ntegrating Case 7-7 Change in estimate of bad debts ALO7-5 McLaughlin Corporation uses the allowance method to account for bad debts. At the end of the company's fiscal year, accounts receivable are analyzed and the allowance for uncollectible accounts is adjusted. At the end of 2021, the company reported the following amounts: Accounts receivable $ 10,850,000 Less: Allowance for uncollectible accounts (450,000) Accounts receivable, net $ 10,400,000 In 2022, it was determined that $1,825,000 of year-end 2021 receivables had to be written off as uncollectible. This was due in part Page 398 co the fact that Hughes Corporation, a long-standing customer that had always paid its bills, unexpectedly declared bankruptcy in 2022. Hughes owed McLaughlin $1,400,000. At the end of 2021, none of the Hughes receivable was considered uncollectible. Required: Should McLaughlin's underestimation of bad debts be treated as an error correction (requiring retroactive restatement) or a change in estimate and accounted for prospectively)? Describe the appropriate accounting treatment and required disclosures in the financial statements issued For the 2021 fiscal year.

ntegrating Case 7-7 Change in estimate of bad debts ALO7-5 McLaughlin Corporation uses the allowance method to account for bad debts. At the end of the company's fiscal year, accounts receivable are analyzed and the allowance for uncollectible accounts is adjusted. At the end of 2021, the company reported the following amounts: Accounts receivable $ 10,850,000 Less: Allowance for uncollectible accounts (450,000) Accounts receivable, net $ 10,400,000 In 2022, it was determined that $1,825,000 of year-end 2021 receivables had to be written off as uncollectible. This was due in part Page 398 co the fact that Hughes Corporation, a long-standing customer that had always paid its bills, unexpectedly declared bankruptcy in 2022. Hughes owed McLaughlin $1,400,000. At the end of 2021, none of the Hughes receivable was considered uncollectible. Required: Should McLaughlin's underestimation of bad debts be treated as an error correction (requiring retroactive restatement) or a change in estimate and accounted for prospectively)? Describe the appropriate accounting treatment and required disclosures in the financial statements issued For the 2021 fiscal year.

Financial & Managerial Accounting

14th Edition

ISBN:9781337119207

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Carl Warren, James M. Reeve, Jonathan Duchac

Chapter8: Receivables

Section: Chapter Questions

Problem 8.14EX: Entries for bad debt expense under the direct write-off and allowance methods The following selected...

Related questions

Question

what is the definitions/general overview of error correction and a change in estimate

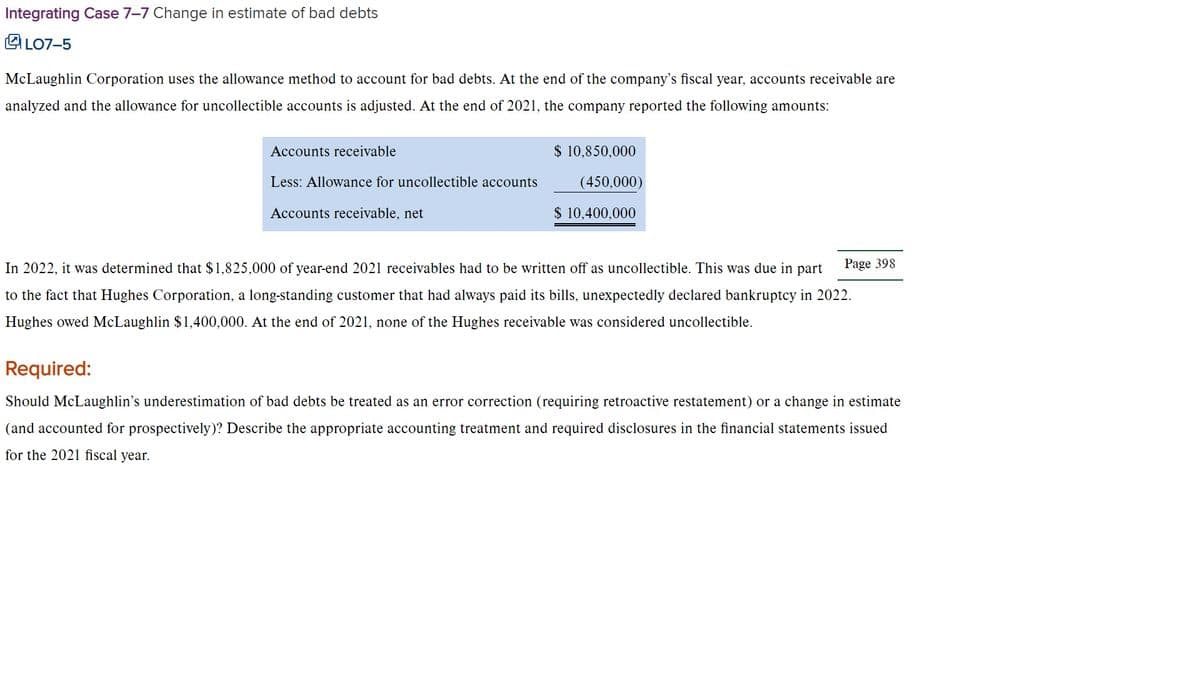

Transcribed Image Text:Integrating Case 7–7 Change in estimate of bad debts

LO7-5

McLaughlin Corporation uses the allowance method to account for bad debts. At the end of the company's fiscal year, accounts receivable are

analyzed and the allowance for uncollectible accounts is adjusted. At the end of 2021, the company reported the following amounts:

Accounts receivable

$ 10,850,000

Less: Allowance for uncollectible accounts

(450,000)

Accounts receivable, net

$ 10,400,000

In 2022, it was determined that $1,825,000 of year-end 2021 receivables had to be written off as uncollectible. This was due in part

Page 398

to the fact that Hughes Corporation, a long-standing customer that had always paid its bills, unexpectedly declared bankruptcy in 2022.

Hughes owed McLaughlin $1,400,000. At the end of 2021, none of the Hughes receivable was considered uncollectible.

Required:

Should McLaughlin's underestimation of bad debts be treated as an error correction (requiring retroactive restatement) or a change in estimate

(and accounted for prospectively)? Describe the appropriate accounting treatment and required disclosures in the financial statements issued

for the 2021 fiscal year.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

Financial & Managerial Accounting

Accounting

ISBN:

9781337119207

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:

9781305653535

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781337119207

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:

9781305653535

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning