Required: 1. Prepare journal entry to set up the allowance for doubtful accounts on January 1, 2020. 2. Compute the doubtful accounts expense for the current year, 3. Determine the net realizable value of accounts receivable on December 31, 2020.

Required: 1. Prepare journal entry to set up the allowance for doubtful accounts on January 1, 2020. 2. Compute the doubtful accounts expense for the current year, 3. Determine the net realizable value of accounts receivable on December 31, 2020.

Auditing: A Risk Based-Approach to Conducting a Quality Audit

10th Edition

ISBN:9781305080577

Author:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Chapter16: Advanced Topics Concerning Complex Auditing Judgments

Section: Chapter Questions

Problem 36RSCQ

Related questions

Question

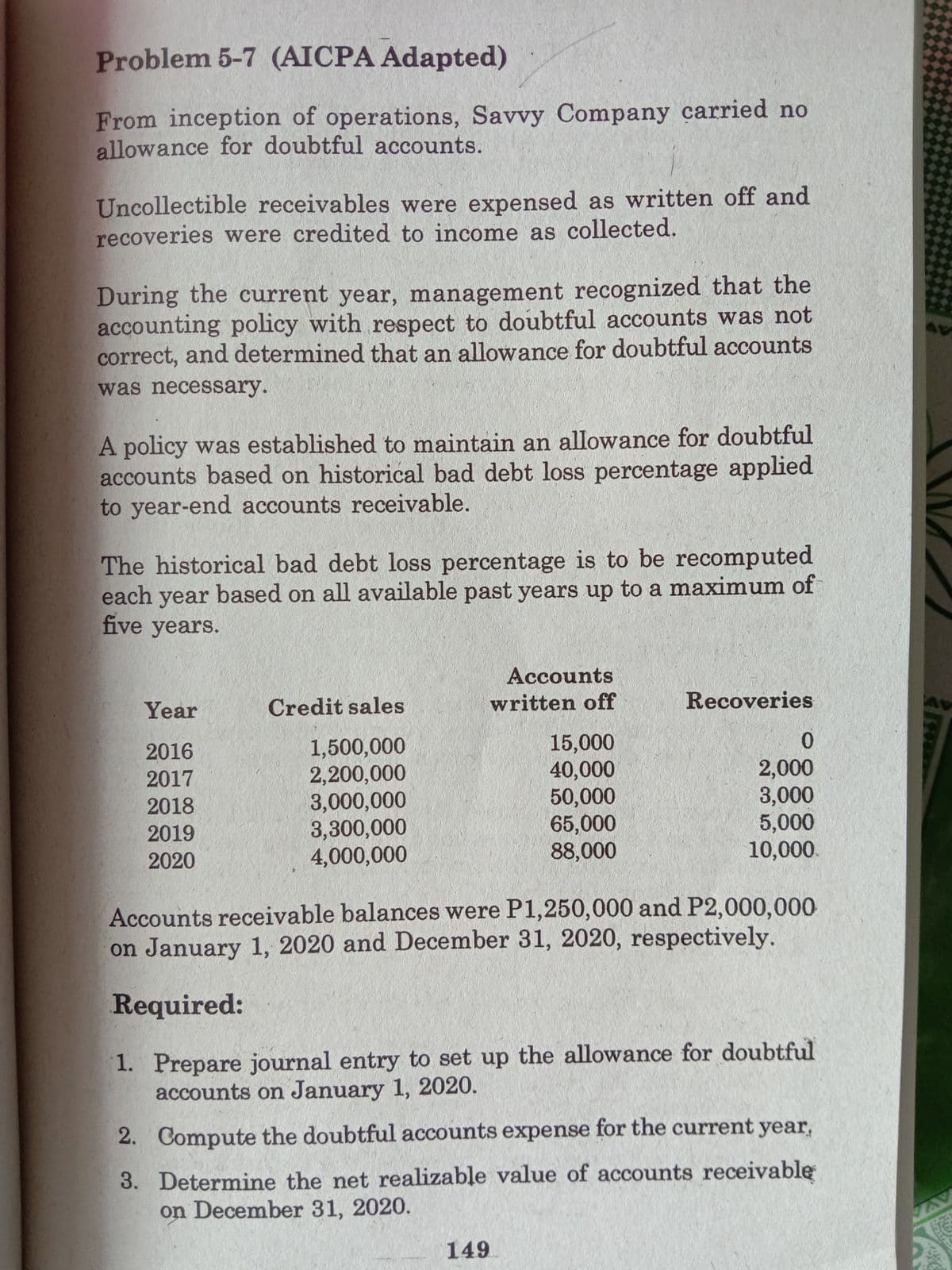

Transcribed Image Text:Problem 5-7 (AICPA Adapted)

From inception of operations, Savvy Company carried no

allowance for doubtful accounts.

Uncollectible receivables were expensed as written off and

recoveries were credited to income as collected.

During the current year, management recognized that the

accounting policy with respect to doubtful accounts was not

correct, and determined that an allowance for doubtful accounts

was necessary.

A policy was established to maintain an allowance for doubtful

accounts based on historical bad debt loss percentage applied

to year-end accounts receivable.

The historical bad debt loss percentage is to be recomputed

each year based on all available past years up to a maximum of

five years.

Accounts

written off

Year

Credit sales

Recoveries

1,500,000

2,200,000

3,000,000

3,300,000

4,000,000

2016

15,000

40,000

50,000

65,000

88,000

2017

2,000

3,000

5,000

10,000

2018

2019

2020

Accounts receivable balances were P1,250,000 and P2,000,000

on January 1, 2020 and December 31, 2020, respectively.

Required:

1. Prepare journal entry to set up the allowance for doubtful

accounts on January 1, 2020.

2. Compute the doubtful accounts expense for the current year,

3. Determine the net realizable value of accounts receivable

on December 31, 2020.

AV

149

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub