P(State) Consider the following information on two stocks: Stock A Stock B Boom 20% 30% 20% Normal 50% 12% -5% Slow 15% 4% 8% Recession 15% -10% 10% $Investment Beta Asset A $35,000 1.45 Asset B $15,000 0.85 Assuming a risk-free rate of 5%, calculate the portfolio's Sharpe Ratio. (Round to 4 decimals; hint: Sharpe ratio = (E(Ret) - Rf))/stdev).

P(State) Consider the following information on two stocks: Stock A Stock B Boom 20% 30% 20% Normal 50% 12% -5% Slow 15% 4% 8% Recession 15% -10% 10% $Investment Beta Asset A $35,000 1.45 Asset B $15,000 0.85 Assuming a risk-free rate of 5%, calculate the portfolio's Sharpe Ratio. (Round to 4 decimals; hint: Sharpe ratio = (E(Ret) - Rf))/stdev).

Chapter8: Risk And Rates Of Return

Section: Chapter Questions

Problem 10PROB

Related questions

Question

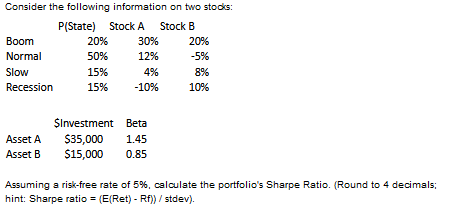

Transcribed Image Text:P(State)

Consider the following information on two stocks:

Stock A Stock B

Boom

20%

30%

20%

Normal

50%

12%

-5%

Slow

15%

4%

8%

Recession

15%

-10%

10%

$Investment Beta

Asset A $35,000 1.45

Asset B

$15,000

0.85

Assuming a risk-free rate of 5%, calculate the portfolio's Sharpe Ratio. (Round to 4 decimals;

hint: Sharpe ratio = (E(Ret) - Rf))/stdev).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 1 images

Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT