mortgage ($400,000 acquisition debt).

$3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and

new car.

$15,000 cash charitable contributions to qualified charities.

Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost

$2,000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Accounting

Accounting

ISBN:

9781337272094

Author:

WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:

Cengage Learning,

Accounting Information Systems

Accounting

ISBN:

9781337619202

Author:

Hall, James A.

Publisher:

Cengage Learning,

Accounting

Accounting

ISBN:

9781337272094

Author:

WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:

Cengage Learning,

Accounting Information Systems

Accounting

ISBN:

9781337619202

Author:

Hall, James A.

Publisher:

Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis…

Accounting

ISBN:

9780134475585

Author:

Srikant M. Datar, Madhav V. Rajan

Publisher:

PEARSON

Intermediate Accounting

Accounting

ISBN:

9781259722660

Author:

J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:

McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:

9781259726705

Author:

John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:

McGraw-Hill Education