production of wine. In June 2021, it anticipated that its assets may be impaired due to a glu the market for grapes and an impending tax from the Australian government seeking to re binge drinking of alcohol by teenagers. Land is measured by Easter Ltd at fair value. At 30 June 2021, the entity revalued the land fair value of $120 000. The land had previously been revalued upwards by $20 000. The tax is 30%.

production of wine. In June 2021, it anticipated that its assets may be impaired due to a glu the market for grapes and an impending tax from the Australian government seeking to re binge drinking of alcohol by teenagers. Land is measured by Easter Ltd at fair value. At 30 June 2021, the entity revalued the land fair value of $120 000. The land had previously been revalued upwards by $20 000. The tax is 30%.

Chapter18: Corporations: Organization And Capital Structure

Section: Chapter Questions

Problem 38P

Related questions

Question

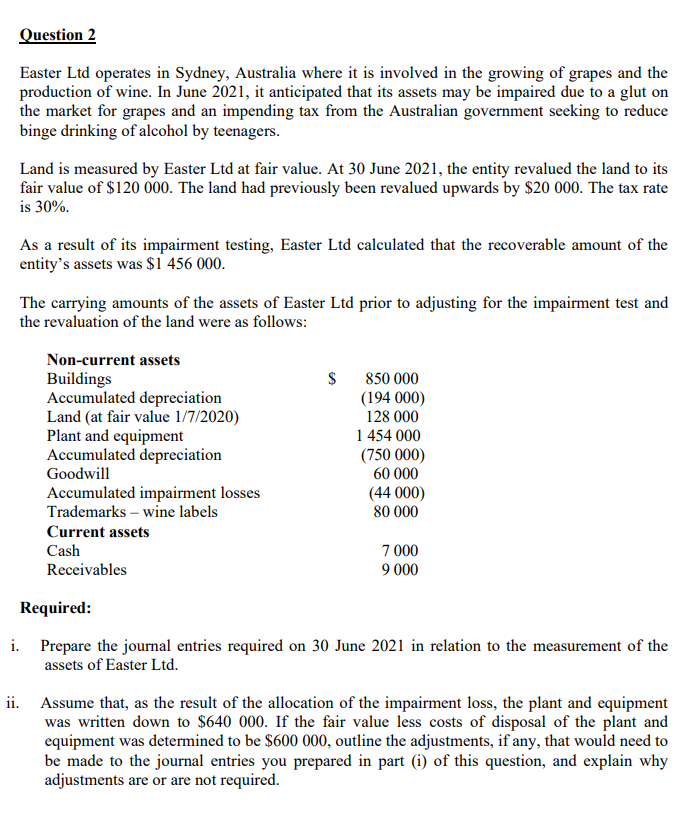

Transcribed Image Text:Question 2

Easter Ltd operates in Sydney, Australia where it is involved in the growing of grapes and the

production of wine. In June 2021, it anticipated that its assets may be impaired due to a glut on

the market for grapes and an impending tax from the Australian government seeking to reduce

binge drinking of alcohol by teenagers.

Land is measured by Easter Ltd at fair value. At 30 June 2021, the entity revalued the land to its

fair value of $120 000. The land had previously been revalued upwards by $20 000. The tax rate

is 30%.

As a result of its impairment testing, Easter Ltd calculated that the recoverable amount of the

entity's assets was $1 456 000.

The carrying amounts of the assets of Easter Ltd prior to adjusting for the impairment test and

the revaluation of the land were as follows:

Non-current assets

Buildings

Accumulated depreciation

Land (at fair value 1/7/2020)

Plant and equipment

Accumulated depreciation

Goodwill

$

850 000

(194 000)

128 000

1 454 000

(750 000)

60 000

Accumulated impairment losses

Trademarks – wine labels

(44 000)

80 000

Current assets

Cash

7 000

Receivables

9 000

Required:

i. Prepare the journal entries required on 30 June 2021 in relation to the measurement of the

assets of Easter Ltd.

ii. Assume that, as the result of the allocation of the impairment loss, the plant and equipment

was written down to $640 000. If the fair value less costs of disposal of the plant and

equipment was determined to be $600 000, outline the adjustments, if any, that would need to

be made to the journal entries you prepared in part (i) of this question, and explain why

adjustments are or are not required.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you