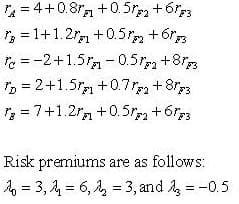

Questions a. - c. refer to the following data. You estimate a 3-factor return-generating process for 5 large portfolios with the following results.

Questions a. - c. refer to the following data. You estimate a 3-factor return-generating process for 5 large portfolios with the following results.

Algebra & Trigonometry with Analytic Geometry

13th Edition

ISBN:9781133382119

Author:Swokowski

Publisher:Swokowski

Chapter1: Fundamental Concepts Of Algebra

Section1.4: Fractional Expressions

Problem 65E

Related questions

Question

Questions a. - c. refer to the following data. You estimate a 3-factor return-generating process for 5 large portfolios with the following results.

a. Which two portfolios are

b. What is the expected return on portfolio B?

c. Suppose that the market is currently pricing portfolio E so that its expected return is 8% and pricing portfolio B so that its expected return is 10%. Describe the forces that will bring about equilibrium according to the APT.

Transcribed Image Text:= 4+0.8r, +0.5r +6rp3

, =1+1.2r +0.5r, +6r3

r = -2+1.5r-0.5r, +8r

D = 2+1.5rm +0.7r +8r3

, = 7+1.2r, +0.5r, +6rp3

F1

%3D

Risk premiums are as follows:

1 = 3, 4 = 6, , = 3, and , = -0.5

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Recommended textbooks for you

Algebra & Trigonometry with Analytic Geometry

Algebra

ISBN:

9781133382119

Author:

Swokowski

Publisher:

Cengage

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Algebra & Trigonometry with Analytic Geometry

Algebra

ISBN:

9781133382119

Author:

Swokowski

Publisher:

Cengage

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill