This credit account carries a temporary low introductory rate (teaser rate) of| %. This teaser APR applies to purchases made within the first months that the account is open. After this introductory period, the APR for purchases reverts to a higher variable APR. This regular APR for purchases is calculated by adding | remains at 4%, then the regular APR for purchases is ]% to the U.S. prime rate (assumed to be 4% in the disclosure). Therefore, if the U.S. prime rate %. For balance transfers, the introductory (teaser) APR i | higher APR of |%. But after the introductory period, the APR for balance transfers reverts to the | % to the prime rate (assumed to be 4%). %. The regular APR for balance transfers is calculated by adding This account does not have an introductory (teaser) APR for cash advances. For cash advances, the APR is calculated by adding| U.S. prime rate (cited at 4% in the disclosure). Therefore, variable APR for cash advances is at least % to the These introductory and regular rates apply as long as you have not defaulted on any terms of the account. To receive these rates, you must make no late payments, you must not exceed your credit limit, and your payment checks must not bounce. If you fail to meet any of these terms, then you will be charged at the much higher default rate. According to the disclosure, the default rate is calculated by adding % to the U.S. prime rate (cited at 4% in the disclosure). Therefore, if you assume a prime rate of 4%, then the variable default rate is %.

This credit account carries a temporary low introductory rate (teaser rate) of| %. This teaser APR applies to purchases made within the first months that the account is open. After this introductory period, the APR for purchases reverts to a higher variable APR. This regular APR for purchases is calculated by adding | remains at 4%, then the regular APR for purchases is ]% to the U.S. prime rate (assumed to be 4% in the disclosure). Therefore, if the U.S. prime rate %. For balance transfers, the introductory (teaser) APR i | higher APR of |%. But after the introductory period, the APR for balance transfers reverts to the | % to the prime rate (assumed to be 4%). %. The regular APR for balance transfers is calculated by adding This account does not have an introductory (teaser) APR for cash advances. For cash advances, the APR is calculated by adding| U.S. prime rate (cited at 4% in the disclosure). Therefore, variable APR for cash advances is at least % to the These introductory and regular rates apply as long as you have not defaulted on any terms of the account. To receive these rates, you must make no late payments, you must not exceed your credit limit, and your payment checks must not bounce. If you fail to meet any of these terms, then you will be charged at the much higher default rate. According to the disclosure, the default rate is calculated by adding % to the U.S. prime rate (cited at 4% in the disclosure). Therefore, if you assume a prime rate of 4%, then the variable default rate is %.

Chapter1: Making Economics Decisions

Section: Chapter Questions

Problem 1QTC

Related questions

Question

100%

A quick response will be appreciated

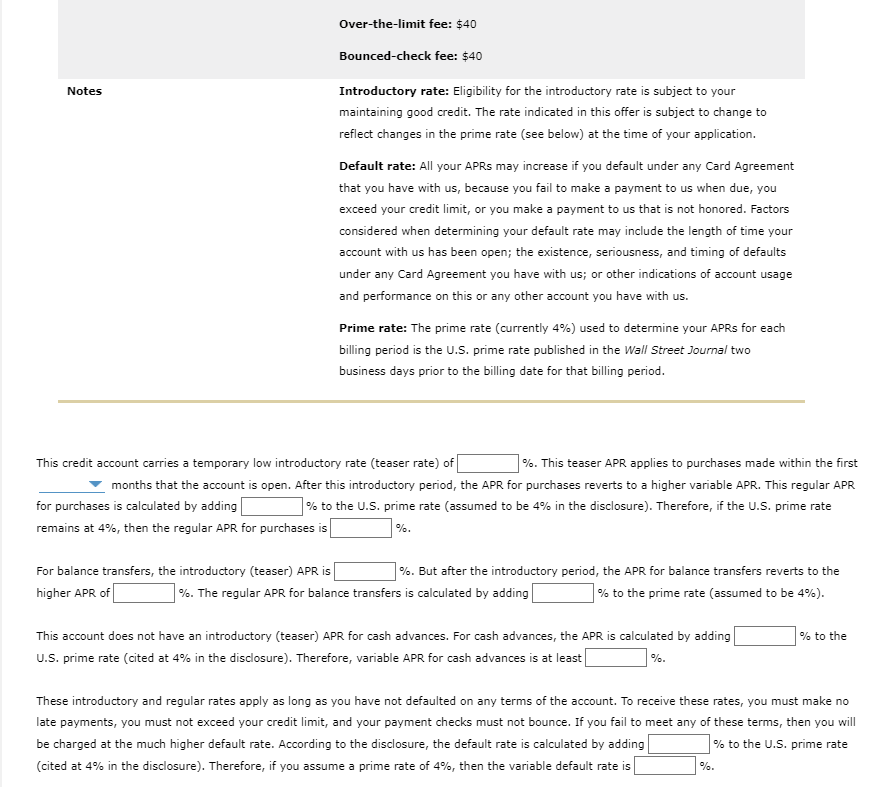

Transcribed Image Text:Over-the-limit fee: $40

Bounced-check fee: $40

Notes

Introductory rate: Eligibility for the introductory rate is subject to your

maintaining good credit. The rate indicated in this offer is subject to change to

reflect changes in the prime rate (see below) at the time of your application.

Default rate: All your APRS may increase if you default under any Card Agreement

that you have with us, because you fail to make a payment to us when due, you

exceed your credit limit, or you make a payment to us that is not honored. Factors

considered when determining your default rate may include the length of time your

account with us has been open; the existence, seriousness, and timing of defaults

under any Card Agreement you have with us; or other indications of account usage

and performance on this or any other account you have with us.

Prime rate: The prime rate (currently 4%) used to determine your APRS for each

billing period is the U.S. prime rate published in the Wall Street Journal two

business days prior to the billing date for that billing period.

This credit account carries a temporary low introductory rate (teaser rate) of

%. This teaser APR applies to purchases made within the first

months that the account is open. After this introductory period, the APR for purchases reverts to a higher variable APR. This regular APR

for purchases is calculated by adding

| % to the U.S. prime rate (assumed to be 4% in the disclosure). Therefore, if the U.S. prime rate

remains at 4%, then the regular APR for purchases is

%.

| %. But after the introductory period, the APR for balance transfers reverts to the

| % to the prime rate (assumed to be 4%).

For balance transfers, the introductory (teaser) APR is

higher APR of

%. The regular APR for balance transfers is calculated by adding

This account does not have an introductory (teaser) APR for cash advances. For cash advances, the APR is calculated by adding

% to the

U.S. prime rate (cited at 4% in the disclosure). Therefore, variable APR for cash advances is at least

%.

These introductory and regular rates apply as long as you have not defaulted on any terms of the account. To receive these rates, you must make no

late payments, you must not exceed your credit limit, and your payment checks must not bounce. If you fail to meet any of these terms, then you will

be charged at the much higher default rate. According to the disclosure, the default rate is calculated by adding

% to the U.S. prime rate

(cited at 4% in the disclosure). Therefore, if you assume a prime rate of 4%, then the variable default rate is

%.

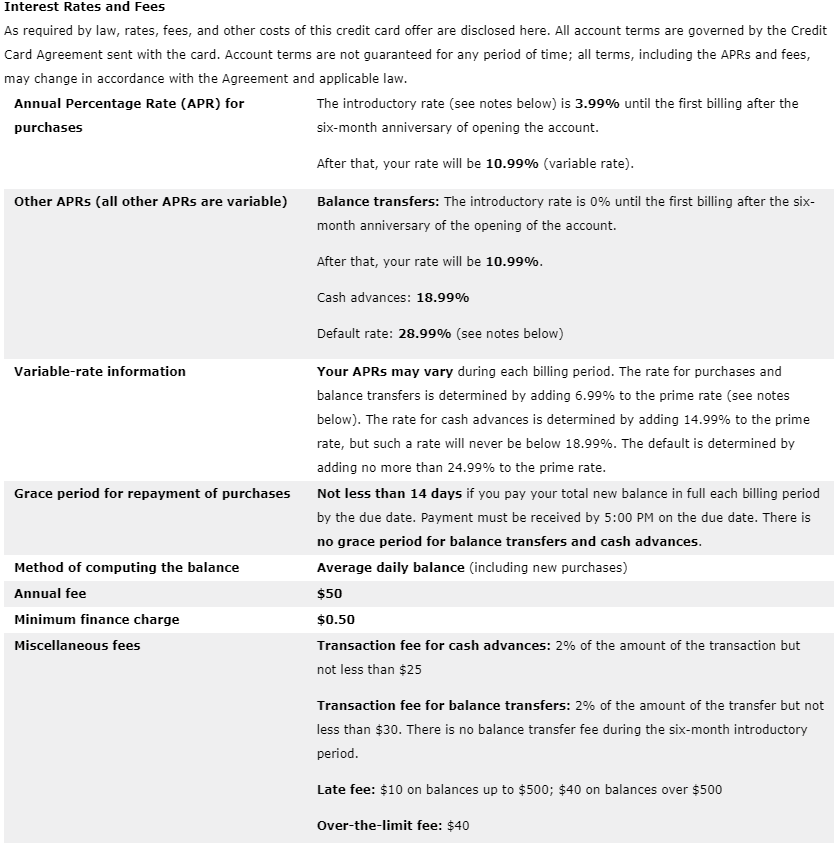

Transcribed Image Text:Interest Rates and Fees

As required by law, rates, fees, and other costs of this credit card offer are disclosed here. All account terms are governed by the Credit

Card Agreement sent with the card. Account terms are not guaranteed for any period of time; all terms, including the APRS and fees,

may change in accordance with the Agreement and applicable law.

Annual Percentage Rate (APR) for

The introductory rate (see notes below) is 3.99% until the first billing after the

purchases

six-month anniversary of opening the account.

After that, your rate will be 10.99% (variable rate).

Other APRS (all other APRS are variable)

Balance transfers: The introductory rate is 0% until the first billing after the six-

month anniversary of the opening of the account.

After that, your rate will be 10.99%.

Cash advances: 18.99%

Default rate: 28.99% (see notes below)

Variable-rate information

Your APRS may vary during each billing period. The rate for purchases and

balance transfers is determined by adding 6.99% to the prime rate (see notes

below). The rate for cash advances is determined by adding 14.99% to the prime

rate, but such a rate will never be below 18.99%. The default is determined by

adding no more than 24.99% to the prime rate.

Grace period for repayment of purchases Not less than 14 days if you pay your total new balance in full each billing period

by the due date. Payment must be received by 5:00 PM on the due date. There is

no grace period for balance transfers and cash advances.

Method of computing the balance

Average daily balance (including new purchases)

Annual fee

$50

Minimum finance charge

$0.50

Miscellaneous fees

Transaction fee for cash advances: 2% of the amount of the transaction but

not less than $25

Transaction fee for balance transfers: 2% of the amount of the transfer but not

less than $30. There is no balance transfer fee during the six-month introductory

period.

Late fee: $10 on balances up to $500; $40 on balances over $500

Over-the-limit fee: $40

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics (12th Edition)

Economics

ISBN:

9780134078779

Author:

Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:

PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:

9780134870069

Author:

William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:

PEARSON

Principles of Economics (12th Edition)

Economics

ISBN:

9780134078779

Author:

Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:

PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:

9780134870069

Author:

William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:

PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:

9781305585126

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-…

Economics

ISBN:

9781259290619

Author:

Michael Baye, Jeff Prince

Publisher:

McGraw-Hill Education