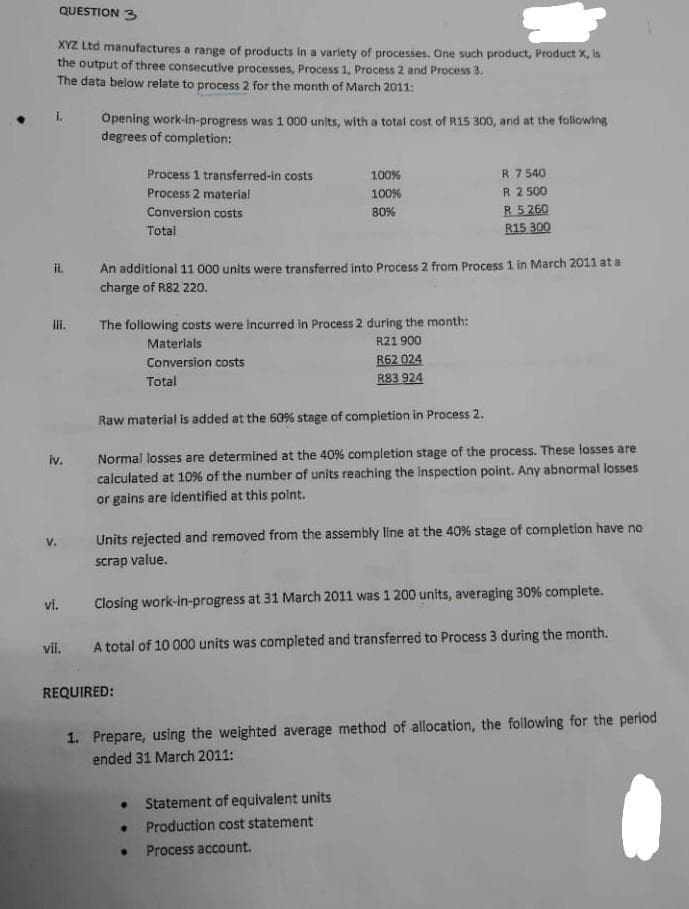

QUESTION 3 XYZ Ltd manufactures a range of products in a variety of processes. One such product, Product X, is the output of three consecutive processes, Process 1, Process 2 and Process 3. The data below relate to process 2 for the month of March 2011: it. III. iv. vi. vil. Opening work-in-progress was 1 000 units, with a total cost of R15 300, and at the following degrees of completion: Process 1 transferred-in costs Process 2 material Conversion costs Total The following costs were incurred in Process 2 during the month: R21 900 R62 024 R83.924 100% 100% 80% An additional 11 000 units were transferred into Process 2 from Process 1 in March 2011 at a charge of R82 220. Materials Conversion costs Total REQUIRED: R 7540 R 2500 R 5 260 R15 300 Raw material is added at the 60% stage of completion in Process 2. Normal losses are determined at the 40% completion stage of the process. These losses are calculated at 10% of the number of units reaching the inspection point. Any abnormal losses or gains are identified at this point. Units rejected and removed from the assembly line at the 40% stage of completion have no scrap value. Closing work-in-progress at 31 March 2011 was 1 200 units, averaging 30% complete. A total of 10 000 units was completed and transferred to Process 3 during the month. ● Statement of equivalent units ● Production cost statement ● Process account. 1. Prepare, using the weighted average method of allocation, the following for the period ended 31 March 2011:

Process Costing

Process costing is a sort of operation costing which is employed to determine the value of a product at each process or stage of producing process, applicable where goods produced from a series of continuous operations or procedure.

Job Costing

Job costing is adhesive costs of each and every job involved in the production processes. It is an accounting measure. It is a method which determines the cost of specific jobs, which are performed according to the consumer’s specifications. Job costing is possible only in businesses where the production is done as per the customer’s requirement. For example, some customers order to manufacture furniture as per their needs.

ABC Costing

Cost Accounting is a form of managerial accounting that helps the company in assessing the total variable cost so as to compute the cost of production. Cost accounting is generally used by the management so as to ensure better decision-making. In comparison to financial accounting, cost accounting has to follow a set standard ad can be used flexibly by the management as per their needs. The types of Cost Accounting include – Lean Accounting, Standard Costing, Marginal Costing and Activity Based Costing.

Step by step

Solved in 2 steps with 4 images