Refer Chapter 10, section 10-4d, MACRS Conventions. (Concepts in Federal Taxation, 2021th Edition, Murphy, Higgins, Skalberg) Briefly explain – which MACRS convention is generally applicable to PP&E (equipment), and what other two MACRS conventions there are and exactly when or under what circumstances they would be mandatory.

Refer Chapter 10, section 10-4d, MACRS Conventions. (Concepts in Federal Taxation, 2021th Edition, Murphy, Higgins, Skalberg) Briefly explain – which MACRS convention is generally applicable to PP&E (equipment), and what other two MACRS conventions there are and exactly when or under what circumstances they would be mandatory.

Practical Management Science

6th Edition

ISBN:9781337406659

Author:WINSTON, Wayne L.

Publisher:WINSTON, Wayne L.

Chapter8: Evolutionary Solver: An Alternative Optimization Procedure

Section8.6: Fitting An S-shaped Curve

Problem 11P

Related questions

Question

Refer Chapter 10, section 10-4d, MACRS Conventions. (Concepts in Federal

Briefly explain –

- which MACRS convention is generally applicable to PP&E (equipment), and

- what other two MACRS conventions there are and exactly when or under what circumstances they would be mandatory.

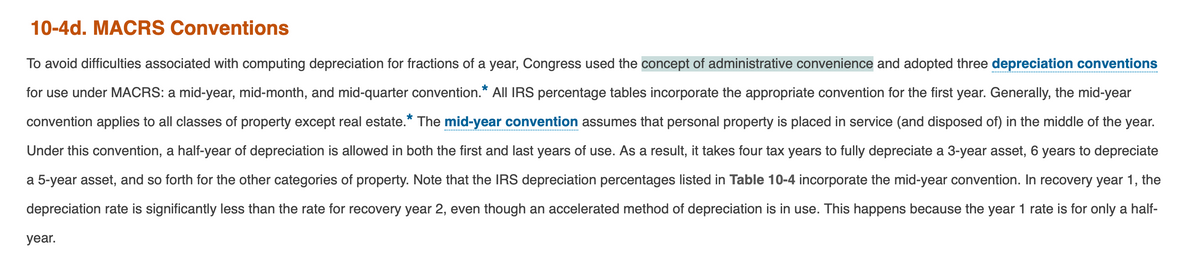

Transcribed Image Text:10-4d. MACRS Conventions

To avoid difficulties associated with computing depreciation for fractions of a year, Congress used the concept of administrative convenience and adopted three depreciation conventions

for use under MACRS: a mid-year, mid-month, and mid-quarter convention.* All| IRS percentage tables incorporate the appropriate convention for the first year. Generally, the mid-year

convention applies to all classes of property except real estate.* The mid-year convention assumes that personal property is placed in service (and disposed of) in the middle of the year.

Under this convention, a half-year of depreciation is allowed in both the first and last years of use. As a result, it takes four tax years to fully depreciate a 3-year asset, 6 years to depreciate

a 5-year asset, and so forth for the other categories of property. Note that the IRS depreciation percentages listed in Table 10-4 incorporate the mid-year convention. In recovery year 1, the

depreciation rate is significantly less than the rate for recovery year 2, even though an accelerated method of depreciation is in use. This happens because the year 1 rate is for only a half-

year.

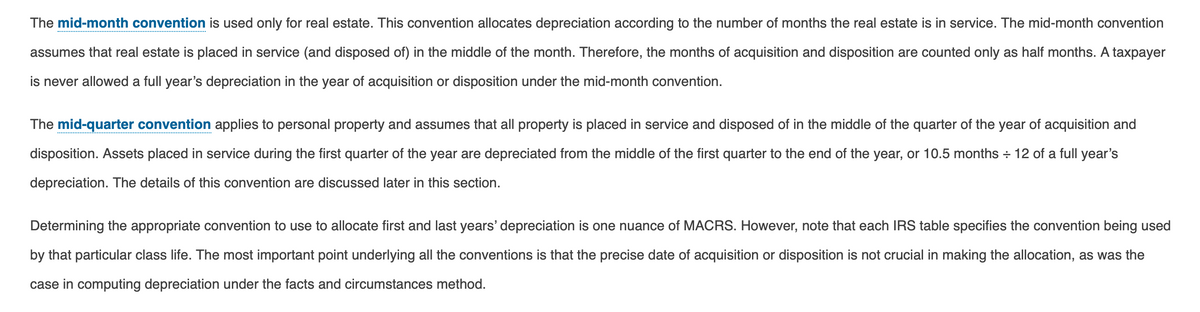

Transcribed Image Text:The mid-month convention is used only for real estate. This convention allocates depreciation according to the number of months the real estate is in service. The mid-month convention

assumes that real estate is placed in service (and disposed of) in the middle of the month. Therefore, the months of acquisition and disposition are counted only as half months. A taxpayer

is never allowed a full year's depreciation in the year of acquisition or disposition under the mid-month convention.

The mid-quarter convention applies to personal property and assumes that all property is placed in service and disposed of in the middle of the quarter of the year of acquisition and

disposition. Assets placed in service during the first quarter of the year are depreciated from the middle of the first quarter to the end of the year, or 10.5 months + 12 of a full year's

depreciation. The details of this convention are discussed later in this section.

Determining the appropriate convention to use to allocate first and last years' depreciation is one nuance of MACRS. However, note that each IRS table specifies the convention being used

by that particular class life. The most important point underlying all the conventions is that the precise date of acquisition or disposition is not crucial in making the allocation, as was the

case in computing depreciation under the facts and circumstances method.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, operations-management and related others by exploring similar questions and additional content below.Recommended textbooks for you

Practical Management Science

Operations Management

ISBN:

9781337406659

Author:

WINSTON, Wayne L.

Publisher:

Cengage,

Practical Management Science

Operations Management

ISBN:

9781337406659

Author:

WINSTON, Wayne L.

Publisher:

Cengage,