Post the journal to a ledger of four-column accounts. Add the appropriate posting reference to the journal.

Post the journal to a ledger of four-column accounts. Add the appropriate posting reference to the journal.

Corporate Financial Accounting

14th Edition

ISBN:9781305653535

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Carl Warren, James M. Reeve, Jonathan Duchac

Chapter4: Completing The Accounting Cycle

Section: Chapter Questions

Problem 1CP: The unadjusted trial balance of PS Music as of July 31, 2018, along with the adjustment data for the...

Related questions

Question

2. Post the journal to a ledger of four-column accounts. Add the appropriate posting reference to the journal. 6. b. Post the adjusting entries , inserting balances in the accounts affected. 9. b. Post the closing entries, inserting balances in the accounts affected. Leave the ITEM column BLANK for each row. If the account balance is zero (0) after closing entries are posted , enter a zero (0) in the account's normal balance column.

LEDGER

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| DATE | ITEM | POST. REF. | DEBIT | CREDIT | BALANCE | ||

|---|---|---|---|---|---|---|---|

| DEBIT | CREDIT | ||||||

|

1

|

|

|

|

|

|

|

|

|

2

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

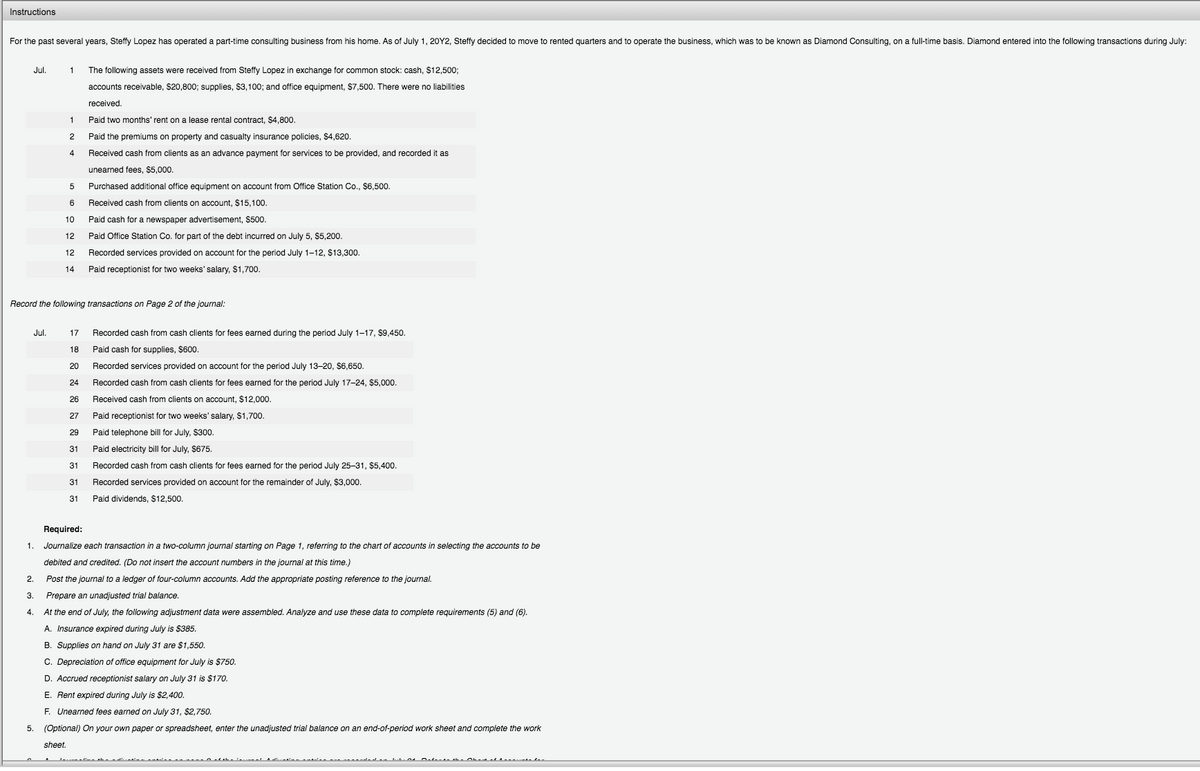

Transcribed Image Text:Instructions

For the past several years, Steffy Lopez has operated a part-time consulting business from his home. As of July 1, 20Y2, Steffy decided to move to rented quarters and to operate the business, which was to be known as Diamond Consulting, on a full-time basis. Diamond entered into the following transactions during July:

Jul.

1

The following assets were received from Steffy Lopez in exchange for common stock: cash, $12,500;

accounts receivable, $20,800; supplies, $3,100; and office equipment, $7,500. There were no liabilities

received.

1

Paid two months' rent on a lease rental contract, $4,800.

2

Paid the premiums on property and casualty insurance policies, $4,620.

4

Received cash from clients as an advance payment for services to be provided, and recorded it as

unearned fees, $5,000.

Purchased additional office equipment on account from Office Station Co., $6,500.

6

Received cash from clients on account, $15,100.

10

Paid cash for a newspaper advertisement, $500.

12

Paid Office Station Co. for part of the debt incurred on July 5, $5,200.

12

Recorded services provided on account for the period July 1-12, $13,300.

14

Paid receptionist for two weeks' salary, $1,700.

Record the following transactions on Page 2 of the journal:

Jul.

17

Recorded cash from cash clients for fees earned during the period July 1-17, $9,450.

18

Paid cash for supplies, $600.

20

Recorded services provided on account for the period July 13-20, $6,650.

24

Recorded cash from cash clients for fees earned for the period July 17-24, $5,000.

26

Received cash from clients on account, $12,000.

27

Paid receptionist for two weeks' salary, $1,700.

29

Paid telephone bill for July, $300.

31

Paid electricity bill for July, $675.

31

Recorded cash from cash clients for fees earned for the period July 25-31, $5,400.

31

Recorded services provided on account for the remainder of July, $3,000.

31

Paid dividends, $12,500.

Required:

1.

Journalize each transaction in a two-column journal starting on Page 1, referring to the chart of accounts in selecting the accounts to be

debited and credited. (Do not insert the account numbers in the journal at this time.)

2.

Post the journal to a ledger of four-column accounts. Add the appropriate posting reference to the journal.

3.

Prepare an unadjusted trial balance.

4.

At the end of July, the following adjustment data were assembled. Analyze and use these data to complete requirements (5) and (6).

A. Insurance expired during July is $385.

B. Supplies on hand on July 31 are $1,550.

C. Depreciation of office equipment for July is $750.

D. Accrued receptionist salary on July 31 is $170.

E. Rent expired during July is $2,400.

F. Unearned fees earned on July 31, $2,750.

5. (Optional) On your own paper or spreadsheet, enter the unadjusted trial balance on an end-of-period work sheet and complete the work

sheet.

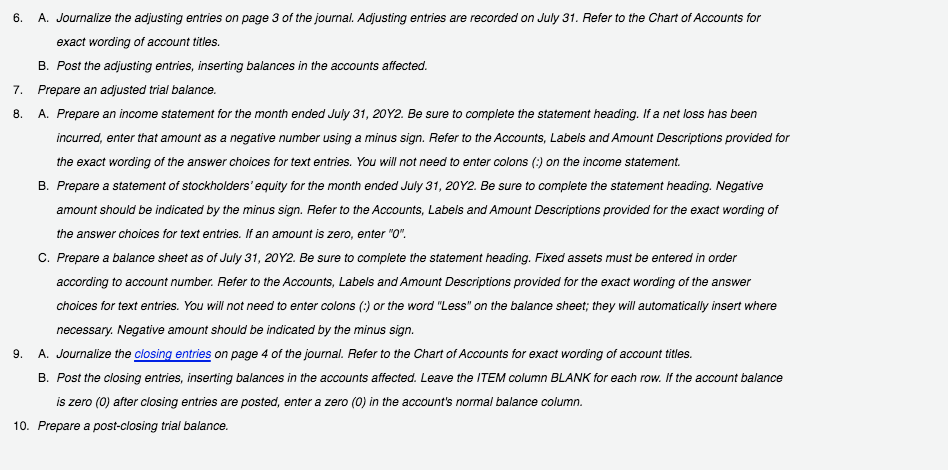

Transcribed Image Text:6.

A. Journalize the adjusting entries on page 3 of the journal. Adjusting entries are recorded on July 31. Refer to the Chart of Accounts for

exact wording of account titles.

B. Post the adjusting entries, inserting balances in the accounts affected.

7. Prepare an adjusted trial balance.

8.

A. Prepare an income statement for the month ended July 31, 20Y2. Be sure to complete the statement heading. If a net loss has been

incurred, enter that amount as a negative number using a minus sign. Refer to the Accounts, Labels and Amount Descriptions provided for

the exact wording of the answer choices for text entries. You will not need to enter colons (:) on the income statement.

B. Prepare a statement of stockholders' equity for the month ended July 31, 20Y2. Be sure to complete the statement heading. Negative

amount should be indicated by the minus sign. Refer to the Accounts, Labels and Amount Descriptions provided for the exact wording of

the answer choices for text entries. If an amount is zero, enter "O".

C. Prepare a balance sheet as of July 31, 20Y2. Be sure to complete the statement heading. Fixed assets must be entered in order

according to account number. Refer to the Accounts, Labels and Amount Descriptions provided for the exact wording of the answer

choices for text entries. You will not need to enter colons (:) or the word "Less" on the balance sheet; they will automatically insert where

necessary. Negative amount should be indicated by the minus sign.

9. A. Journalize the closing entries on page 4 of the journal. Refer to the Chart of Accounts for exact wording of account titles.

B. Post the closing entries, inserting balances in the accounts affected. Leave the ITEM column BLANK for each row. If the account balance

is zero (0) after closing entries are posted, enter a zero (0) in the account's normal balance column.

10. Prepare a post-closing trial balance.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 5 steps with 7 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Corporate Financial Accounting

Accounting

ISBN:

9781305653535

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:

9781305653535

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning