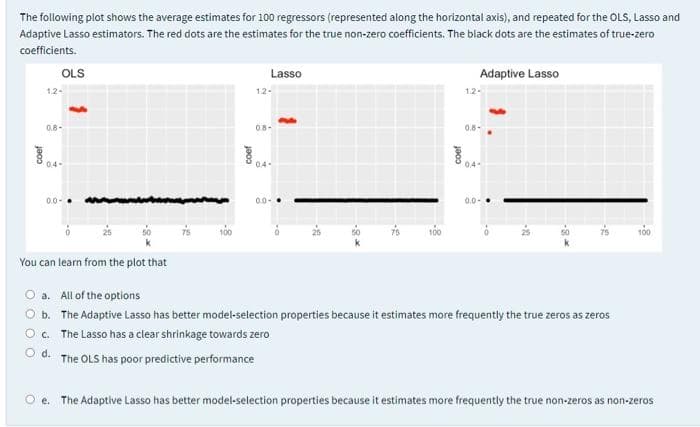

The following plot shows the average estimates for 100 regressors (represented along the horizontal axis), and repeated for the OLS, Lasso and Adaptive Lasso estimators. The red dots are the estimates for the true non-zero coefficients. The black dots are the estimates of true-zero coefficients. OLS Lasso Adaptive Lasso 1.2- 12- 1.2 0.8- 08- 0.8- 04- 04- 04- 0.0-. 0- 0.0-. 100 You can learn from the plot that O a. All of the options O b. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true zeros as zeros O. The Lasso has a clear shrinkage towards zero O d. The OLS has poor predictive performance e. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true non-zeros as non-zeros

The following plot shows the average estimates for 100 regressors (represented along the horizontal axis), and repeated for the OLS, Lasso and Adaptive Lasso estimators. The red dots are the estimates for the true non-zero coefficients. The black dots are the estimates of true-zero coefficients. OLS Lasso Adaptive Lasso 1.2- 12- 1.2 0.8- 08- 0.8- 04- 04- 04- 0.0-. 0- 0.0-. 100 You can learn from the plot that O a. All of the options O b. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true zeros as zeros O. The Lasso has a clear shrinkage towards zero O d. The OLS has poor predictive performance e. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true non-zeros as non-zeros

Linear Algebra: A Modern Introduction

4th Edition

ISBN:9781285463247

Author:David Poole

Publisher:David Poole

Chapter7: Distance And Approximation

Section7.3: Least Squares Approximation

Problem 31EQ

Related questions

Question

6

Transcribed Image Text:The following plot shows the average estimates for 100 regressors (represented along the horizontal axis), and repeated for the OLS, Lasso and

Adaptive Lasso estimators. The red dots are the estimates for the true non-zero coefficients. The black dots are the estimates of true-zero

coefficients.

OLS

Lasso

Adaptive Lasso

12-

12-

1.2-

0.8-

08-

0.8-

04-

04-

04-

00-.

00

0.0-.

100

75

100

100

You can learn from the plot that

a. All of the options

b. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true zeros as zeros

O. The Lasso has a clear shrinkage towards zero

O d. The OLS has poor predictive performance

e. The Adaptive Lasso has better model-selection properties because it estimates more frequently the true non-zeros as non-zeros

-8

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Recommended textbooks for you

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill