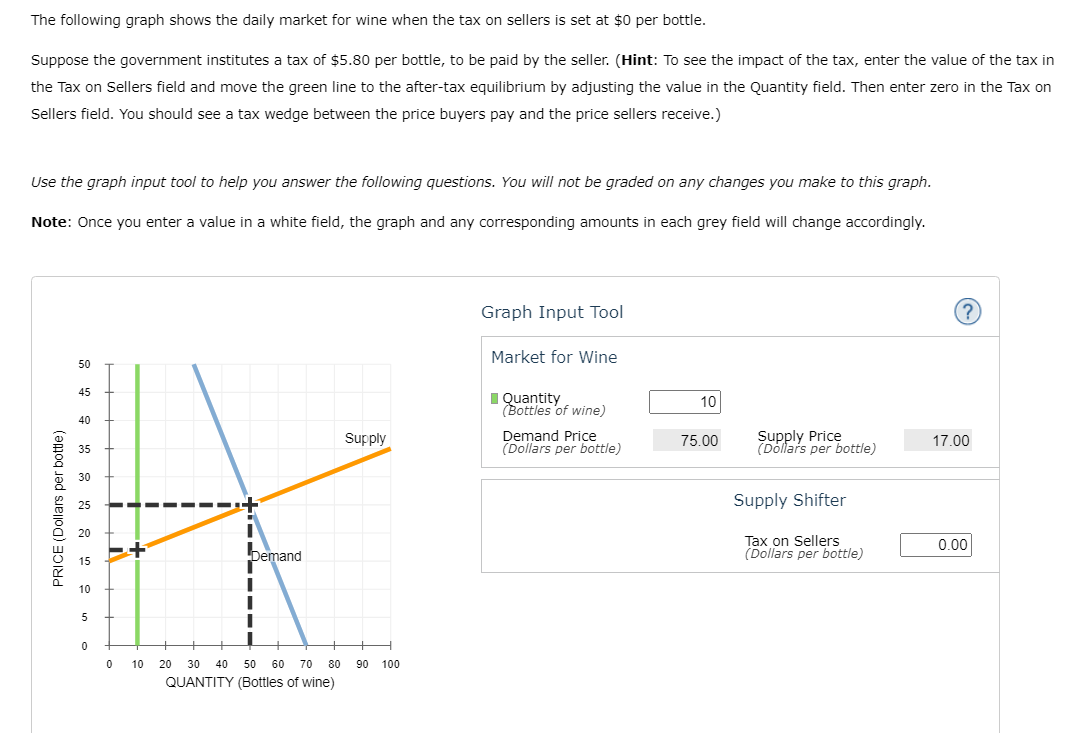

The following graph shows the daily market for wine when the tax on sellers is set at $0 per bottle. Suppose the government institutes a tax of $5.80 per bottle, to be paid by the seller. (Hint: To see the impact of the tax, enter the value of the tax in the Tax on Sellers field and move the green line to the after-tax equilibrium by adjusting the value in the Quantity field. Then enter zero in the Tax on Sellers field. You should see a tax wedge between the price buyers pay and the price sellers receive.) Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. 50 45 40 Graph Input Tool Market for Wine Quantity (Bottles of wine) 10

The following graph shows the daily market for wine when the tax on sellers is set at $0 per bottle. Suppose the government institutes a tax of $5.80 per bottle, to be paid by the seller. (Hint: To see the impact of the tax, enter the value of the tax in the Tax on Sellers field and move the green line to the after-tax equilibrium by adjusting the value in the Quantity field. Then enter zero in the Tax on Sellers field. You should see a tax wedge between the price buyers pay and the price sellers receive.) Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. 50 45 40 Graph Input Tool Market for Wine Quantity (Bottles of wine) 10

Principles of Microeconomics (MindTap Course List)

8th Edition

ISBN:9781305971493

Author:N. Gregory Mankiw

Publisher:N. Gregory Mankiw

Chapter8: Application: The Cost Of Taxation

Section: Chapter Questions

Problem 10PA

Related questions

Question

Transcribed Image Text:The following graph shows the daily market for wine when the tax on sellers is set at $0 per bottle.

Suppose the government institutes a tax of $5.80 per bottle, to be paid by the seller. (Hint: To see the impact of the tax, enter the value of the tax in

the Tax on Sellers field and move the green line to the after-tax equilibrium by adjusting the value in the Quantity field. Then enter zero in the Tax on

Sellers field. You should see a tax wedge between the price buyers pay and the price sellers receive.)

Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph.

Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly.

PRICE (Dollars per bottle)

50

45

40

35

5

0

0

10

Demand

80

20 30 40 50 60 70

QUANTITY (Bottles of wine)

Supply

90 100

Graph Input Tool

Market for Wine

Quantity

(Bottles of wine)

Demand Price

(Dollars per bottle)

10

75.00

Supply Price

(Dollars per bottle)

Supply Shifter

Tax on Sellers

(Dollars per bottle)

17.00

0.00

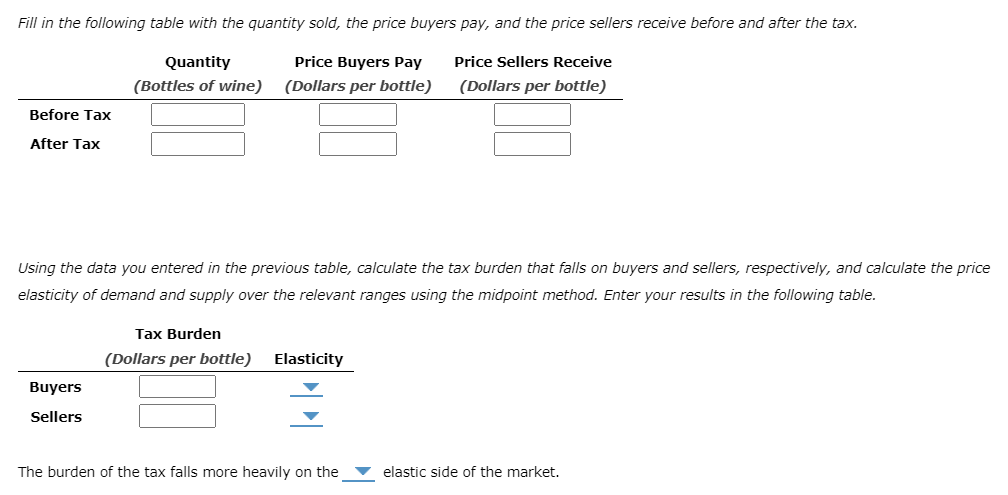

Transcribed Image Text:Fill in the following table with the quantity sold, the price buyers pay, and the price sellers receive before and after the tax.

Quantity

Price Buyers Pay Price Sellers Receive

(Bottles of wine) (Dollars per bottle) (Dollars per bottle)

Before Tax

After Tax

Using the data you entered in the previous table, calculate the tax burden that falls on buyers and sellers, respectively, and calculate the price

elasticity of demand and supply over the relevant ranges using the midpoint method. Enter your results in the following table.

Buyers

Sellers

Tax Burden

(Dollars per bottle) Elasticity

The burden of the tax falls more heavily on the

elastic side of the market.

Expert Solution

Step 1

Demand refers to the amount of a certain good or service that consumers are willing and able to purchase at a given price.

Supply refers to the amount of a certain good or service that producers are willing and able to produce and sell at a given price.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Microeconomics (MindTap Course List)

Economics

ISBN:

9781305971493

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Macroeconomics (MindTap Course List)

Economics

ISBN:

9781285165912

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Microeconomics (MindTap Course List)

Economics

ISBN:

9781305971493

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Macroeconomics (MindTap Course List)

Economics

ISBN:

9781285165912

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Macroeconomics (MindTap Course List)

Economics

ISBN:

9781305971509

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning