Noelle Company began operations on January 1. Authorized were 120,000 shares of P10 par value ordinary shares and 240,000 shares of 10%, P100 par value preference shares. The following transactions involving shareholders' equity occurred during the first year of operations: Jan 1 Issued 30,000 ordinary shares to the corporation promoters in exchange for land valued at P1,020,000 and services valued at P420,000. The property had cost the promoters P540,000 three (3) years before and was carried on the promoters' books at P300,000. Feb 23 Issued 60,000 preference shares with a par value of P100 per share. The shares were issued at a price of P150 per share, and the company paid P450,000 to an agent for selling the shares. Mar 10 Sold 18,000 ordinary shares for P390 per share. Issue costs were P150,000. 24,000 ordinary shares were sold under share subscriptions at P450 per share. No shares are issued until full payment of a subscription contract. No cash was received as a down payment. Apr 10 July 14 Exchanged 4,200 ordinary shares and 8,400 preference shares for a building with a fair value of P3,060,000. In addition, 3,600 ordinary shares were sold for P1,440,000 in cash. Aug. 3 Received payments in full for half of the share subscriptions and payments on account on the rest of the subscriptions. Total cash received was P8,400,000. Share certificates were issued for the subscriptions paid in full. Dec 31 Net income for the first year of operations was P3,600,000. Declared a cash dividend of P10 per share on preference shares and P20 per share on ordinary shares, payable on February 10 to shareholders of record on January 15. Dec 31 Based on the preceding information: a. Prepare journal entries to record each transaction(

Noelle Company began operations on January 1. Authorized were 120,000 shares of P10 par value ordinary shares and 240,000 shares of 10%, P100 par value preference shares. The following transactions involving shareholders' equity occurred during the first year of operations: Jan 1 Issued 30,000 ordinary shares to the corporation promoters in exchange for land valued at P1,020,000 and services valued at P420,000. The property had cost the promoters P540,000 three (3) years before and was carried on the promoters' books at P300,000. Feb 23 Issued 60,000 preference shares with a par value of P100 per share. The shares were issued at a price of P150 per share, and the company paid P450,000 to an agent for selling the shares. Mar 10 Sold 18,000 ordinary shares for P390 per share. Issue costs were P150,000. 24,000 ordinary shares were sold under share subscriptions at P450 per share. No shares are issued until full payment of a subscription contract. No cash was received as a down payment. Apr 10 July 14 Exchanged 4,200 ordinary shares and 8,400 preference shares for a building with a fair value of P3,060,000. In addition, 3,600 ordinary shares were sold for P1,440,000 in cash. Aug. 3 Received payments in full for half of the share subscriptions and payments on account on the rest of the subscriptions. Total cash received was P8,400,000. Share certificates were issued for the subscriptions paid in full. Dec 31 Net income for the first year of operations was P3,600,000. Declared a cash dividend of P10 per share on preference shares and P20 per share on ordinary shares, payable on February 10 to shareholders of record on January 15. Dec 31 Based on the preceding information: a. Prepare journal entries to record each transaction(

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter15: Contributed Capital

Section: Chapter Questions

Problem 2MC: Cary Corporation has 50,000 shares of 10 par common stock authorized. The following transactions...

Related questions

Question

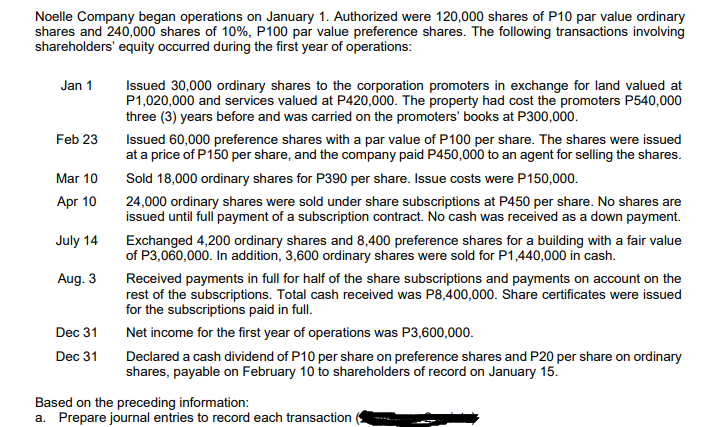

Transcribed Image Text:Noelle Company began operations on January 1. Authorized were 120,000 shares of P10 par value ordinary

shares and 240,000 shares of 10%, P100 par value preference shares. The following transactions involving

shareholders' equity occurred during the first year of operations:

Issued 30,000 ordinary shares to the corporation promoters in exchange for land valued at

P1,020,000 and services valued at P420,000. The property had cost the promoters P540,000

three (3) years before and was carried on the promoters' books at P300,000.

Jan 1

Feb 23

Issued 60,000 preference shares with a par value of P100 per share. The shares were issued

at a price of P150 per share, and the company paid P450,000 to an agent for selling the shares.

Mar 10

Sold 18,000 ordinary shares for P390 per share. Issue costs were P150,000.

Apr 10

24,000 ordinary shares were sold under share subscriptions at P450 per share. No shares are

issued until full payment of a subscription contract. No cash was received as a down payment.

July 14

Exchanged 4,200 ordinary shares and 8,400 preference shares for a building with a fair value

of P3,060,000. In addition, 3,600 ordinary shares were sold for P1,440,000 in cash.

Aug. 3

Received payments in full for half of the share subscriptions and payments on account on the

rest of the subscriptions. Total cash received was P8,400,000. Share certificates were issued

for the subscriptions paid in full.

Dec 31

Net income for the first year of operations was P3,600,000.

Dec 31

Declared a cash dividend of P10 per share on preference shares and P20 per share on ordinary

shares, payable on February 10 to shareholders of record on January 15.

Based on the preceding information:

a. Prepare journal entries to record each transaction

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,