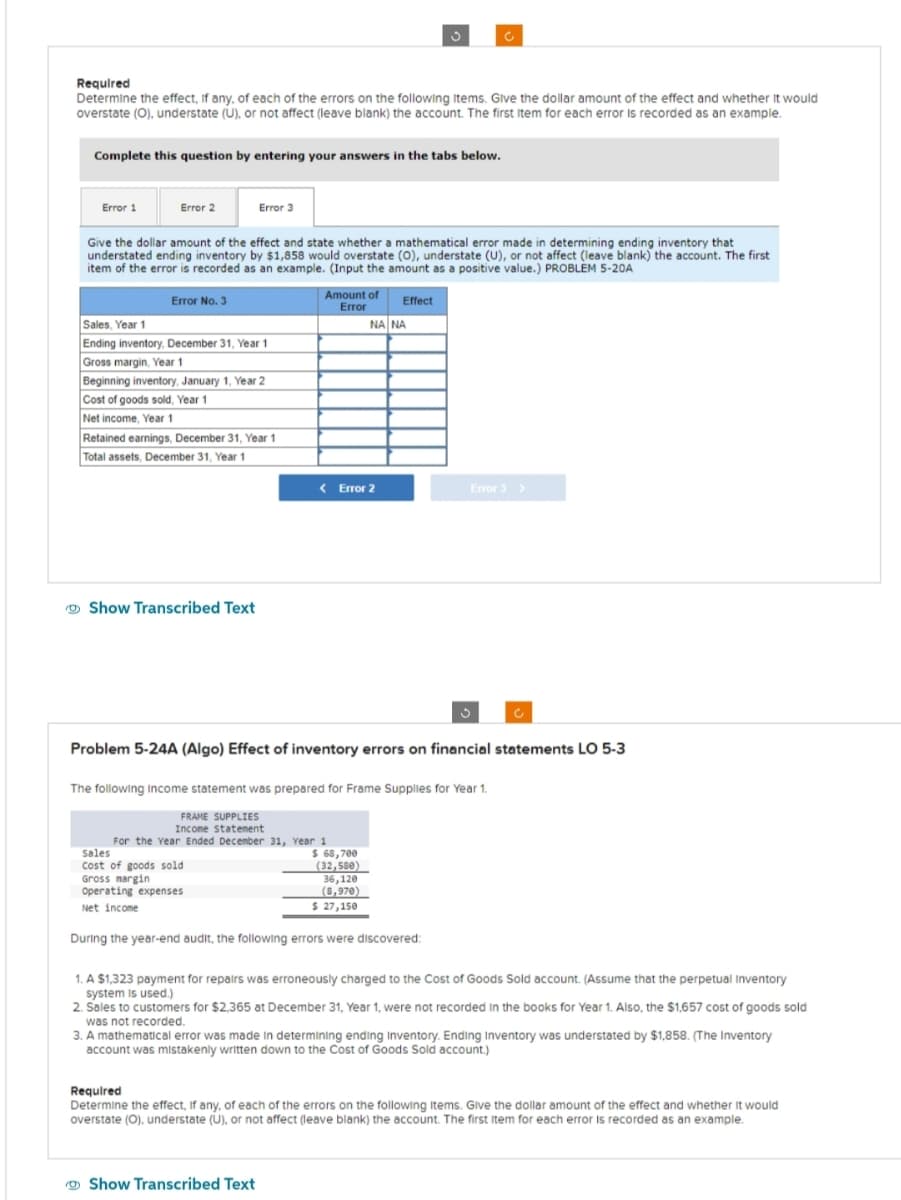

Required Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would overstate (O), understate (U), or not affect (leave blank) the account. The first item for each error is recorded as an example. Complete this question by entering your answers in the tabs below. Error 1 Error 2 Error 3 Give the dollar amount of the effect and state whether a mathematical error made in determining ending inventory that understated ending inventory by $1,858 would overstate (O), understate (U), or not affect (leave blank) the account. The first item of the error is recorded as an example. (Input the amount as a positive value.) PROBLEM 5-20A

Required Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would overstate (O), understate (U), or not affect (leave blank) the account. The first item for each error is recorded as an example. Complete this question by entering your answers in the tabs below. Error 1 Error 2 Error 3 Give the dollar amount of the effect and state whether a mathematical error made in determining ending inventory that understated ending inventory by $1,858 would overstate (O), understate (U), or not affect (leave blank) the account. The first item of the error is recorded as an example. (Input the amount as a positive value.) PROBLEM 5-20A

College Accounting, Chapters 1-27

23rd Edition

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:HEINTZ, James A.

Chapter4: Journalizing And Posting Transactions

Section: Chapter Questions

Problem 8SEA: FINDING AND CORRECTING ERRORS On May 25, after the transactions had been posted, Joe Adams...

Related questions

Question

Please Solve all Requirement With details and Do not give solution in images format

Transcribed Image Text:Required

Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would

overstate (O), understate (U), or not affect (leave blank) the account. The first Item for each error is recorded as an example.

Complete this question by entering your answers in the tabs below.

Error 1

Error 2

Give the dollar amount of the effect and state whether a mathematical error made in determining ending inventory that

understated ending inventory by $1,858 would overstate (O), understate (U), or not affect (leave blank) the account. The first

item of the error is recorded as an example. (Input the amount as a positive value.) PROBLEM 5-20A

Error No. 3

Error 3

Sales, Year 1

Ending inventory, December 31, Year 1

Gross margin, Year 1

Beginning inventory, January 1, Year 2

Cost of goods sold, Year 1

Net income, Year 1

Retained earnings, December 31, Year 1

Total assets, December 31, Year 1

Show Transcribed Text

Amount of

Error

<Error 2

ΝΑΙ ΝΑ

FRAME SUPPLIES

Income statement

For the Year Ended December 31, Year 1

Problem 5-24A (Algo) Effect of inventory errors on financial statements LO 5-3

Effect

The following income statement was prepared for Frame Supplies for Year 1.

$ 68,700

(32,580)

36,120

(8,970)

$ 27,150

Show Transcribed Text

Error 3 >

Sales

Cost of goods sold

Gross margin

Operating expenses

Net income

During the year-end audit, the following errors were discovered:

1. A $1,323 payment for repairs was erroneously charged to the Cost of Goods Sold account. (Assume that the perpetual Inventory

system is used.)

2. Sales to customers for $2,365 at December 31, Year 1, were not recorded in the books for Year 1. Also, the $1,657 cost of goods sold

was not recorded.

3. A mathematical error was made in determining ending Inventory. Ending Inventory was understated by $1,858. (The Inventory

account was mistakenly written down to the Cost of Goods Sold account.)

Required

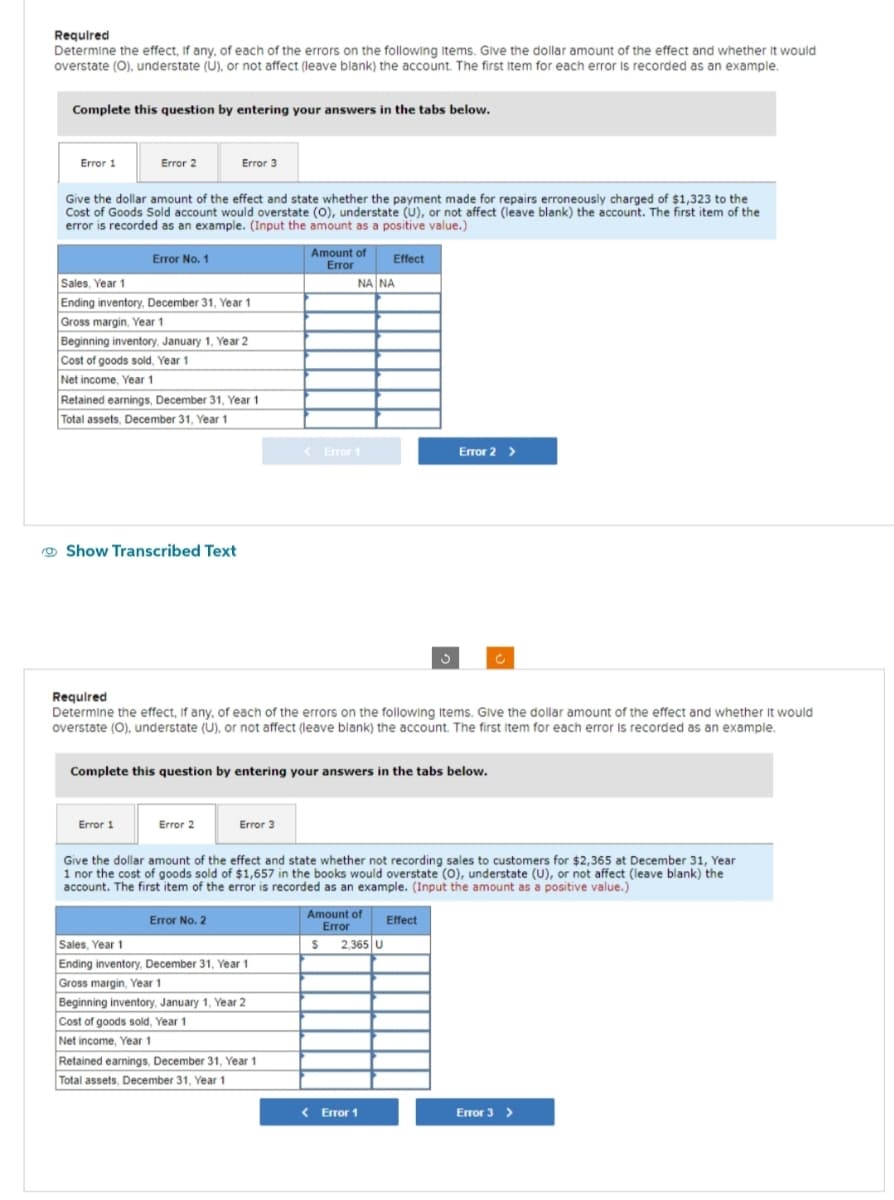

Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would

overstate (O), understate (U), or not affect (leave blank) the account. The first item for each error is recorded as an example.

Transcribed Image Text:Required

Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would

overstate (O), understate (U), or not affect (leave blank) the account. The first Item for each error is recorded as an example.

Complete this question by entering your answers in the tabs below.

Error 1

Error 2

Give the dollar amount of the effect and state whether the payment made for repairs erroneously charged of $1,323 to the

Cost of Goods Sold account would overstate (O), understate (U), or not affect (leave blank) the account. The first item of the

error is recorded as an example. (Input the amount as a positive value.)

Error No. 1

Sales, Year 1

Ending inventory, December 31, Year 1

Gross margin, Year 1

Beginning inventory, January 1, Year 2

Cost of goods sold, Year 1

Net income, Year 1

Retained earnings, December 31, Year 1

Total assets, December 31, Year 1

Show Transcribed Text

Error 3

Error 1

Error 2

Error No. 2

Error 3

Amount of

Error

Required

Determine the effect, if any, of each of the errors on the following items. Give the dollar amount of the effect and whether it would

overstate (O), understate (U), or not affect (leave blank) the account. The first item for each error is recorded as an example.

Complete this question by entering your answers in the tabs below.

Sales, Year 1

Ending inventory, December 31, Year 1

Gross margin, Year 1

Beginning inventory, January 1, Year 2

Cost of goods sold, Year 1

Net income, Year 1

<Error 1

Retained earnings, December 31, Year 1

Total assets, December 31, Year 1

NA NA

Effect

Give the dollar amount of the effect and state whether not recording sales to customers for $2,365 at December 31, Year

1 nor the cost of goods sold of $1,657 in the books would overstate (O), understate (U), or not affect (leave blank) the

account. The first item of the error is recorded as an example. (Input the amount as a positive value.)

Amount of

Error

$ 2,365 U

<Error 1

S

Error 2 >

Effect

Error 3 >

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning