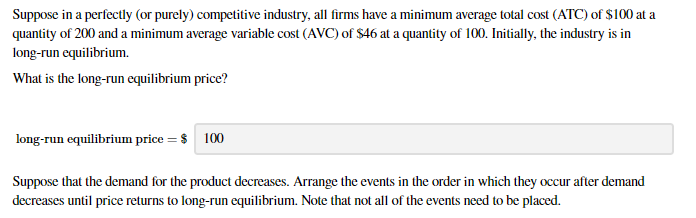

Suppose in a perfectly (or purely) competitive industry, all firms have a minimum average total cost (ATC) of $100 at a quantity of 200 and a minimum average variable cost (AVC) of $46 at a quantity of 100. Initially, the industry is in long-run equilibrium. What is the long-run equilibrium price? long-run equilibrium price = $ 100 Suppose that the demand for the product decreases. Arrange the events in the order in which they occur after demand decreases until price returns to long-run equilibrium. Note that not all of the events need to be placed. After demand decreases price increases supply increases price decreases firms exit supply decreases firms enter Until the market returns to long-run equilibrium price Answer Bank

Suppose in a perfectly (or purely) competitive industry, all firms have a minimum average total cost (ATC) of $100 at a quantity of 200 and a minimum average variable cost (AVC) of $46 at a quantity of 100. Initially, the industry is in long-run equilibrium. What is the long-run equilibrium price? long-run equilibrium price = $ 100 Suppose that the demand for the product decreases. Arrange the events in the order in which they occur after demand decreases until price returns to long-run equilibrium. Note that not all of the events need to be placed. After demand decreases price increases supply increases price decreases firms exit supply decreases firms enter Until the market returns to long-run equilibrium price Answer Bank

Chapter12: The Partial Equilibrium Competitive Model

Section: Chapter Questions

Problem 12.9P

Related questions

Question

Transcribed Image Text:Suppose in a perfectly (or purely) competitive industry, all firms have a minimum average total cost (ATC) of $100 at a

quantity of 200 and a minimum average variable cost (AVC) of $46 at a quantity of 100. Initially, the industry is in

long-run equilibrium.

What is the long-run equilibrium price?

long-run equilibrium price = $

100

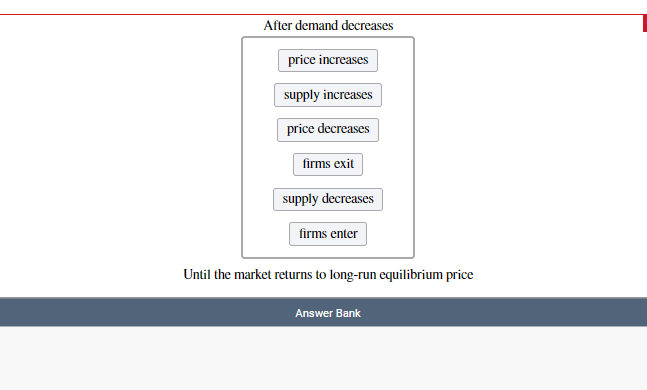

Suppose that the demand for the product decreases. Arrange the events in the order in which they occur after demand

decreases until price returns to long-run equilibrium. Note that not all of the events need to be placed.

Transcribed Image Text:After demand decreases

price increases

supply increases

price decreases

firms exit

supply decreases

firms enter

Until the market returns to long-run equilibrium price

Answer Bank

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 1 images

Recommended textbooks for you