Melbourne Corporation was set up in 2016. The shareholders equity accounts of the company, with balances on 1 January 2018, are as follows: Share CapitalOrdinary, $20 par value (500,000 shares authorized, 375,000 shares issued and 350.000 shares outstanding) Share Capital-6% Cumulative Preference, no-par (150,000 shares authorized, 7.500,000 80,000 shares issued and outstanding)* Share Capital-8% Non -cumulative Preference, no-par (200,000 shares authorize 120,000 shares issued and outstanding) Share Premium 2,400,000 7,200,000 Retained Eamings 825,000 8,500,000 Treasury Share (25,000 shares, at cost) 450,000 All these shares were issued on 1 January 2016 The following shares transactions occurred during the year of 2018 Jan Issued 30,000 non-cumulative preference shares at S60 Apr 10 Issued 10,000 ordinary shares at $21 Jun 6 Sold 25,000 treasury share for $24 per share July Issued 26,000 cumulative preference shares at $30 23 Purchased 21,000 shares of treasury share for S18 per share 1 Nov Dec 1 Sold 13,000 treasury share for $15 per share Dec 28 Declared So.05 dividend per ordinary share Dec 31 Declared dividend for all the preference shares While there is no outstanding dividends before 2017 No dividend was paid for the year of 2017 for all the preference shares 雖然2017年之前,沒有欠付任何股息,但白2017年起,並無付任何優先股股息 REQUIRED: Calculate the outstanding shares of each class of share capital at 31 December, 2018 Calculate the total dividends for each class of share capital at 31 December, 2018 Journalize the entries to record all the transactions Prepare a statement of retained earnings for the year ended December 31, 2018 assume that the net profit for the year was $720,000 Prepare the Shareholders' Equity section of the statement of financial position. as at 31 December, 2018

Melbourne Corporation was set up in 2016. The shareholders equity accounts of the company, with balances on 1 January 2018, are as follows: Share CapitalOrdinary, $20 par value (500,000 shares authorized, 375,000 shares issued and 350.000 shares outstanding) Share Capital-6% Cumulative Preference, no-par (150,000 shares authorized, 7.500,000 80,000 shares issued and outstanding)* Share Capital-8% Non -cumulative Preference, no-par (200,000 shares authorize 120,000 shares issued and outstanding) Share Premium 2,400,000 7,200,000 Retained Eamings 825,000 8,500,000 Treasury Share (25,000 shares, at cost) 450,000 All these shares were issued on 1 January 2016 The following shares transactions occurred during the year of 2018 Jan Issued 30,000 non-cumulative preference shares at S60 Apr 10 Issued 10,000 ordinary shares at $21 Jun 6 Sold 25,000 treasury share for $24 per share July Issued 26,000 cumulative preference shares at $30 23 Purchased 21,000 shares of treasury share for S18 per share 1 Nov Dec 1 Sold 13,000 treasury share for $15 per share Dec 28 Declared So.05 dividend per ordinary share Dec 31 Declared dividend for all the preference shares While there is no outstanding dividends before 2017 No dividend was paid for the year of 2017 for all the preference shares 雖然2017年之前,沒有欠付任何股息,但白2017年起,並無付任何優先股股息 REQUIRED: Calculate the outstanding shares of each class of share capital at 31 December, 2018 Calculate the total dividends for each class of share capital at 31 December, 2018 Journalize the entries to record all the transactions Prepare a statement of retained earnings for the year ended December 31, 2018 assume that the net profit for the year was $720,000 Prepare the Shareholders' Equity section of the statement of financial position. as at 31 December, 2018

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter16: Retained Earnings And Earnings Per Share

Section: Chapter Questions

Problem 5MC: Kent Corporation was organized on January 1, 2014. On that date, it issued 200,000 shares of 10 par...

Related questions

Question

100%

how to do this questions? thanksssss!!

Transcribed Image Text:Melbourne Corporation was set up in 2016. The shareholders equity accounts

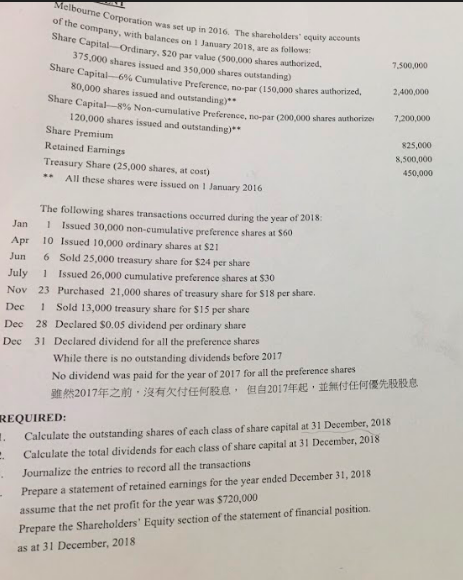

of the company, with balances on 1 January 2018, are as follows:

Share CapitalOrdinary, $20 par value (500,000 shares authorized,

375,000 shares issued and 350.000 shares outstanding)

Share Capital-6% Cumulative Preference, no-par (150,000 shares authorized,

7.500,000

80,000 shares issued and outstanding)*

Share Capital-8% Non -cumulative Preference, no-par (200,000 shares authorize

120,000 shares issued and outstanding)

Share Premium

2,400,000

7,200,000

Retained Eamings

825,000

8,500,000

Treasury Share (25,000 shares, at cost)

450,000

All these shares were issued on 1 January 2016

The following shares transactions occurred during the year of 2018

Jan

Issued 30,000 non-cumulative preference shares at S60

Apr

10 Issued 10,000 ordinary shares at $21

Jun

6

Sold 25,000 treasury share for $24 per share

July

Issued 26,000 cumulative preference shares at $30

23 Purchased 21,000 shares of treasury share for S18 per share

1

Nov

Dec

1

Sold 13,000 treasury share for $15 per share

Dec

28 Declared So.05 dividend per ordinary share

Dec

31

Declared dividend for all the preference shares

While there is no outstanding dividends before 2017

No dividend was paid for the year of 2017 for all the preference shares

雖然2017年之前,沒有欠付任何股息,但白2017年起,並無付任何優先股股息

REQUIRED:

Calculate the outstanding shares of each class of share capital at 31 December, 2018

Calculate the total dividends for each class of share capital at 31 December, 2018

Journalize the entries to record all the transactions

Prepare a statement of retained earnings for the year ended December 31, 2018

assume that the net profit for the year was $720,000

Prepare the Shareholders' Equity section of the statement of financial position.

as at 31 December, 2018

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781285866307

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning