Two potential pitfalls encountered in the design of performance indicators and measurement systems

Two potential pitfalls encountered in the design of performance indicators and measurement systems

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter10: Decentralization: Responsibility Accounting, Performance Evaluation, And Transfer Pricing

Section: Chapter Questions

Problem 30P

Related questions

Question

Two potential pitfalls encountered in the design of performance indicators and measurement systems

Transcribed Image Text:D Corporation is one of the major producers of pre-fabricated houses in the home building

industry. The corporation consists of two divisions:

1. Bell Division, which acquires the raw materials to manufacture the basic house components

and assembles them into kits.

2. Cornish Division, which takes the kits and constructs the homes for final home buyers.

The corporation is decentralized and the management of each division is measured by its income and

return on investment.

Bell Division assembles seven separate house kits using raw materials purchased at the

prevailing market prices. The seven kits are sold to Cornish for prices ranging from US$45,000 to

US$98,000. The prices are set by corporate management of D Corporation using prices paid by Cornish

when it buys comparable units from outside sources. The smaller kits with the lower prices have

become a larger portion of the units sold because the final house buyer is face with prices that are

increasing more rapidly than personal income. The kits are manufactured and assembled in a new plant

purchased by Bell this year. The division had been located in a leased plant for the past four

years.

All kits are assembled upon receipt of an order from the Cornish Division. When the kit is

completely assembled it is immediately taken by the Cornish Division for final construction. Thus, Bell

Division has no finished goods inventory.

The Bell Division's accounts and reports are prepared on an actual-cost basis. There is no budget

and standards have not been developed for each product. A factory overhead rate is calculated at the

beginning of each year. The rate is designed to charge all overhead to the product each year. Any under-

or over- applied overhead is allocated to the cost of goods sold account and the WIP inventories.

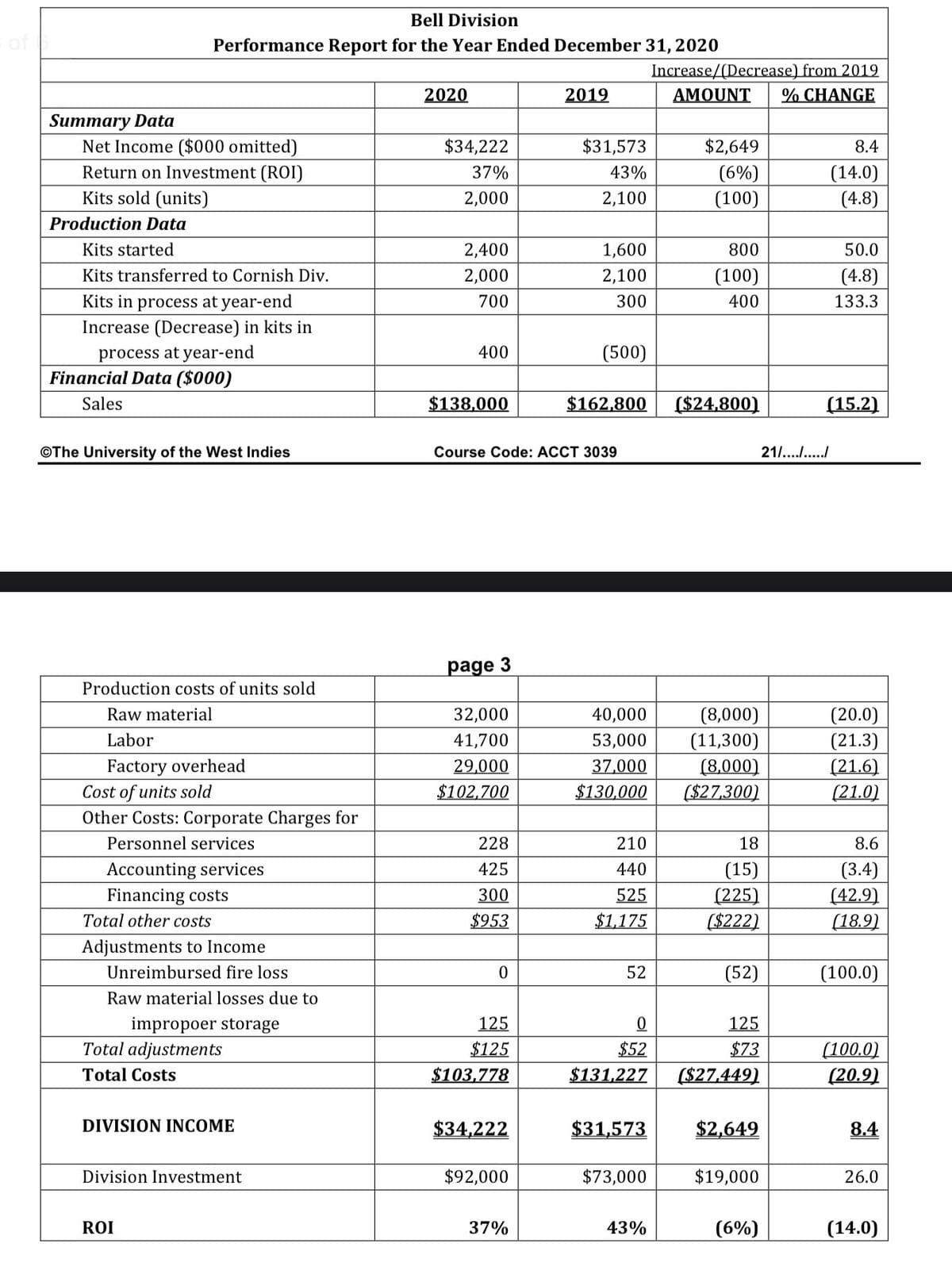

Bell Division's annual report is presented below. This report forms the basis of the evaluation of

the division and its management by the corporation management.

Additional information regarding corporate and division practices is as follows:

The corporation office does all the personnel and accounting work for each division.

The corporate personnel costs are allocated on the basis of number of employees in the

division.

The accounting costs are allocated to the division on the basis of total costs excluding

corporate charges.

The division administration costs are included in factory overhead.

The finance charges include a corporate-imputed interest charge on division assets and

divisional lease payments.

any

The division investment for the ROI calculation includes division inventory and plant and

equipment at gross book value.

Transcribed Image Text:Bell Division

Performance Report for the Year Ended December 31, 2020

Increase/(Decrease) from 2019

% CHANGE

2020

2019

AMOUNT

Summary Data

Net Income ($000 omitted)

Return on Investment (ROI)

Kits sold (units)

$34,222

$31,573

$2,649

8.4

(6%)

(14.0)

(4.8)

37%

43%

2,000

2,100

(100)

Production Data

Kits started

2,400

1,600

800

50.0

Kits transferred to Cornish Div.

2,000

2,100

(100)

(4.8)

Kits in process at year-end

700

300

400

133.3

Increase (Decrease) in kits in

(500)

process at year-end

Financial Data ($000)

400

Sales

$138,000

$162,800

($24,800)

(15.2)

©The University of the West Indies

Course Code: ACCT 3039

211.../

page 3

Production costs of units sold

40,000

(8,000)

(11,300)

(8,000)

($27,300)

(20.0)

(21.3)

(21.6)

(21.0)

Raw material

32,000

Labor

41,700

53,000

Factory overhead

29,000

37,000

Cost of units sold

$102,700

$130,000

Other Costs: Corporate Charges for

Personnel services

228

210

18

8.6

Accounting services

Financing costs

(15)

(225

($222)

425

(3.4)

(42.9)

(18.9)

440

300

525

Total other costs

$953

$1,175

Adjustments to Income

Unreimbursed fire loss

52

(52)

(100.0)

Raw material losses due to

125

125

impropoer storage

Total adjustments

$125

$52

$73

(100.0)

(20.9)

Total Costs

$103,778

$131,227

($27,449)

DIVISION INCOME

$34,222

$31,573

$2,649

8.4

Division Investment

$92,000

$73,000

$19,000

26.0

ROI

37%

43%

(6%)

(14.0)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning