Please help me solve this problem; If the portfolio is 500,000, with the significance level of 1%, what would be the absolute value of the portfolio with the 99% confidence level? Refer to table in the given picture for your reference in answering the above question.

Please help me solve this problem; If the portfolio is 500,000, with the significance level of 1%, what would be the absolute value of the portfolio with the 99% confidence level? Refer to table in the given picture for your reference in answering the above question.

Chapter3: Evaluation Of Financial Performance

Section: Chapter Questions

Problem 10P

Related questions

Question

Please help me solve this problem;

If the portfolio is 500,000, with the significance level of 1%, what would be the absolute value of the portfolio with the 99% confidence level?

Refer to table in the given picture for your reference in answering the above question.

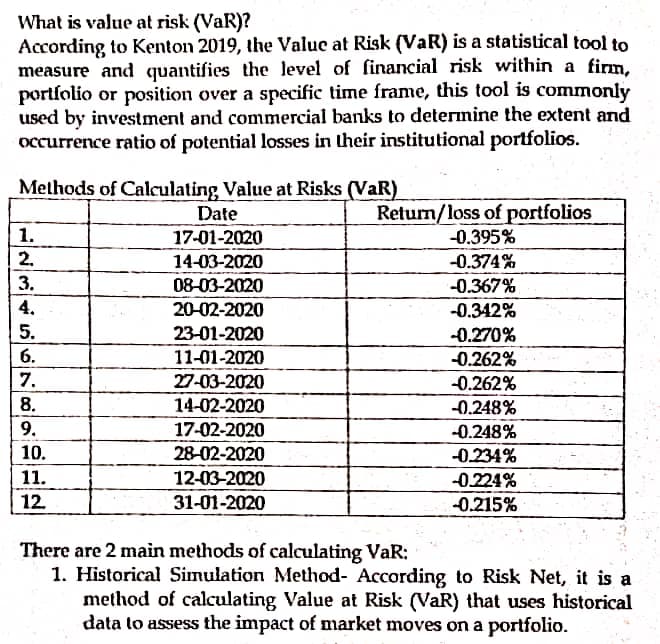

Transcribed Image Text:What is value at risk (VaR)?

According to Kenton 2019, the Value at Risk (VaR) is a statistical tool to

measure and quantifies the level of financial risk within a firm,

portfolio or position over a specific time frame, this tool is commonly

used by investment and commercial banks to determine the extent and

occurrence ratio of potential losses in their institutional portfolios.

Methods of Calculating Value at Risks (VaR)

Date

17-01-2020

Return/loss of portfolios

-0.395%

1.

2.

14-03-2020

-0.374%

3.

08-03-2020

-0.367%

4.

20-02-2020

-0.342%

5.

23-01-2020

-0.270%

6.

11-01-2020

-0.262%

7.

27-03-2020

-0.262%

8.

14-02-2020

-0.248%

9.

17-02-2020

-0.248%

10.

28-02-2020

-0.234%

11.

12-03-2020

-0.224%

12.

31-01-2020

-0.215%

There are 2 main methods of calculating VaR:

1. Historical Simulation Method- According to Risk Net, it is a

method of calculating Value at Risk (VaR) that uses historical

data to assess the impact of market moves on a portfolio.

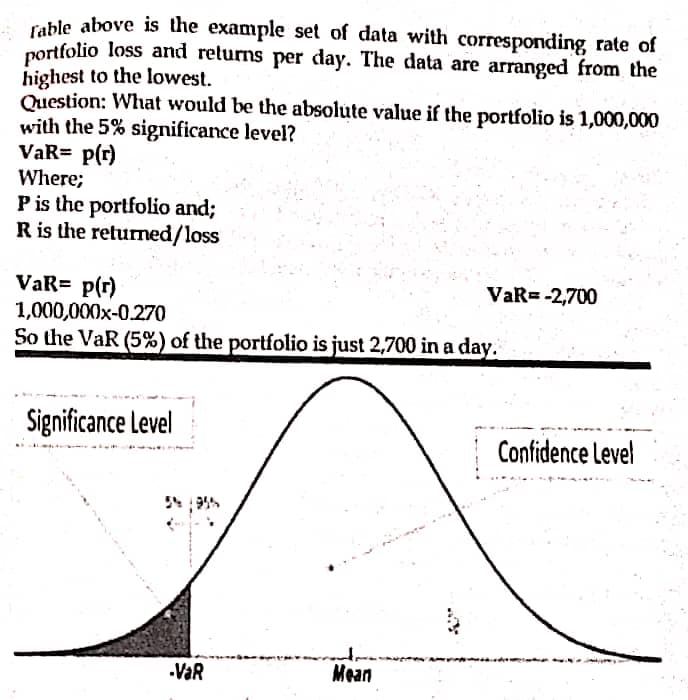

Transcribed Image Text:Table above is the example set of data with corresponding rate of

portfolio loss and returns per day. The data are arranged from the

highest to the lowest.

Question: What would be the absolute value if the portfolio is 1,000,000

with the 5% significance level?

VaR= p(r)

Where;

Pis the portfolio and;

R is the returned/loss

VaR= p(r)

1,000,000x-0.270

So the VaR (5%) of the portfolio is just 2,700 in a day.

VaR= -2,700

Significance Level

Confidence Level

VaR

Mean

..

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 5 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning