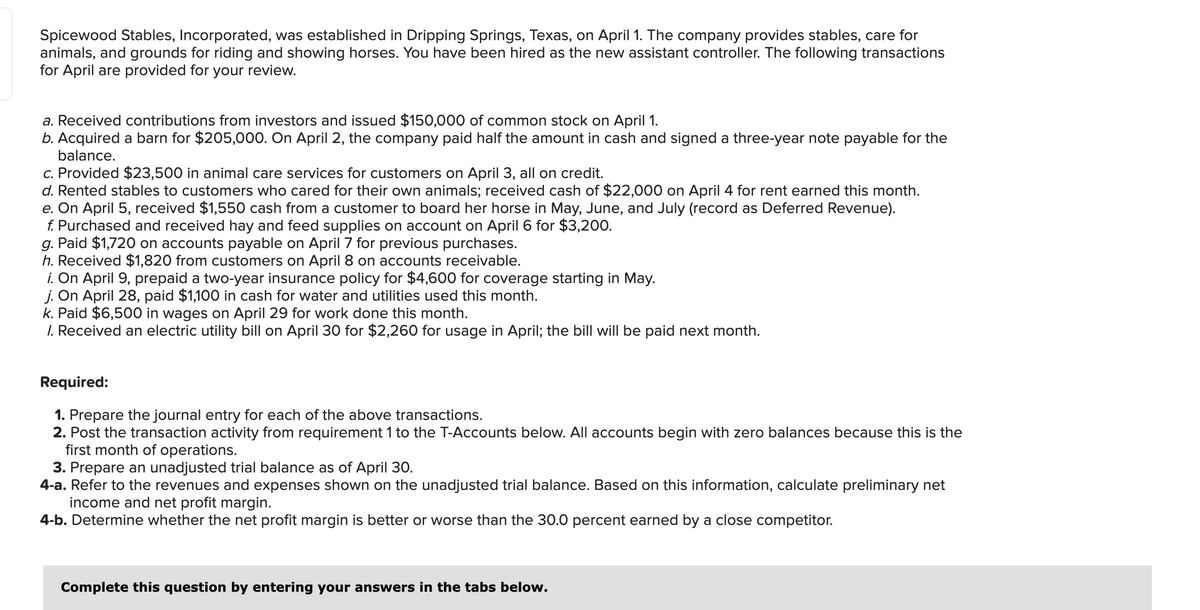

Spicewood Stables, Incorporated, was established in Dripping Springs, Texas, on April 1. The company provides stables, care for animals, and grounds for riding and showing horses. You have been hired as the new assistant controller. The following transactions for April are provided for your review. a. Received contributions from investors and issued $150,000 of common stock on April 1. b. Acquired a barn for $205,000. On April 2, the company paid half the amount in cash and signed a three-year note payable for the balance. c. Provided $23,500 in animal care services for customers on April 3, all on credit. d. Rented stables to customers who cared for their own animals; received cash of $22,000 on April 4 for rent earned this month. e. On April 5, received $1,550 cash from a customer to board her horse in May, June, and July (record as Deferred Revenue). f. Purchased and received hay and feed supplies on account on April 6 for $3,200. g. Paid $1,720 on accounts payable on April 7 for previous purchases. h. Received $1,820 from customers on April 8 on accounts receivable. i. On April 9, prepaid a two-year insurance policy for $4,600 for coverage starting in May. j. On April 28, paid $1,100 in cash for water and utilities used this month. k. Paid $6,500 in wages on April 29 for work done this month. I. Received an electric utility bill on April 30 for $2,260 for usage in April; the bill will be paid next month.

Spicewood Stables, Incorporated, was established in Dripping Springs, Texas, on April 1. The company provides stables, care for animals, and grounds for riding and showing horses. You have been hired as the new assistant controller. The following transactions for April are provided for your review. a. Received contributions from investors and issued $150,000 of common stock on April 1. b. Acquired a barn for $205,000. On April 2, the company paid half the amount in cash and signed a three-year note payable for the balance. c. Provided $23,500 in animal care services for customers on April 3, all on credit. d. Rented stables to customers who cared for their own animals; received cash of $22,000 on April 4 for rent earned this month. e. On April 5, received $1,550 cash from a customer to board her horse in May, June, and July (record as Deferred Revenue). f. Purchased and received hay and feed supplies on account on April 6 for $3,200. g. Paid $1,720 on accounts payable on April 7 for previous purchases. h. Received $1,820 from customers on April 8 on accounts receivable. i. On April 9, prepaid a two-year insurance policy for $4,600 for coverage starting in May. j. On April 28, paid $1,100 in cash for water and utilities used this month. k. Paid $6,500 in wages on April 29 for work done this month. I. Received an electric utility bill on April 30 for $2,260 for usage in April; the bill will be paid next month.

Financial Accounting: The Impact on Decision Makers

10th Edition

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Gary A. Porter, Curtis L. Norton

Chapter9: Current Liabilities, Contingencies, And The Time Value Of Money

Section: Chapter Questions

Problem 9.10E

Related questions

Question

Transcribed Image Text:Spicewood Stables, Incorporated, was established in Dripping Springs, Texas, on April 1. The company provides stables, care for

animals, and grounds for riding and showing horses. You have been hired as the new assistant controller. The following transactions

for April are provided for your review.

a. Received contributions from investors and issued $150,000 of common stock on April 1.

b. Acquired a barn for $205,000. On April 2, the company paid half the amount in cash and signed a three-year note payable for the

balance.

c. Provided $23,500 in animal care services for customers on April 3, all on credit.

d. Rented stables to customers who cared for their own animals; received cash of $22,000 on April 4 for rent earned this month.

e. On April 5, received $1,550 cash from a customer to board her horse in May, June, and July (record as Deferred Revenue).

f. Purchased and received hay and feed supplies on account on April 6 for $3,200.

g. Paid $1,720 on accounts payable on April 7 for previous purchases.

h. Received $1,820 from customers on April 8 on accounts receivable.

i. On April 9, prepaid a two-year insurance policy for $4,600 for coverage starting in May.

j. On April 28, paid $1,100 in cash for water and utilities used this month.

k. Paid $6,500 in wages on April 29 for work done this month.

I. Received an electric utility bill on April 30 for $2,260 for usage in April; the bill will be paid next month.

Required:

1. Prepare the journal entry for each of the above transactions.

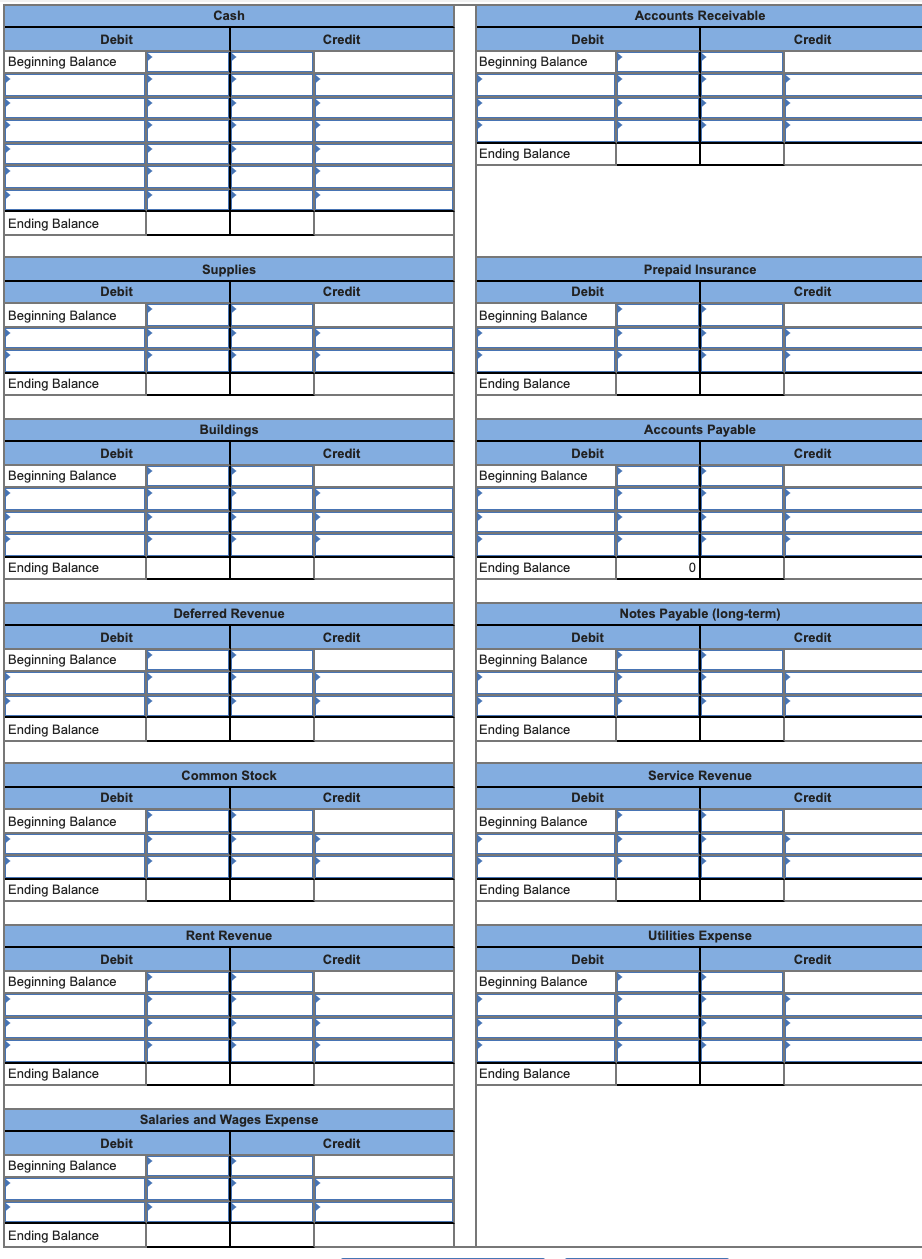

2. Post the transaction activity from requirement 1 to the T-Accounts below. All accounts begin with zero balances because this is the

first month of operations.

3. Prepare an unadjusted trial balance as of April 30.

4-a. Refer to the revenues and expenses shown on the unadjusted trial balance. Based on this information, calculate preliminary net

income and net profit margin.

4-b. Determine whether the net profit margin is better or worse than the 30.0 percent earned by a close competitor.

Complete this question by entering your answers in the tabs below.

Transcribed Image Text:Cash

Accounts Receivable

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Supplies

Prepaid Insurance

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Buildings

Accounts Payable

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Deferred Revenue

Notes Payable (long-term)

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Common Stock

Service Revenue

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Rent Revenue

Utilities Expense

Debit

Credit

Debit

Credit

Beginning Balance

Beginning Balance

Ending Balance

Ending Balance

Salaries and Wages Expense

Debit

Credit

Beginning Balance

Ending Balance

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781305084087

Author:

Cathy J. Scott

Publisher:

Cengage Learning