When Jacob Kohler died unmarried in 2015, he left an estate valued at $7,900,000. His trust directed distribution as follows: $20,000 to the local hospital, $170,000 to his alma mater, and the remainder to his three adult children. Death-related costs and expenses were $15,800 for funeral expenses, $50,000 paid to attorneys, $3,500 paid to accountants, and $35,000 paid to the trustee of his living trust. In addition, there were debts of $80,000. Use Exhibit 15.7 and Exhibit 15.8 to calculate the federal estate tax due on his estate. Round your answer to the nearest whole dollar.

When Jacob Kohler died unmarried in 2015, he left an estate valued at $7,900,000. His trust directed distribution as follows: $20,000 to the local hospital, $170,000 to his alma mater, and the remainder to his three adult children. Death-related costs and expenses were $15,800 for funeral expenses, $50,000 paid to attorneys, $3,500 paid to accountants, and $35,000 paid to the trustee of his living trust. In addition, there were debts of $80,000. Use Exhibit 15.7 and Exhibit 15.8 to calculate the federal estate tax due on his estate. Round your answer to the nearest whole dollar.

PFIN (with PFIN Online, 1 term (6 months) Printed Access Card) (New, Engaging Titles from 4LTR Press)

6th Edition

ISBN:9781337117005

Author:Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Chapter15: Preserving Your Estate

Section: Chapter Questions

Problem 9FPE

Related questions

Question

When Jacob Kohler died unmarried in 2015, he left an estate valued at $7,900,000. His trust directed distribution as follows: $20,000 to the local hospital, $170,000 to his alma mater, and the remainder to his three adult children. Death-related costs and expenses were $15,800 for funeral expenses, $50,000 paid to attorneys, $3,500 paid to accountants, and $35,000 paid to the trustee of his living trust. In addition, there were debts of $80,000. Use Exhibit 15.7 and Exhibit 15.8 to calculate the federal estate tax due on his estate. Round your answer to the nearest whole dollar.

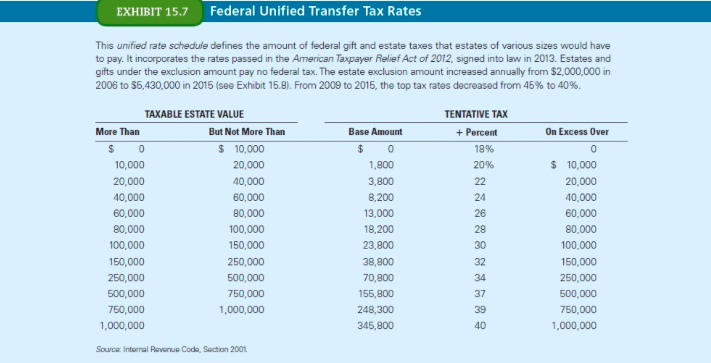

Transcribed Image Text:EXHIBIT 15.7 Federal Unified Transfer Tax Rates

This unified rate schedule defines the amount of federal gift and estate taxes that estates of various sizes would have

to pay. It incorporates the rates passed in the American Taxpayer Relief Act of 2012, signed into law in 2013. Estates and

gifts under the exclusion amount pay no federal tax. The estate exclusion amount increased annually from $2,000,000 in

2006 to $5,430,000 in 2015 (see Exhibit 15.8). From 2009 to 2015, the top tax rates decreased from 45% to 40%.

TAXABLE ESTATE VALUE

TENTATIVE TAX

But Not More Than

On Excess Over

More Than

Base Amount

+ Percent

$ 10,000

$ 0

18%

10,000

20,000

1,800

20%

$ 10,000

20,000

40,000

3,800

22

20,000

40,000

60,000

8,200

24

40,000

60,000

80,000

13,000

26

60,000

80,000

100,000

18,200

28

80,000

100,000

150,000

23,800

30

100,000

150,000

250,000

38,800

32

150,000

250,000

500,000

70,800

34

250,000

500,000

750,000

155,800

37

500,000

750,000

1,000,000

248,300

39

750,000

1,000,000

345,800

40

1,000,000

Source: Intornal Revonue Codo, Section 2001

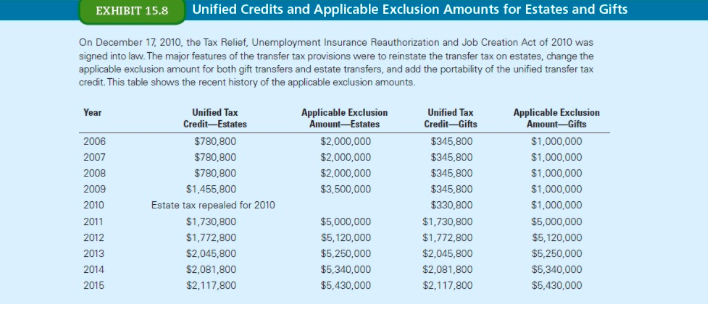

Transcribed Image Text:EXHIBIT 15.8

Unified Credits and Applicable Exclusion Amounts for Estates and Gifts

On December 17, 2010, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 was

signed into law. The major features of the transfer tax provisions were to reinstate the transfer tax on estates, change the

applicable exclusion amount for both gift transfers and estate transfers, and add the portability of the unified transfer tax

credit. This table shows the recent history of the applicable exclusion amounts.

Year

Unified Tax

Credit-Estates

Applicable Exclusion

Amount-Estates

Unified Tax

Credit-Gifts

Applicable Exclusion

Amount-Gifts

2006

$780,800

$2,000,000

$345,800

$1,000,000

2007

$790,800

$2,000,000

$345,800

$1,000,000

2008

$780,800

$2,000,000

$345,800

$1,000,000

2009

$1,455,800

$3,500,000

$345,800

$1,000,000

2010

Estate tax repealed for 2010

$330,800

$1,000,000

$1,730,800

$5,000,000

$1,730,800

$5,000,000

$5, 120,000

$5,250,000

$5,340,000

2011

2012

$1,772,800

$5,120,000

$1,772,800

2013

$2,045,800

$5,250,000

$2,045,800

2014

$2,081,800

$5,340,000

$2,081,800

2015

$2,117,800

$5,430,000

$2,117,800

$5,430,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.{kind=link}

Recommended textbooks for you

PFIN (with PFIN Online, 1 term (6 months) Printed…

Finance

ISBN:

9781337117005

Author:

Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

PFIN (with PFIN Online, 1 term (6 months) Printed…

Finance

ISBN:

9781337117005

Author:

Randall Billingsley, Lawrence J. Gitman, Michael D. Joehnk

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning