Refer to the diagram, in which S is the market supply curve and S, is a supply curve comprising all costs of production, including external costs. Assume that the number of people affected by these external costs is large. If the government wishes to establish an optimal allocation of resources in this market, it should

Refer to the diagram, in which S is the market supply curve and S, is a supply curve comprising all costs of production, including external costs. Assume that the number of people affected by these external costs is large. If the government wishes to establish an optimal allocation of resources in this market, it should

Economics: Private and Public Choice (MindTap Course List)

16th Edition

ISBN:9781305506725

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Chapter5: Difficult Cases For The Market And The Role Of Government

Section: Chapter Questions

Problem 10CQ

Related questions

Question

100%

Transcribed Image Text:6:14 1

.ul LTE O

I moodle.ku.edu.kw

P Flag question

S

Quantity

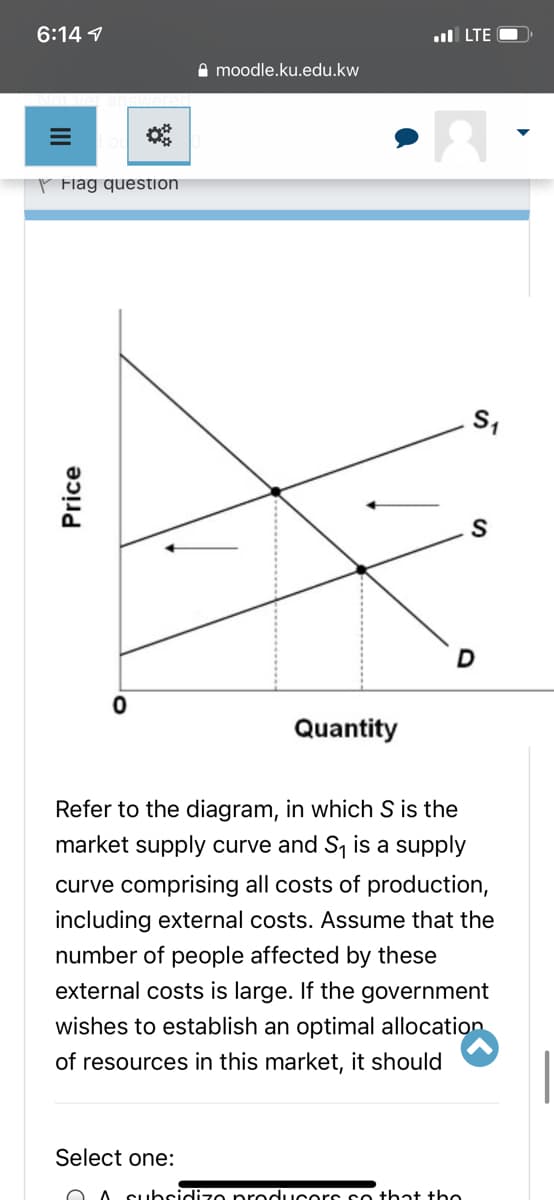

Refer to the diagram, in which S is the

market supply curve and S is a supply

curve comprising all costs of production,

including external costs. Assume that the

number of people affected by these

external costs is large. If the government

wishes to establish an optimal allocation

of resources in this market, it should

Select one:

O A SUbsidizo producors so that the

Price

II

Transcribed Image Text:6:14 1

ul LTE O

I moodle.ku.edu.kw

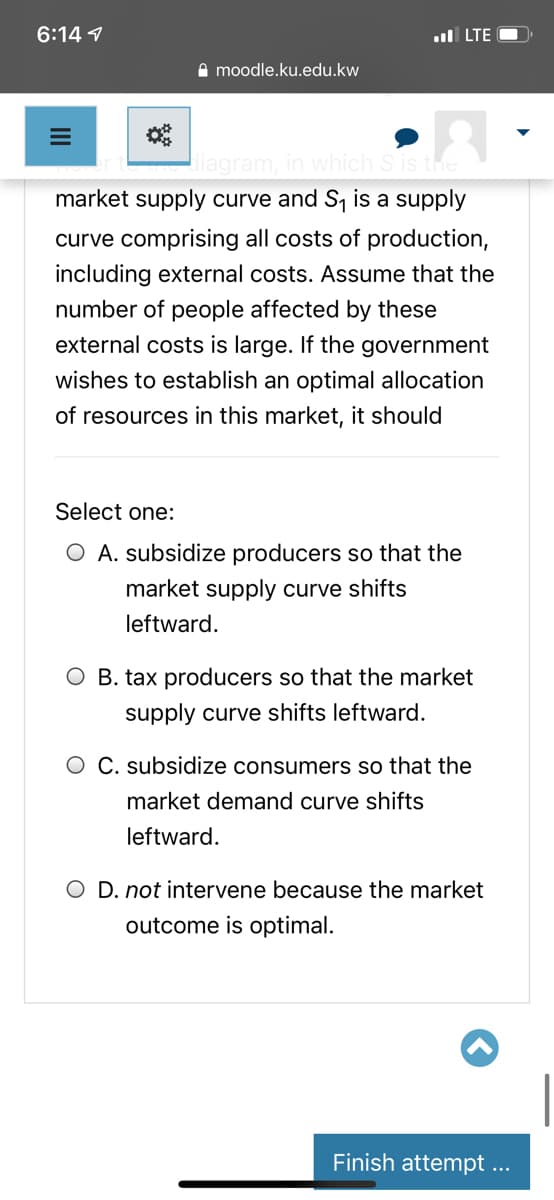

iagram, in which S is

market supply curve and S, is a supply

curve comprising all costs of production,

including external costs. Assume that the

number of people affected by these

external costs is large. If the government

wishes to establish an optimal allocation

of resources in this market, it should

Select one:

O A. subsidize producers so that the

market supply curve shifts

leftward.

O B. tax producers so that the market

supply curve shifts leftward.

O C. subsidize consumers so that the

market demand curve shifts

leftward.

O D. not intervene because the market

outcome is optimal.

Finish attempt ...

II

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Macroeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506756

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Macroeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506756

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax