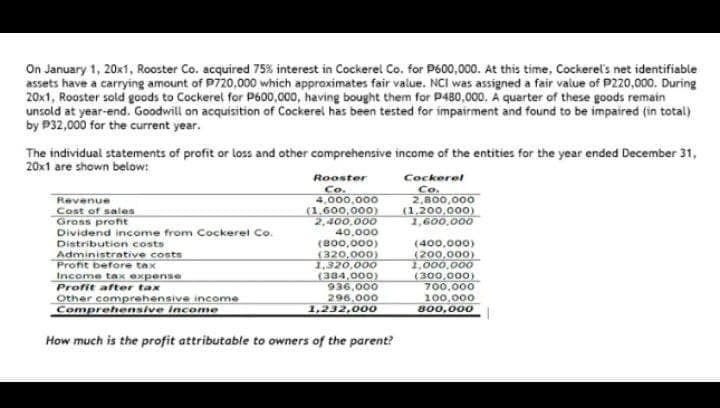

On January 1, 20x1, Rooster Co. acquired 75% interest in Cockerel Co. for P600,000. At this time, Cockerel's net identifiable assets have a carrying amount of P720,000 which approximates fair value. NCI was assigned a fair value of P220,000. During 20x1, Rooster sold goods to Cockerel for P600,000, having bought them for p480,000. A quarter of these goods remain unsold at year-end. Goodwill on acquisition of Cockerel has been tested for impairment and found to be impaired (in total) by P32,000 for the current year. The individual statements of profit or loss and other comprehensive income of the entities for the year ended December 31, 20x1 are shown below: Rooster Co. 4,000,000 (1,600,000) 2,400,000 40,000 Cockerel Co. 2,800,000 (1,200,000) 1,600,000 Revenue Cost of sales Gross proft Dividend income from Cockerel Co. Distribution costs Administrative costs Profit before tax Income taK expense (B00,000) (320,000) 1,320,000 (384,000) 936.000 296.000 1,232,00o (400,000) (200,000) 1,000,000 (300,000) 700,000 100,000 800,000 Profit after tax Other comprehensive income Comprehensive income How much is the profit attributable to owners of the parent?

On January 1, 20x1, Rooster Co. acquired 75% interest in Cockerel Co. for P600,000. At this time, Cockerel's net identifiable assets have a carrying amount of P720,000 which approximates fair value. NCI was assigned a fair value of P220,000. During 20x1, Rooster sold goods to Cockerel for P600,000, having bought them for p480,000. A quarter of these goods remain unsold at year-end. Goodwill on acquisition of Cockerel has been tested for impairment and found to be impaired (in total) by P32,000 for the current year. The individual statements of profit or loss and other comprehensive income of the entities for the year ended December 31, 20x1 are shown below: Rooster Co. 4,000,000 (1,600,000) 2,400,000 40,000 Cockerel Co. 2,800,000 (1,200,000) 1,600,000 Revenue Cost of sales Gross proft Dividend income from Cockerel Co. Distribution costs Administrative costs Profit before tax Income taK expense (B00,000) (320,000) 1,320,000 (384,000) 936.000 296.000 1,232,00o (400,000) (200,000) 1,000,000 (300,000) 700,000 100,000 800,000 Profit after tax Other comprehensive income Comprehensive income How much is the profit attributable to owners of the parent?

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter12: Intangibles

Section: Chapter Questions

Problem 18E

Related questions

Question

Transcribed Image Text:On January 1, 20x1, Rooster Co. acquired 75% interest in Cockerel Co, for P600,000. At this time, Cockerel's net identifiable

assets have a carrying amount of P720,000 which approximates fair value. NCI was assigned a fair value of P220,000. During

20x1, Rooster sold goods to Cockerel for P600,000, having bought them for P480,000. A quarter of these goods remain

unsold at year-end. Goodwill on acquisition of Cockerel has been tested for impairment and found to be impaired (in total)

by P32,000 for the current year.

The individual statements of profit or loss and other comprehensive income of the entities for the year ended December 31,

20x1 are shown below:

Rooster

Co.

4,000,000

(1,600,000)

2,400,000

40,000

(B00,000)

(320,000)

1,320,000

(384,000)

936,000

296.000

1,232,000

Cockerel

Co.

2,800,000

(1,200.000)

1,600,000

Revenue

Cost of sales

Gross profnt

Dividend income from Cockerel Co.

Distributicn costs

(400,000)

(200,000)

1,000,000

(300,000)

700,000

100,000

800,000

Administrative costs

Profit before tax

Income tax expense

Profit after tax

Other comprehensive income

Comprehensive Income

How much is the profit attributable to owners of the parent?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 1 images

Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning