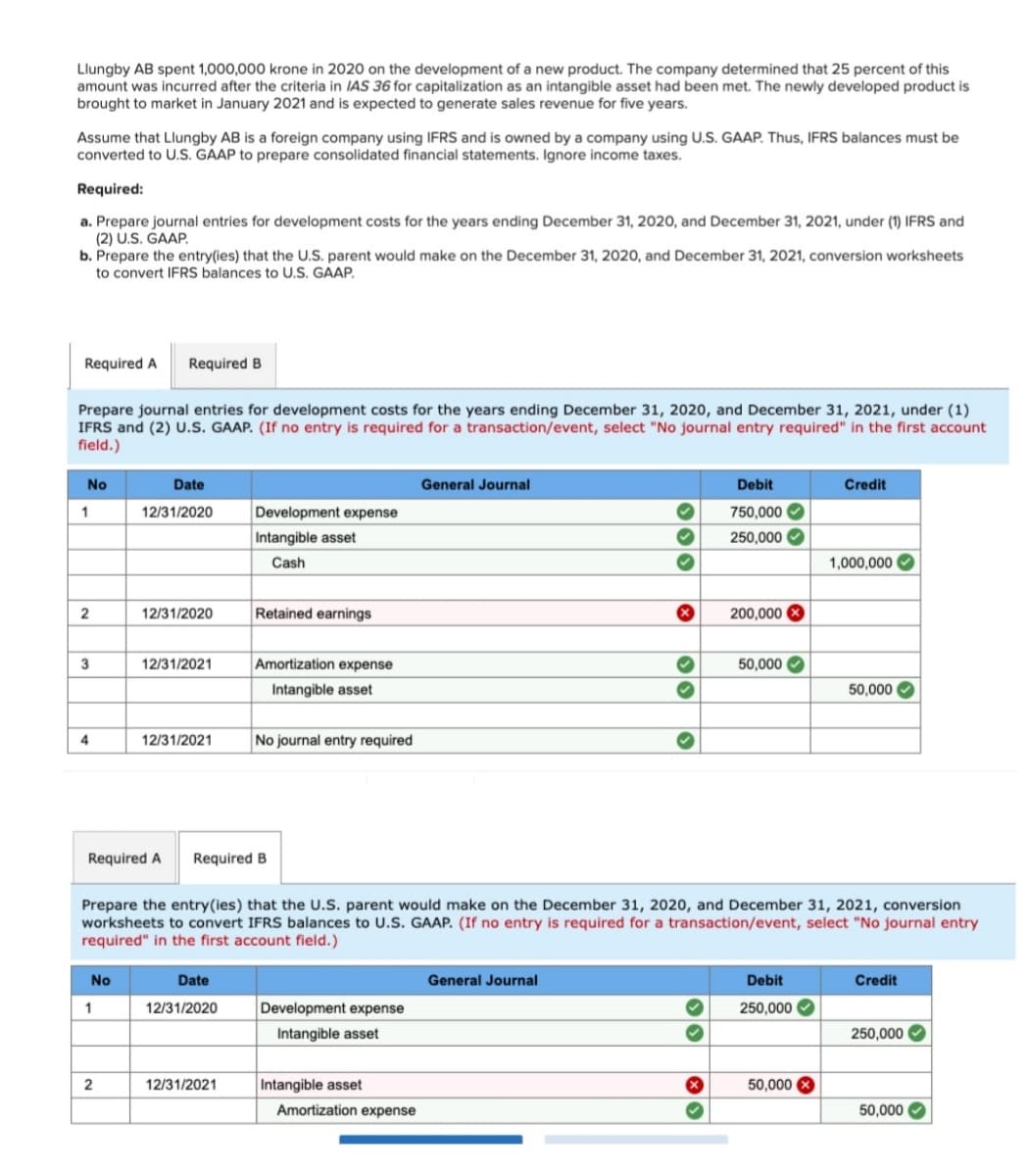

Llungby AB spent 1,000,000 krone in 2020 on the development of a new product. The company determined that 25 percent of this amount was incurred after the criteria in IAS 36 for capitalization as an intangible asset had been met. The newly developed product is brought to market in January 2021 and is expected to generate sales revenue for five years.

Llungby AB spent 1,000,000 krone in 2020 on the development of a new product. The company determined that 25 percent of this amount was incurred after the criteria in IAS 36 for capitalization as an intangible asset had been met. The newly developed product is brought to market in January 2021 and is expected to generate sales revenue for five years.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter11: Depreciation, Depletion, Impairment, And Disposal

Section: Chapter Questions

Problem 19P

Related questions

Question

Transcribed Image Text:Llungby AB spent 1,000,000 krone in 2020 on the development of a new product. The company determined that 25 percent of this

amount was incurred after the criteria in IAS 36 for capitalization as an intangible asset had been met. The newly developed product is

brought to market in January 2021 and is expected to generate sales revenue for five years.

Assume that Llungby AB is a foreign company using IFRS and is owned by a company using U.S. GAAP. Thus, IFRS balances must be

converted to U.S. GAAP to prepare consolidated financial statements. Ignore income taxes.

Required:

a. Prepare journal entries for development costs for the years ending December 31, 2020, and December 31, 2021, under (1) IFRS and

(2) U.S. GAAP.

b. Prepare the entry(ies) that the U.S. parent would make on the December 31, 2020, and December 31, 2021, conversion worksheets

to convert IFRS balances to U.S. GAAP.

Required A

Required B

Prepare journal entries for development costs for the years ending December 31, 2020, and December 31, 2021, under (1)

IFRS and (2) U.S. GAAP. (If no entry is required for a transaction/event, select "No journal entry required" in the first account

field.)

No

Date

General Journal

Debit

Credit

1

12/31/2020

Development expense

750,000 O

Intangible asset

250,000

Cash

1,000,000 O

12/31/2020

Retained earnings

200,000

3

12/31/2021

Amortization expense

50,000

Intangible asset

50,000

12/31/2021

No journal entry required

Required A

Required B

Prepare the entry(ies) that the U.S. parent would make on the December 31, 2020, and December 31, 2021, conversion

worksheets to convert IFRS balances to U.S. GAAP. (If no entry is required for a transaction/event, select "No journal entry

required" in the first account field.)

No

Date

General Journal

Debit

Credit

1

12/31/2020

Development expense

250,000 O

Intangible asset

250,000

2

12/31/2021

Intangible asset

50,000 X

Amortization expense

50,000 O

000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT