Q3 O Qi Total revenue O Q2 all quantities beyond Q1 Total cost Where on the graph does the firm earn zero economic profit? Q Q2 Q. Quantity O only Q2 only Q1 O both Q1 and Q3 O only Q3 Where on the graph is profit negative? O all quantities between Q1 and Q3 O only quantities more than Q3 O only quantities less than Q1 quantities less than Q1 or more than Q3

Q3 O Qi Total revenue O Q2 all quantities beyond Q1 Total cost Where on the graph does the firm earn zero economic profit? Q Q2 Q. Quantity O only Q2 only Q1 O both Q1 and Q3 O only Q3 Where on the graph is profit negative? O all quantities between Q1 and Q3 O only quantities more than Q3 O only quantities less than Q1 quantities less than Q1 or more than Q3

Chapter12: Firms In Perfectly Competitive Markets

Section: Chapter Questions

Problem 17P

Related questions

Question

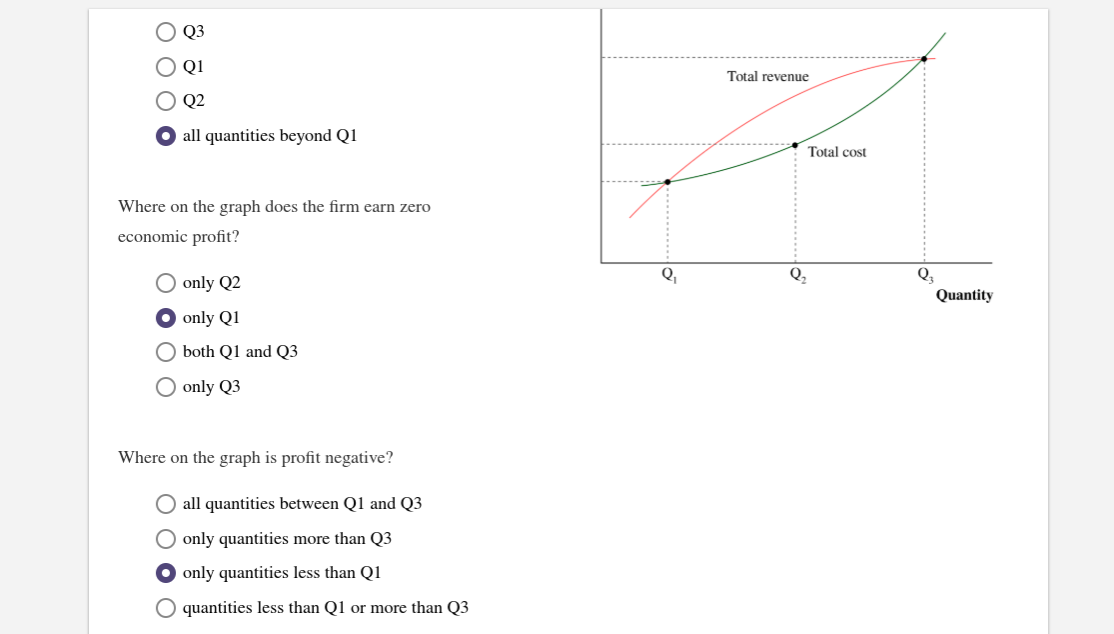

Transcribed Image Text:Q3

O Qi

Total revenue

O Q2

all quantities beyond Q1

Total cost

Where on the graph does the firm earn zero

economic profit?

Q

Q2

Q.

Quantity

O only Q2

only Q1

O both Q1 and Q3

O only Q3

Where on the graph is profit negative?

O all quantities between Q1 and Q3

O only quantities more than Q3

O only quantities less than Q1

quantities less than Q1 or more than Q3

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Recommended textbooks for you

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax