s the chief investment officer for a money management firm specializing in taxable individual investors, you are trying to establish a strategic asset allocation for two different clients. You have established that Ms. A has a risk-tolerance factor of 8, while Mr. B has a risk-tolerance factor of 26. The characteristics for four model portfolios follow: ASSET MIX Bond 91% 80 2 39 3 4 14 a. Calculate the expected utility of each prospective portfolio for each of the two clients. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio 1 2 3 Portfolio 1 Stock 9% 20 61 86 Ms. A ER 8% 9 10 11 02 6% 12 15 24 Mr. B b. Which portfolio represents the optimal strategic allocation for Ms. A? Which portfolio is optimal for Mr. B? Portfolio -Select-represents the optimal strategic allocation for Ms. A. Portfolio -Select- is the optimal allocation for Mr. B. c. For Ms. A, what level of risk tolerance would leave her indifferent between having Portfolio 1 or Portfolio 2 as her strategic allocation? Round your answer to the nearest whole number.

s the chief investment officer for a money management firm specializing in taxable individual investors, you are trying to establish a strategic asset allocation for two different clients. You have established that Ms. A has a risk-tolerance factor of 8, while Mr. B has a risk-tolerance factor of 26. The characteristics for four model portfolios follow: ASSET MIX Bond 91% 80 2 39 3 4 14 a. Calculate the expected utility of each prospective portfolio for each of the two clients. Do not round intermediate calculations. Round your answers to two decimal places. Portfolio 1 2 3 Portfolio 1 Stock 9% 20 61 86 Ms. A ER 8% 9 10 11 02 6% 12 15 24 Mr. B b. Which portfolio represents the optimal strategic allocation for Ms. A? Which portfolio is optimal for Mr. B? Portfolio -Select-represents the optimal strategic allocation for Ms. A. Portfolio -Select- is the optimal allocation for Mr. B. c. For Ms. A, what level of risk tolerance would leave her indifferent between having Portfolio 1 or Portfolio 2 as her strategic allocation? Round your answer to the nearest whole number.

Chapter10: Project Cash Flows And Risk

Section: Chapter Questions

Problem 20PROB

Related questions

Question

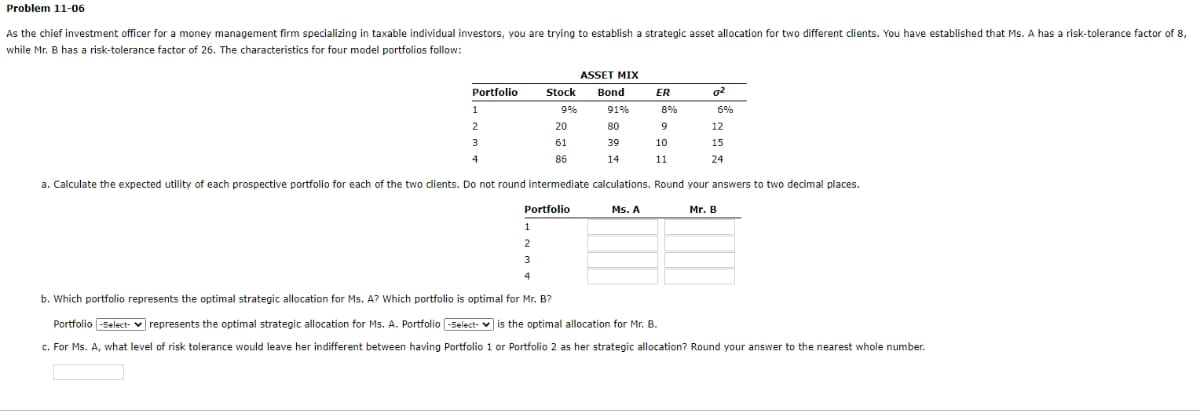

Transcribed Image Text:Problem 11-06

As the chief investment officer for a money management firm specializing in taxable individual investors, you are trying to establish a strategic asset allocation for two different clients. You have established that Ms. A has a risk-tolerance factor of 8,

while Mr. B has a risk-tolerance factor of 26. The characteristics for four model portfolios follow:

ASSET MIX

Bond

91%

8%

80

9

39

10

3

4

14

11

a. Calculate the expected utility of each prospective portfolio for each of the two clients. Do not round intermediate calculations. Round your answers to two decimal places.

Mr. B

Portfolio

1

2

Portfolio

1

Stock

9%

20

61

86

2

3

4

b. Which portfolio represents the optimal strategic allocation for Ms. A? Which portfolio is optimal for Mr. B?

Ms. A

ER

02

6%

12

15

24

Portfolio -Select-represents the optimal strategic allocation for Ms. A. Portfolio -Select- is the optimal allocation for Mr. B.

c. For Ms. A, what level of risk tolerance would leave her indifferent between having Portfolio 1 or Portfolio 2 as her strategic allocation? Round your answer to the nearest whole number.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781337395250

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781337395250

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781285867977

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning